Published by: https://braveneweurope.com/sergio-cesaratto-sharing-central-banks-costs-and-profits-of-monetary-policy-in-the-euro-area Sergio Cesaratto - Sharing Central Banks’ costs and profits of monetary policy in the euro area (Adapted for Brave New Europe from Lavoce.info) ; the author thanks Giancarlo Bergamini for help in editing the translation). A debate has developed in Europe (on Vox.eu and elsewhere) on the fiscal costs related to the interest payments that central banks in the eurozone are bestowing on commercial banks, a result of the way monetary policy is currently conducted. The implementation of monetary policy currently revolves around the ECB's direct control of the interest rate paid on an abundant excess of bank reserves (relative to mandatory reserve

Topics:

Sergio Cesaratto considers the following as important: Brave New Europe, Cesaratto, eurosystem, excess reserves, Monetary income

This could be interesting, too:

Sergio Cesaratto writes Nuovo Working Paper di dialogo interdisciplinare fra economisti e antichisti

Sergio Cesaratto writes La nuova governance fiscale europea

Sergio Cesaratto writes Draghi mercantilista?

Sergio Cesaratto writes Il “Nobel” ad Acemoglu et c. commentato e criticato su Ottolina TV

Published by: https://braveneweurope.com/sergio-cesaratto-sharing-central-banks-costs-and-profits-of-monetary-policy-in-the-euro-area

Sergio Cesaratto - Sharing Central Banks’ costs and profits of monetary policy in the euro area

(Adapted for Brave New Europe from Lavoce.info) ; the author thanks Giancarlo Bergamini for help in editing the translation).

A debate has developed in Europe (on Vox.eu and elsewhere) on the fiscal costs related to the interest payments that central banks in the eurozone are bestowing on commercial banks, a result of the way monetary policy is currently conducted. The implementation of monetary policy currently revolves around the ECB's direct control of the interest rate paid on an abundant excess of bank reserves (relative to mandatory reserve requirements) (see Cesaratto 2020, chapter 7). This excess is the result of past quantitative easing (QE) operations whereby the eurozone's national central banks (NCBs) bought government and corporate bonds by issuing reserves (liquidity). At the ECB's current target rate of 3.75 per cent, banks are collecting considerable sums, more than 118 billion per year rebus sic stantibus. This also happens in other monetary areas, but there are European peculiarities.

To begin with, the uneven distribution of excess reserves among Eurosystem countries makes it difficult follow De Grauwe’s suggestion to raise the mandatory reserve ratio so as to transform excess liquidity into unremunerated compulsory liquidity. This mismatch is measured against the capital key, i.e. the NCBs' share in the ECB's capital. Relative to this parameter, excess liquidity is, for example, larger in Germany and smaller in Italy. In order to comply with a higher reserve requirement, Italian banks could thus find themselves having to borrow reserves from banks beyond the Alps or from the ECB at very expensive rates. An additional issue concerns the fact that the interest expenses that each NCB incurs to remunerate the excess reserves of its jurisdiction are shared among all NCBs according to capital key. Again, the fact that excess reserves are not shared according to the capital key has significant consequences. In fact, in jurisdictions where liquidity is relatively more abundant (such as Germany), disbursements to local commercial banks will be relatively larger, but the respective NCBs (such as the Bundesbank) may share these costs with NCBs in jurisdictions where liquidity is more scarce (such as the Bank of Italy). The result is that the Bank of Italy, effectively the Italian taxpayer, finds itself subsidising German commercial banks.

This result, however, needs to be checked by examining the set of rules concerning the centralisation and redistribution of a complex of expenses and profits that the NCBs pool through the monetary income of the Eurosystem, a hitherto little known (or poorly explored) institution of European monetary governance. A more comprehensive discussion is now available here.

In a nutshell, the NCBs channel their respective revenues and costs related to monetary policy operations and the running of the payments system into the monetary income of the Eurosystem, a kind of yearly income-tax declaration, if the metaphor helps. Acting as a mere administrator, the ECB subsequently redistributes the monetary income according to the capital key. The logic seems to be to proportionally allocate costs and revenues of operations and functions undertaken on the basis of joint decisions (for the record, the Eurosystem functions by decentralising most operational functions to the NCBs).

