Part Two explores where Medicare should be going forward as determined by doctors Richard Gilfillan and Donald M. Berwick. It is an endorsement of the ACO model with changes to it creating greater efficiency. I am not so sure Kip Sullivan would endorse this approach as opposed to Single Payer. Ultimately Single Payer is less costly when we consider the elimination of much of the administration effort. There is another post I will be putting up when I am sure I can see appropriately again. It may touch upon this area of cost saves. In the other half of this post, you will notice I italicized some sentences and then used unitalicized wording. The Italicized sentences are a subject with the normal wording being an explanation. Other than using

Topics:

run75441 considers the following as important: Education, FFS Medicare, Healthcare, Medicare Advantage, politics, US EConomics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

Part Two explores where Medicare should be going forward as determined by doctors Richard Gilfillan and Donald M. Berwick. It is an endorsement of the ACO model with changes to it creating greater efficiency. I am not so sure Kip Sullivan would endorse this approach as opposed to Single Payer. Ultimately Single Payer is less costly when we consider the elimination of much of the administration effort. There is another post I will be putting up when I am sure I can see appropriately again. It may touch upon this area of cost saves.

In the other half of this post, you will notice I italicized some sentences and then used unitalicized wording. The Italicized sentences are a subject with the normal wording being an explanation. Other than using quotes, I felt this was a better way to approach what I wanted to draw attention too. Hope you enjoy the read.

Medicare Advantage, Direct Contracting, And the Medicare ‘Money Machine,’ Part 2: Building on the ACO Model, Health Affairs, Richard Gilfillan and Donald M. Berwick.

In Part one of this two-part post, are the reasons for the surging growth and profits in the Medicare Advantage (MA) programs. The dynamics of growth and profits are related to risk-coding games, making MA a costly form of transfer of public and beneficiary dollars into private hands. As taken from Part one.

The first being the combined activity of private equity and venture capital firms, initial public offerings, special purpose acquisition companies (SPACs), and insurance company purchases of MA-focused firms has soared: more than $50 billion in valuation has been created in the past 18 months, dwarfing the speculative bubble for physician practice management companies in the 1990s.

The second being the amount per covered life implicit in a firm’s overall valuation. Historically, per-life valuations in MA have ranged from $4,000 to $10,500. My earlier Part One post in Exhibit 1 of Part One shows per-life valuations for a sample of recent transactions. The average being $87,000 per beneficiary. This being a “Medicare Gold Rush” as stated by the authors Gilfillan and Berwick.

In Part two the approach fostered originally by the Trump Administration to implant those same dynamics into the traditional Medicare side of the Centers for Medicare and Medicaid Services (CMS) ledger is explored. The effort to do so occurs in the form of the misnamed “Direct Contracting” model.

Part two also offers policy recommendations to restore balance and efficiency to MA and further alternative payment models for traditional Medicare.

Direct Contracting: The Path to Medicare Privatization

Given an Orwellian title, Direct Contracting, launched by Center for Medicare and Medicaid Innovation (CMMI), was anything but direct. “Indirect Contracting” would have been a far more accurate name, since the cornerstone of the program was CMS’s opening the door to non-provider-controlled “Direct Contracting Entities (DCEs).” DCEs became the fiscal intermediaries between patients and providers.

Originally, CMS proposed three Direct Contracting Models: Professional, Global, and Geographic (GEO).

The GEO Direct Contracting model (GEO DC) was the most extreme. It proposes to auto-assign every fee-for-service (FFS) beneficiary in a number of large geographic regions into a fully capitated MA-like “Geo DCE.” Beneficiaries were not given the right to opt out. GEO DCEs were expected to assume total responsibility for all FFS beneficiaries in their region. This responsibility included beneficiaries in any accountable care organizations (ACOs) or other Alternative Payment Models (APMs), except those assigned to other types of DCEs. With full capitation, as with MA, GEO DCEs would be responsible for most claims payments as well as medical management. This was a straightforward privatization of traditional Medicare. Differing from MA only in that GEO Direct Contracting beneficiaries retained the right to see any Medicare provider under standard Medicare coverage.

