With the death of Jacques Delors, president of the European Commission from 1985 to 1995, a chapter in European history has ended. The time has come to take critical stock of this decisive period and to draw lessons for the future, a few months ahead of the European elections of June 2024. To say that the Europe we know today was shaped during this period would be an understatement, with the 1986 Single European Act (allowing for the free movement of goods and services), the 1988 European Directive on the liberalization of capital flows and the 1992 Maastricht Treaty. In particular, it was the Maastricht Treaty, narrowly adopted by French voters in September 1992 (51% yes), that transformed the former European Economic Community (EEC, established in 1957 by the Treaty of Rome) into the

Topics:

Thomas Piketty considers the following as important: in-english, Non classé

This could be interesting, too:

Thomas Piketty writes Regaining confidence in Europe

Thomas Piketty writes Trump, national-capitalism at bay

Thomas Piketty writes Democracy vs oligarchy, the fight of the century

Thomas Piketty writes For a new left-right cleavage

With the death of Jacques Delors, president of the European Commission from 1985 to 1995, a chapter in European history has ended. The time has come to take critical stock of this decisive period and to draw lessons for the future, a few months ahead of the European elections of June 2024.

To say that the Europe we know today was shaped during this period would be an understatement, with the 1986 Single European Act (allowing for the free movement of goods and services), the 1988 European Directive on the liberalization of capital flows and the 1992 Maastricht Treaty. In particular, it was the Maastricht Treaty, narrowly adopted by French voters in September 1992 (51% yes), that transformed the former European Economic Community (EEC, established in 1957 by the Treaty of Rome) into the European Union (EU) and endowed it with a single currency. As planned in 1992, the euro came into effect in 1999 for companies and in 2002 for individuals.

The 2005 Treaty establishing a Constitution for Europe – rejected in France in a referendum (55% voted no) and then adopted by Parliament after a few minor changes in the form of the Lisbon Treaty in 2007 – basically confined itself to consolidating the crucial decisions made between 1986 and 1992 and constitutionalizing the principles of free competition and free movement, without any major innovations. The 2012 European Fiscal Compact tightened up the Maastricht criteria on debt and deficits laid down in 1992, again without any significant innovation.

To understand what was at stake in the decisive European negotiations between 1985 and 1995, the reference work remains that published in 2007 by Rawi Abdelal (Capital Rules: The Construction of Global Finance, Harvard University Press). Based on dozens of in-depth interviews with the main political players and senior European officials at the time, in particular Jacques Delors and Pascal Lamy, Abdelal skillfully analyzes the visions of the future and the negotiating leeway of both sides.

In a nutshell, the French Socialists were gambling that the creation of the euro and the European Central Bank (ECB), a powerful federal institution that makes decisions by majority vote, would eventually enable the establishment of a European public power capable of regulating economic forces more effectively than the French left-wing unity government that emerged from the 1981 elections. To achieve this result, they agreed to the central demand of the German Christian Democrats, who advocated absolute liberalization of capital flows, without any public regulation, and in particular without any common taxation. This was a crucial issue largely neglected by French President François Mitterrand and Delors during the negotiations. The foundations of the compromise were laid.

Thirty years on, the outcome of these radical innovations is inevitably mixed. On the one hand, the ECB played a central role in preventing a widespread collapse in the wake of the 2008 financial crisis and the Covid-19 pandemic. After some initial blunders during the Greek crisis and the unnecessary austerity relapse of 2012-2013, majority decision-making enabled the ECB to override national (notably German) vetoes and quickly and efficiently mobilize considerable sums to stabilize the European economy and reduce interest rate differentials within the eurozone. No one knows what would have happened without the single currency, and it has to be said that the Nordic countries that remained outside the euro did not fare so badly. The truth remains that no credible political player is proposing a return to the franc.