Monetary policy operations generating costs and profits for the NCBs include: the ‘refinancing operations’ by which the NCBs create liquidity and which are normally interest-bearing (indeed, the famous targeted longer-term refinancing operations (TLTRO) long-term refinancing operations were conducted until mid-2022 at negative rates, implying costs for the NCBs at that time); the aforementioned QE policies with attendant yield accrued to securities purchased; the remuneration of deposit accounts at the NCBs where commercial banks hold reserves. The rates on these deposits were negative until mid-2022 (entailing then revenues for the NCBs), but are now positive, with the mentioned exorbitant costs for the NCBs.

Monetary income generates a redistribution between NCBs if, for reasons beyond its control, an NCB in executing common decisions does not perform a certain operation in line with its capital key, or at a rate different from the other NCBs. For example, when Italian commercial banks used TLTROs at negative rates in greater proportion than German commercial banks, the Bundesbank bore part of the costs of the Bank of Italy. The first row of Table 1 (from the Bank of Italy’s Annual Accounts 2023) shows how, on the other hand, in 2023, with fully positive rates, Bank of Italy centralised €7,831m of revenues from these operations (a subtraction from the revenues of its profit and loss [P&L] account) into monetary income, receiving back only €4,525m, thus having reduced the revenues from its P&P account by €3,306m. Looking at the reserve accounts, Angelo Baglioni documents how in 2023 the Bundesbank had on average a higher share of the Eurosystem's total excess reserves than its capital key (31.7% vs. 26.6%); the obverse for the Bank of Italy (5.7% vs. 16.0%). This implies that the Italian NCB has borne part of the costs incurred by Frankfurt. The sixth row of Table 1 (sorry, in Italian) shows, in fact, that Bank of Italy pools interest losses on excess reserves of €7.850m, but is allocated €21.973m, with an additional loss recorded in its P&L account of -€14.123m (it had originally provisionally recorded losses of €7.8bn, which became almost €22bn following the redistribution).

A special discourse has to be made for the government bonds purchased by the NCBs through the mentioned QE between 2015 and 2022 (the bulk of QE). Each NCB bought (apart from temporary deviations permitted by the latest Pandemic emergency purchasing programme-PEPP) national securities according to capital key and assumed the relative risk (no risk-sharing involved), retaining the relative actual revenues (usually transferred back to the respective government). For the purposes of calculating monetary income, the procedures require each NCB to contribute an amount of interest calculated at a conventional interest rate equal to that on the main refinancing operations (currently 4.25%). It is easily shown, however, that in fact each NCB then gets back what it paid, so that in this case nothing is shared. In intuitive terms: since each NCB centralises an income calculated on a stock of assets respectful of the capital key and at a common interest rate, what is pooled is precisely equal to what is received back, that is the net redistribution is zero. The third row of the table shows that this is roughly true, but there is a residual (-€2,438m) due, it seems, to the fact that the Bank of Italy has bought something more than its capital key (as allowed by the PEPP) and therefore must share the interest revenues with the other NCBs.

Tavola 1 – Scomposizione del risultato netto della ridistribuzione del reddito monetario (milioni di euro)

|

VOCI |

2023 |

2022 |

|||

|

Reddito monetario |

|||||

|

Totale Eurosistema |

Accentrato dalla Banca (A) |

Redistribuito alla Banca (B) |

Risultato netto (B–A) |

Risultato netto |

|

|

Rifinanziamento alle istituzioni creditizie |

26.850 |

7.831 |

4.525 |

–3.306 |

248 |

|

Titoli detenuti per finalità di politica monetaria (a rischio condiviso) |

8.483 |

703 |

1.430 |

727 |

324 |

|

Titoli detenuti per finalità di politica monetaria (a rischio non condiviso) (1) |