The Global and Professional Direct Contracting models were combined as GPDC. Along side GEO DC, they appear to be an extension of the ACO approach. Like ACOs, DCEs create a defined provider network. Beneficiaries are either auto-aligned via claims history or voluntarily enrolled. Members maintain access to all Medicare providers under standard benefits. Benchmarks or capitation rates will include a defined discount to CMS. But GPDC DCEs differ in important ways from ACOs. GPDC DCEs can select varying degrees of capitation up to and including full capitation. Full capitation would require them to pay DCE preferred provider claims. Although beneficiaries do have the right to opt out of CMS data sharing, they remain aligned with the DCE for purposes of capitation payments and ultimate financial reconciliation.

The ACO model was built as a Direct Contracting relationship between CMS and providers. ACOs were required to have 75 percent provider governance control. In Direct Contracting, CMS established a stated aim of bringing “organizations currently operating exclusively in Medicare Advantage” into traditional Medicare. This is targeting the very MA insurers and investor-controlled provider firms that are driving the MA overpayments explored in Part One of this post. To help accomplish this, CMS decreased the provider governance requirement to just 25 percent.

CMS created other policies that were favorable for “New Entrants” in the Direct Contracting program. Liberalized marketing and sales opportunities, along with the ability to offer additional benefits, play to the sales strengths of MA firms. The New Entrant benchmark methodology was based more on an MA rate-book approach than the ACO historical cost-blended model that nets out prior savings. New voluntarily enrolled beneficiaries, expected to be the majority of beneficiaries for New Entrants, were excluded from the risk coding constraints for several years.

Another publicly stated Direct Contracting aim was to accelerate progress of Medicare coverage away from FFS payment toward value-based contracting (VBC) “alternative payment models” (APMs). The illogical hypothesis was MA firms, expert at driving costs up, could do a better job controlling costs than existing ACOs. While savings from ACOs have been modest (MedPAC reports 1 percent to 2 percent), accurate evaluation has been difficult. The level of ACO success has been controversial, momentum has built every year in this voluntary program. CMS recently announced that ACOs in 2020 decreased costs by over $4 billion and saved CMS almost $2 billion. MedPAC projects, at a minimum, MA will cost CMS $8 billion more than FFS in 2020 (AB: as it was MedPac reported $12 billion [page 439] in overcharges).

Notwithstanding ACO success, the prior CMS administration also introduced their “Pathways to Success” ACO policy, which created more stringent requirements for provider-led ACOs and triggered a 15 percent decrease in the number of ACOs. The net result is that experienced MA firms are attempting to pull ACOs apart by soliciting ACO physicians to join their DCE networks.

Ironically, this is reminiscent of the original, well-intended strategy for privatized Medicare: to bring health maintenance organization (HMO) savings and care improvements to Medicare. But the Direct Contracting model seems to have ignored the lessons learned from the experience of MA and its predecessors at a cost to CMS and taxpayers of hundreds of billions of dollars. As MedPAC confirmed recently, over 35 years, privatized Medicare has always cost more than traditional Medicare, not less.

Current Status of Direct Contracting

The Trump Administration’s CMS attempted to launch GEO Direct Contracting in its waning days. The Biden administration paused it.

In January 2021, CMS announced the selection of the first tranche of 53 GPDCEs spread across 38 states. Combined, they hold 30 million of the 36 million FFS beneficiaries. A second tranche of DCEs (numbers unknown) were approved by CMS. CMS elected to defer their start dates to January 1, 2022. It then paused further entry into this 2022 tranche, with the exception of Next Generation ACOs. CMS is believed to be considering an additional solicitation for another set of DCEs.