Conversely, it is well understood that money creation alone cannot solve all problems. Moreover, central bankers have been far more willing to save banks and bankers than to invest in education, health and the climate. In this way, they have contributed to the increasing concentration of wealth, with the richest benefiting from the swelling of the stock market and real estate assets made possible by share buybacks and public money, while the savings of the poorest are being wiped out by ongoing inflation. The European rules on the free movement of capital laid down in 1992 have proved so extreme and destabilizing that even the IMF decided after the Asian crisis of 1997 and then 2008 to reintroduce some form of capital controls for short-term flows.

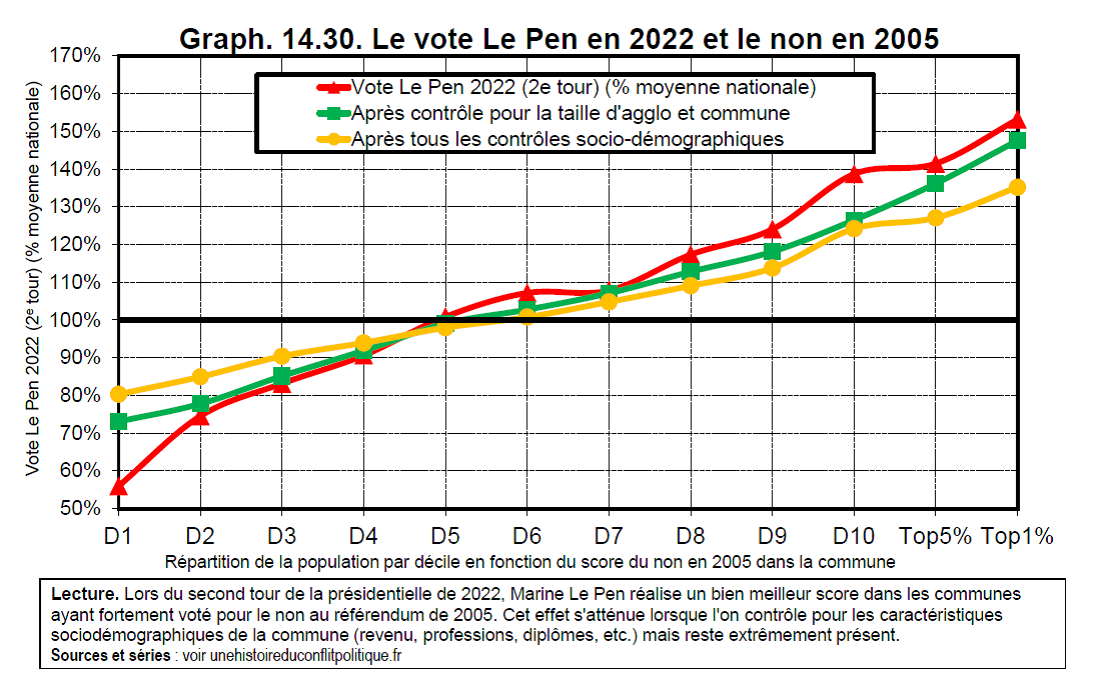

The new European rules have also played a major role in exacerbating tax dumping: endless corporate tax cuts, the unprecedented development of tax havens and the structural under-taxation of billionaires and multi-millionaires. Politically, the 1992 and 2005 referendums contributed significantly to alienating a proportion of the working class from the ballot box and from the left. The « no » vote in 2005 in France thus was the best predictor of the vote for the far-right Rassemblement National party in 2022, particularly in medium-sized towns affected by deindustrialization.

{kind=link}

What can we do about this complex legacy? First, we need to propose to our partners that they set up a strong core within the EU capable of making majority decisions on budgetary, fiscal and environmental matters. Even if this European Parliamentary Union does not see the light of day in the immediate future, it remains the central objective. Second, until a compromise is reached, it will undoubtedly be essential to adopt substantial unilateral measures in the face of intra-European and extra-European fiscal, social and environmental dumping. This will give rise to complex crises that can be overcome if we maintain a consistent internationalist course, and are probably inevitable if we want to break out of the current deadlock.