127.854 |

23.984 |

21.546 |

–2.438 |

–346 |

|

Crediti intra Eurosistema equivalenti al trasferimento delle riserve |

1.335 |

225 |

225 |

— |

— |

|

Crediti intra Eurosistema (netti) derivanti dall’allocazione delle banconote in euro |

–4.817 |

1.877 |

–812 |

–2.689 |

–427 |

|

Depositi delle istituzioni creditizie |

–130.387 |

–7.850 |

–21.973 |

–14.123 |

–689 |

|

Debiti/crediti intra Eurosistema risultanti dalle transazioni TARGET |

14.172 |

–22.769 |

2.388 |

25.157 |

4.276 |

|

Gap (2) |

–2.730 |

3.998 |

–460 |

–4.458 |

–1.011 |

|

Totale |

40.760 |

7.999 |

6.869 |

–1.130 |

2.375 |

(1) Ai fini del calcolo del reddito monetario, sono considerati fruttiferi di interessi in misura pari al tasso marginale applicato alle operazioni di rifinanziamento principali; pertanto il relativo reddito accentrato differisce dagli interessi attivi esposti nella sottovoce 1.1.

(2) Differenza tra attività earmarkable e liability base. Include altre componenti minori.

Fonte: Banca d’Italia (2024, p.78, tavola 38).

Costs and revenues related to the operation of the payment system, i.e.

attendant to the TARGET2 platform

and the issuance of banknotes, also enter into monetary income, but with

surprising results.