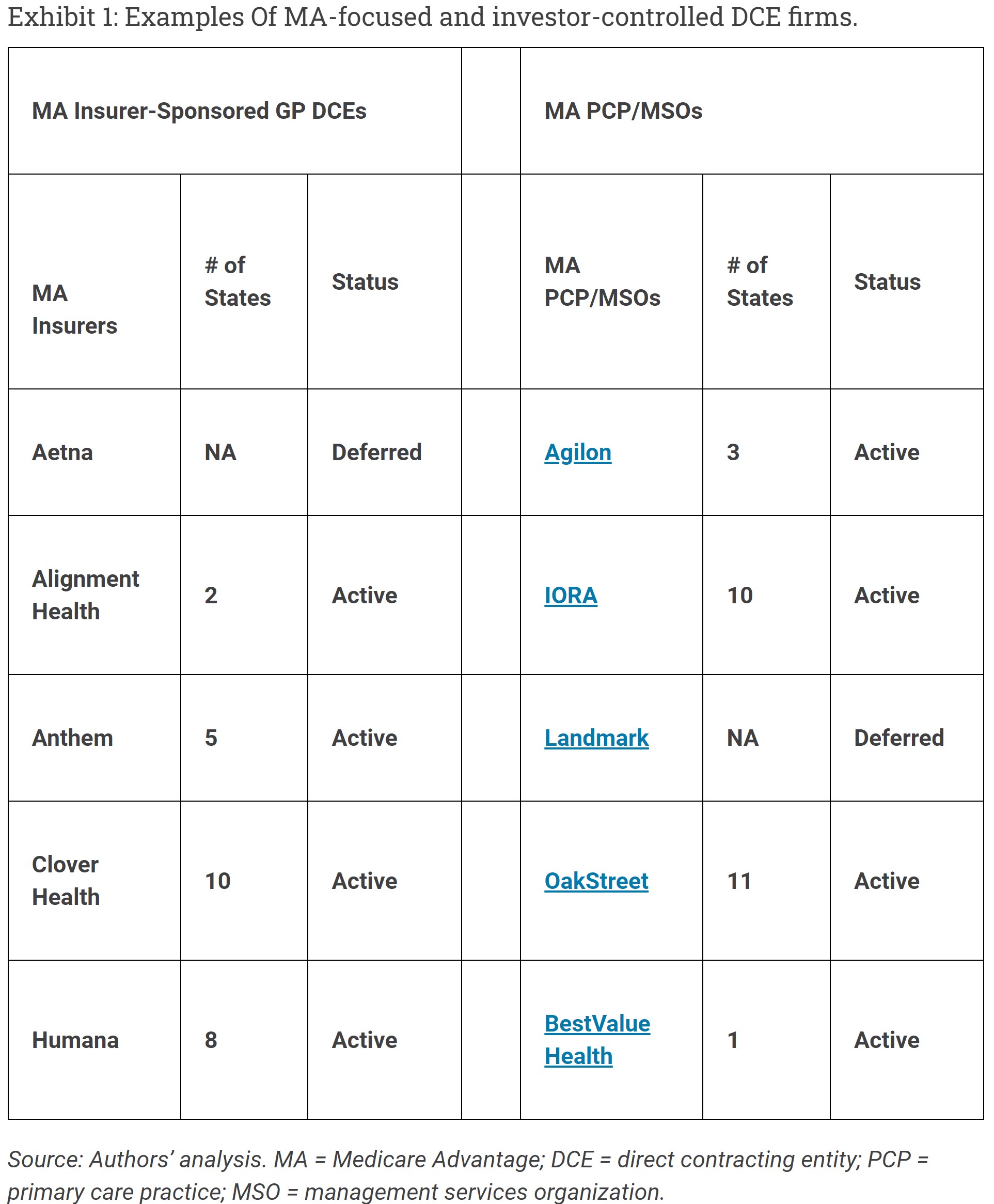

The January tranche did include some traditional, provider sponsored DCEs. However, a majority of the DCEs (28) are investor (not provider) controlled and most have roots in MA. Six of these, owned by four different MA insurers, are approved to operate in 19 states, with potential access to over 20 million traditional Medicare beneficiaries, over 60 percent of the national total. (See exhibit 1)

While CMMI has not identified firms that have deferred until 2022, Cigna is currently recruiting DCE providers. Aetna’s Active health subsidiary was originally approved, and United Healthcare is rumored to be acquiring Landmark (which had also been announced as a DCE).

In short, the largest national insurers are positioning to become DCEs. Each of these national MA companies has a broad national network. The possibility of their using these networks to enroll millions of Traditional Medicare beneficiaries is very real. Currently, CMS has stated publicly “no limits on the growth of DCE networks and geographies.”

Direct Contracting Implications for Beneficiaries

DCEs have the option of selecting varying degrees of capitation from CMS, up to and including full capitation for DCE participating provider services. It is likely insurer DCEs will choose this approach given their history and operating capabilities. Insurer DCEs then will be responsible for paying claims, and they will bring their MA-based medical, claims payment and possibly other managed care administrative practices into Direct Contracting. This environment will be even more confusing than MA, with three different parties processing claims: the DCE, CMS, and the Medicare supplemental insurance payer. In short, millions of traditional Medicare beneficiaries, who made a specific choice not to enroll in MA, will find themselves in an MA-like managed care environment.

Direct Contracting and The Medicare Money Machine

There was a catch in CMS’s strategy to enlist MA firms in Direct Contracting. Would the firms accept the risk without the ability to increase risk scores? CMS seems to have been trying to finesse this issue for the past 18 months. Direct Contracting does have significant constraints on risk score increases.

For individuals aligned via claims, there is a 3 percent symmetrical cap on risk adjustment factor (RAF) score increases year to year. However, there is no cap on the base year, so DCEs can increase their score over time. A program-wide Coding Intensity Factor (CIF) does retrospectively adjust the capped risk adjustment scores for DCEs to correct for aggressive coding at the overall program level. The base year for the CIF is fixed. Thus, while the CIF will decrease code creep for CMS, it will allow the most aggressive coders to benefit at the expense of those who are less aggressive. This reality will lead to major retroactive adjustments to risk scores, financial reconciliation changes, and likely program instability. Alternatively, it is possible that CMS will decide to not enforce the CIF, thereby rewarding gaming.

Originally, voluntarily enrolled individuals who are not aligned with claims, expected to be the majority for new DCEs, would have been excluded from these controls for several years. In response to input from concerned policy and industry experts, CMS has now decreased that exclusion to one year. However, how the voluntarily enrolled individuals will be treated under the cap and the CIF adjustment remains unclear.

DCEs over the past year have already begun evading these constraints by simply increasing risk scores for people before they enroll them. This is exactly what MA firms do with their 64-year-old commercial members prior to enrolling them in MA. As we have heard said by industry insiders,

“There is no bad time to work on risk scores.”

Overall, it appears that, under current DCE rules, aggressive risk coders might still garner 20-40 percent of MA Money Machine profits. That at least seems to be the story DCE representatives are telling PCPs and investors. The other commonly heard story line is that, even if Direct Contracting does not prove profitable, it provides a perfect pathway for wholesale movement of beneficiaries into MA at a much lower cost of sales.

MA Plans are required to use at least 85 percent of premium revenues to pay for claims. As we showed in Part one, the Money Machine eliminates the constraint in MA. Direct Contracting does not have an explicit MLR requirement. The only limit on profits is a risk corridor methodology that provides for graduated CMS sharing in savings or losses that are greater than 25 percent of the Benchmark, a level DCEs are unlikely to attain without risk score gaming. The net result is that Direct Contracting has an implicit but irrelevant MLR requirement of approximately 60 percent, leaving DCEs well positioned to keep virtually all savings as profits.

The Medicare Gold Rush

MA-focused firms, insurers, and investor-controlled primary care practices (PCPs)/management services organizations (MSOs), can now add Direct Contracting profits to their financial prospectus, and they have.