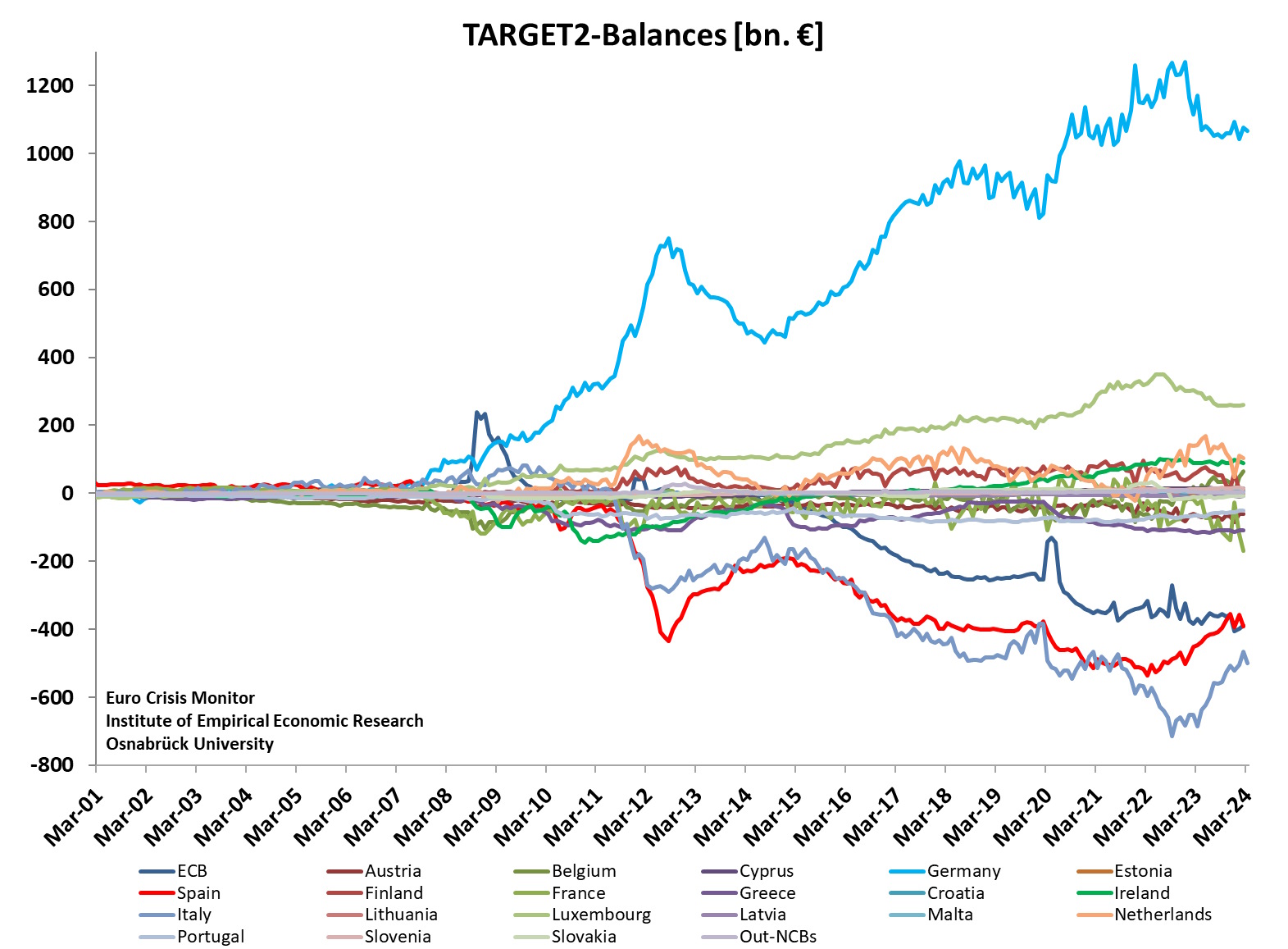

The analysis of monetary income reveals how, de facto, on the enormous TARGET2 (T2) balances, positive in particular for Germany (by more than €1 trillion) and symmetrically negative for Italy and Spain (each by more than €400 billion), no interest is paid, an issue on which there has been extreme confusion until now (as anticipated by Brave New Europe). On the one hand, it is true that during the year, NCBs with negative T2 balances pay interests (at the conventional rate) which, via the ECB, are collected by NCBs with positive balances. At the end of the year, however, losses and profits are all pooled into the shared monetary income, so that they disappear from the P&L account of the respective NCBs. The Eurosystem for its part has nothing to share since the profits contributed by some NCBs are exactly offset by the losses pooled by the remaining NCBs. Row 7 of the table shows that Bank of Italy centralises losses (subtracting them from its P&L account) of €22,769m. The fact that, in addition to making a negative contribution to monetary income, it even receives something back (€2,388m) has nothing to do with T2 balances, but with the ECB's redistribution of the interests it earned on its securities purchased under QE (the ECB participated in QE by buying 10% of bonds).

{kind=link}

Something similar happens with the allocation of banknotes. On the one hand, NCBs that have issued more (less) than the capital key are ‘punished’ (‘rewarded’) by paying (receiving) interest payments during the year, but then they pool their respective losses (or profits) to monetary income and everything cancels out. Line 5 shows how Bank of Italy, initially rewarded for issuing below its quota, loses these profits by centralising €1877m, and on top of that receives back a penalty of -€812m. This relates, however, to the ECB's role in banknote issuance – arguably, this is so since NCBs issue banknotes on behalf of the ECB, which is entitled to an 8% share of the total issuance, but must then return to Frankfurt the related seigniorage).

As can be seen, the analysis of Eurozone monetary income is quite complex - we have, for example, left out the last row of Table 1, the ‘gap’, which plays a non-negligible role in the case of Bank of Italy. For this reason we have included many explanatory examples in the paper. It can be seen that the process of sharing and reallocating costs and revenues among NCBs has significant and sometimes surprising impacts. In particular, it is confirmed that, net of the various shared items, Bank of Italy is currently bearing part of the substantial interest that German banks are receiving from the Buba. This would bring Bank of Italy's P&L account into negative territory were it not for the recourse to provisions prudently put aside in recent years (this recourse leads anyway to a loss of public net wealth). In the paper we also show that, to a first approximation at least, the exorbitant remuneration of bank excess reserves is not justified by the negative rates to which they were subject in the past years. Finally, while the effort made by the Bank of Italy (and by the Bank of Spain too) to provide additional information on monetary income this year is very much to be welcomed, further clarifications by the NCBs and the ECB would be desirable.