The first six firms in Exhibit 1, Part One of this two-part post are all investor controlling DCEs recently acquiring funds at extraordinary levels. All have cited DCE participation in their investor road shows. Clover Health attributed about 70 percent of their $3.7 billion valuation to Direct Contracting.

These favorable MA and Direct Contracting business model dynamics are enhanced by the strong ambient tailwinds in the Medicare space. One special purpose acquisition company (SPAC) pitch deck highlights the reality of growth in the MA and Direct Contracting market segments.

Driven by baby boomer aging and increasing per capita costs, the results will exceed $600 billion in annual Medicare premiums over the next 5 years. This is probably the largest short-term revenue growth opportunity of any current US industry sector. With such financial opportunities available, it is no surprise the speculative fever runs high on Wall Street.

The evident lack of political will to address the distorted, subsidized MA marketplace, and the growing power of the artificial intelligence – (AI) enabled MA Money Machine add fuel to the speculative fire. The result is IPO, SPAC, and private equity investments that have pushed billions of private investment dollars into acquiring MA-focused firms at prices-per-patient-life (see beginning) beggaring the imagination. From early April 2010 through the end of August 2021, the average stock price for five MA-focused insurers—United Health, Humana, Cigna, Anthem, and CVS/Aetna—increased 825 percent (compared to 280 percent for the entire S&P 500). The market capitalization for the same five entities increased by 497 percent (as opposed to 245 percent for the S&P 500 as a whole). The market thus seems to affirm MA as the must place to be.

The Risks of Insurer-Controlled and Investor-Controlled DCEs

Risk-score gaming in Medicare Advantage, now encroaching into Direct Contracting, is creating an accelerating immediate threat to our health care system. Traditional health care providers typically have a longstanding commitment to their patients and communities.

The large national MA plans have shown a distinctive ability to destroy value by increasing costs, not adding value, with little local community commitment.

As DCEs they will likely find ways to profit through coding or alternatively attempt to move beneficiaries into their MA plans. Either way they will increase Medicare costs at a time when the Trust Fund is in severe jeopardy.

New start-up MA-focused plans are likely short-term players and unlikely in the long run to be able to match the economies of scale of the large national insurers. They will use risk-score gaming to increase rebates, attracting new customers, burning through their start-up money, and ultimately becoming a part of large insurers.

Investor backed PCP/MSO firms are playing a short-term game.

Several offer innovative variations on the intensive PCP clinical-care model probably deliver better, more convenient care, and improved utilization. But all are dependent on the Money Machine to cover their added service costs and their owners’ profits. None offers a sustainable competitive advantage. They likely face either financial failure, rollup, or acquisition by larger firms. This happened in 1990s with Physician Practice Management Companies. This being the same hype, investment froth, story lines, and then roll-up followed by bankruptcy.

ACOs and DCEs both acquire aligned beneficiaries through their participating PCPs.

PCPs cannot be in both for traditional Medicare patients. DCEs are now actively soliciting PCPs to drop their ACO affiliations and join them. Across the country, well-funded DCEs are offering PCPs and ACOs multi-million dollar guarantees. Some are holding out the allure of MA Money Machine-like coding opportunities.

Thus, in yet another ironic twist, CMS is enabling the agents of MA cost increases to undo the ACO initiative, which has decreased costs. The Direct Contracting program poses a direct threat to the ACO experiment now underway in the nation.

A Policy Agenda For Reform

For 35 years, privatized Medicare plans have failed to achieve their primary objective of controlling costs while preserving the quality of care.

Aside from some notable exceptions with group model and staff model HMOs, capitation of privatized Medicare plans has simply allowed insurance companies to collect (from CMS) a toll of 15 percent or more on the total cost of care, to deny or downgrade provider claims, and then to pass through the dollars they finally pay using Medicare’s FFS payment systems and prices. The ability to game the Medicare “star quality rating” system rivals Lake Wobegon: most plans are now above average. It is far easier to game the codes than to improve the care or change health care delivery. Based on this track record, insurers should be eliminated from the Direct Contracting initiative.

Risk-score gaming is today necessary for business success in MA.

Low risk scores lead to higher prices and lower benefits, a recipe for health plan failure. It is extremely costly to continue to ignore the corrosive, insidious effects of the defective MA HCC risk adjustment system. It undercuts the many dedicated hardworking plan and provider teams caring for MA patients. It is fundamentally redefining our primary care networks, turning PCP practices into insurer-owned or investor-owned coding shops, and impacting large integrated systems the same way. If this trend is left alone, CMS will witness even more rapid MA growth. With it, a more rapid descend to Trust Fund insolvency.

Direct contracting should be indeed “direct.”

That is an arrangement with provider-governed organizations, not financial intermediaries.

- If primary care needs capital, the capital should be tied to the expectation that providers will control how it is used. If CMMI wants to test investor-backed start-up firms? It should do it only at the limited scale needed for the test and only through direct providers of care and not through reconstituted or renamed MA Plans.

- If the scale of Direct Contracting outpaces the evidence? The Direct Contracting model will instead be what the Trump Administration seemed to intend. It will be an effort driven by ideological doctrine to turn over to private hands Medicare, the nation’s most popular universal public program.

Our health care system has responded to the COVID pandemic with heroic work by nurses, physicians, hospital employees, and leaders. We will continue to need all of those services in the future. But we also need to redesign our care system. A far better system is not hard to imagine.

- It would be based in homes and community settings, using hospitals only as a last resort.

- It would invest heavily both in primary prevention—addressing the true social drivers of illness, injury, and disability—and secondary prevention, helping people with chronic illness anticipate and intercept deterioration.

- It would focus sharply on what matters to patients.

- It would assure continuity of care for patients across time and among care settings.

The Triple Aim of better care for individuals, better health for populations, and lower per capita cost can be and should be, its North Star. This can only be achieved through major changes and improvements in the actual delivery of care, itself, not through financial gaming.

Change Medicare Advantage

The MA program is fundamentally flawed.

Most sensible business-minded large employers in America do not give an insurer all their health care money upfront. They know that would cost them more. Instead, they hire administrators, not financial optimization firms. Although politically difficult, the following changes in policy would better position the Medicare Advantage program to meet its original, valuable objectives: to foster innovation in care and coverage, to improve the quality of care, and to reduce per capita costs without harm to patients.

MA overpayments are the consequences of policy decisions, and those decisions could be changed.

Congress should instruct CMS to announce an intention to replace the current Hierarchical Condition Category (HCC) RAF scoring system in the next three years. It should sponsor a major developmental effort to design a replacement risk adjustment methodology that does not rely on provider reporting and that is resistant to gaming. The model would need to address plan-specific and contract-specific risk scores. Potential approaches could include the DECI approach, expansion of the Beneficiary Survey, or potentially the use of small-area social determinants of health models such as the Area Deprivation Index (ADI) and the Child Opportunity Index (COI).

Congress should order CMS to follow the MedPAC recommendations for fixing the structural over-payments related to benchmarks and the Quality Bonus Program.

In the absence of eliminating the HCC system?

CMS should move immediately toward a more realistic Coding Intensity Factor (CIF), increasing it by at least the 1 percent per year differential between MA and FFS coding creep. This would freeze MA RAF overpayments at the current level, eliminate the threat of benefit cuts from MA Plans, and provide significant out year savings. CMS should also constrain the MA Money Machine contracting approaches that incent and reward coding and ensure that such incentive payments to owned physician groups are excluded from MLR calculations.

Importantly, CMS should assure a level playing field for comparing and transparently reporting results in beneficiary care, disease prevention, and total per capita health care costs between the ACO programs and Medicare Advantage.

Replace Or Redesign the Direct Contracting Model Experiment, Some Actions

The best way to mitigate the undesirable effects of Direct Contracting would be to stop the program.

CMS should announce that the Direct Contracting Model will be replaced in 2023 by a new Medicare Shared Savings Program (MSSP) model that uses CMMI authority to create more advanced tracks for providers, including full capitation. Features should include:

- Primary Care Capitation

- Use of the taxpayer identification number-national provider identifier combination

- Upfront discount and 100 percent of savings option

- Full capitation

- A way to let new entrants into the program

- Easier voluntary enrollment per the Direct Contracting model

- Enhanced benefits for beneficiaries; and extended care delivery waivers

- More upfront investment for providers without access to capital.

The HHS Secretary should pursue a path to mandating ACO participation by hospitals, physicians and other providers over five years using CMMI authority based on evidence of success from Pioneer, MSSP, and other ACO models. The MSSP advanced tracks should include only entities that follow the 75 precent provider governance rule, and they should provide guardrails for MA-focused investor-backed entities.

If CMS cannot simply stop the Direct Contracting experiment, at a minimum CMS should make clear that Direct Contracting is a small experiment, not a path to replacement of ACOs. (See Appendix 1)

The number of beneficiaries should be limited to 1.3 million, (about the size of the Next Gen ACO test, or about 10 percent of the MSSP) and CMS should limit the size of any specific DCE. CMS should also establish disincentives and rules for DCEs to prohibit movement of beneficiaries to MA, such as fixing the risk score of beneficiaries that move from Direct Contracting to MA at 1.0 in perpetuity.

As with Medicare Advantage, CMS should take specific steps to eliminate risk-score gaming opportunities for DCEs, and to substitute an alternative risk adjustment methodology as discussed above.

CMS should assure public transparency for the progress and results of the Direct Contracting model, including access to primary data to facilitate independent evaluations. As detailed in Appendix 1, (at the bottom of Part 2). CMS should also create guardrails for remaining investor controlled DCEs.

In any event, CMS should eliminate all insurers from the Direct Contracting model.

MA insurers should focus their attention on delivering the Triple Aim (not higher costs) in MA, not to invading the traditional Medicare space. CMS and CMMI should proceed cautiously in any new Direct Contracting model test to avoid excessive and unwise distortions of investment and impediments to the (simultaneous) ongoing development, improvement, and expansion of ACO models, built on the decade of ACO experience so far. CMS should reinstate the 75 percent provider governance rule for DCEs. Direct Contracting should be with providers, not investors. It would take a major redesign, addressing many of the issues identified above, to make Direct Contracting the future path for provider-based value transformation.

Advance And Build Upon the Accountable Care Organization Experience

Health care costs as a percent of gross domestic product have flattened since the ACA.

While spillover effects are hard to measure and many components of the ACA affected Medicare spending, Medicare per capita spending growth since ACOs were introduced has been the lowest in decades, notwithstanding the higher trend in MA spending per capita. In their first eight years,

ACOs have brought tens of thousands of providers and virtually all segments of the health care industry toward population heath management. CMS data shows that ACOs, which care for over 12 million beneficiaries in 2021, have now generated gross savings of nearly $14 billion and net savings to CMS of over $4 billion.

Some observers have questioned those numbers and recommended significant changes to encourage more ACO engagement and investments by providers.

As CMS Administrator Chiquita Brooks-LaSure and coauthors recently wrote on Health Affairs Blog,

“While voluntary models can demonstrate a proof of concept, they limit the potential savings and full ability to test an intervention . . . “

We believe the MSSP ACO program, further adapted, is poised to expand rapidly toward global payments and population-based payments, with many participants now ready to accept full risk, exiting at last from the shackles of FFS. CMS should, as fast as is feasible, develop more advanced MSSP ACO models using CMMI authority to include global payment models, and make the MSSP model more inclusive of physician practices at the threshold of participation.

Providers have vacillated for 10 years between FFS and an accountable, value-based care business model.

While results from accountable care have not yet been optimal, enough ACO success is in hand to support the belief that providers would be successful if the models were further developed and made mandatory. CMS should provide a multi-year strategy to make FFS less attractive and the ACO opportunity more attractive, leading ultimately to a mandatory ACO program. That commitment would also discourage ACOs from trying to succeed simply by cherry picking efficient providers, rather than trying to improve the mainstream.

CMS should ensure that advancing other payment models, especially Direct Contracting, does not block or impede further development of ACOs, drawing on lessons learned so far.

Support A Constructive Role For Private Investment:

Change requires capital.

Creating the health care delivery of the future requires investment, public and private, to help incumbent providers develop new skills and systems, and to help create new entrants with care designs usefully disruptive to legacy models. The non-profit health care sector (especially its primary care components) has had difficulty finding that capital. Investors backed such investment in ACO-enabling firms. These firms and their investors are now being lured into the MA world by easy money. It is essential to correct the HCC Risk Score system to appropriately align capital. We owe entrepreneurs a fair opportunity for return commensurate with risk. We do not owe them fish in a barrel, as MA offers.

As CMS becomes even more effective as a sponsor for care innovation, it will need the savvy and skills to distinguish between helpful private investment and exploitative private investment. Fixing the costly defects in MA and forbidding the importation of those same defects into traditional Medicare, while authentically testing new models of payment, is a good place to start.

Appendix 1: Direct Contracting Model Guardrails (use link) Not really nescessary to include here.

Some Definitions:

Direct Contracting (DC) model. Transfers cost and care management to private for-profit insurer and investor contracting entities. CMS auto-assigns more than 30 million beneficiaries who have chosen traditional Medicare. DC entities are managed by private for-profit companies, without their understanding or consent. These are similar to Medicare Advantage plans even though the enrollees explicitly rejected this type of coverage. Although not technically permissible, contracting entities could shift enrollees to Medicare Advantage.

Capitated. relating to, participating in, or being a health-care system in which a medical provider is given a set fee per patient (as by an HMO) regardless of the treatment required.

Capitation: The payment of a fee or grant to a doctor, school, or other person or body providing services to a number of people, such that the amount paid is determined by the number of patients, students, or customers.

Value-based contracting (VBC); Not including Medicare Advantage programs. Value-based programs reward health care providers with incentive payments for the quality of care they give to people with Medicare.

GPDCE; Global and Professional Direct Contracting (GPDC) Model was a voluntary, Accountable Care Organization (ACO) model designed to put patients at the center of their care. Building upon lessons-learned from initiatives involving Medicare ACOs, such as the Medicare Shared Savings Program and the Next Generation ACO Model, this model provided greater individualized attention to a beneficiary’s specific health care needs within Original Medicare, and changed financial incentives to reward high quality care. The GPDC Model beyond December 31, 2022

Hierarchical Condition Category (HCC): coding is a risk-adjustment model design to estimate future health care costs for patients. (read the link for further explanation).

Coding Intensity Factor (CIF); The retrospective CIF ensures the change in normalized risk scores across all claims-aligned beneficiaries is zero between the baseline year (2019) and the PY. It will be applied uniformly across ACOs for a given risk adjustment model. (PNHP)

Triple Aim: goals of improved quality of care, improved population health, and reduced cost.

Some Readings

Medicare Advantage, Direct Contracting and The Medicare ‘Money Machine’ Part 1: The Risk-Score Game, Angry Bear, Richard Gilfillan and Donald M. Berwick

MedPAC – Medicare Payment Advisory Commission (via Public) / For the record: MedPAC’s response to AHIP’s recent “Correcting the Record” blog post, publicnow.com, MedPac.

The Medicare Advantage program: Status report and mandated report on dual eligible special needs plans. Chapter 12, MedPAC March 2022, Report to the Congress, (page 439 for MA over coding costs).

Accountability for Medicare Advantage plans is long overdue, PNHP, Physicians for a National Health Program (next up).