Summary:

Blog

Keeping bills and carbon low – where next for policy?

Options for energy market reform compared

By

Chaitanya Kumar

12 July 2022

The ongoing cost of living crisis has exposed the vulnerabilities of the UK’s welfare system. A decade of austerity and a culling of green policy measures have left us less prepared in the face of this crisis. Now as inflation continues to soar, with an expectation of it reaching almost 11% this year, the Bank of England is dramatically raising interest rates, which as a result is set to drag the country into a

Topics:

New Economics Foundation considers the following as important:

The ongoing cost of living crisis has exposed the vulnerabilities of the UK’s welfare system. A decade of austerity and a culling of green policy measures have left us less prepared in the face of this crisis. Now as inflation continues to soar, with an expectation of it reaching almost 11% this year, the Bank of England is dramatically raising interest rates, which as a result is set to drag the country into a recession, drive up unemployment and put the biggest squeeze on living standards that we’ve seen in a generation.

NEF has consistently argued that the most effective way of dealing with this crisis in the short term is to lift household incomes and reduce energy demand, particularly on low-income and fuel-poor homes. While the Chancellor has heeded this call with the latest support package of £15bn, the scale of the crisis demands much more intervention. However, the debate is also slowly shifting towards questions of energy market reform that can ensure greater resiliency and less volatility for consumers.

The government is set to consult on a set of high-level reforms of the wholesale and retail energy market design, aimed at reducing the impact of foreign gas on domestic energy bills. This crisis is unfolding within a rapidly changing energy system in the UK. Within the next eight years, over 90% of the country’s electricity is expected to come from low-carbon sources and demand for electricity is expected to jump by nearly 20%, but there is widespread agreement that the current market design isn’t fit to deliver that outcome.

There are three specific challenges that emerge from the current crisis which need to be addressed in the short-to-medium term:

The impact of gas prices on electricity bills – whereby the price of electricity is set by gas power plants, that often provides the energy necessary to balance supply and demand in the system. As gas prices have risen considerably over the past year, so has the price of power, despite an increasing amount of our electricity coming from cheap, renewable energy.

Inadequacy of the price cap to keep low-income household bills sufficiently low – even prior to the consistent hike in the price cap since April last year, energy bills were too high for millions of households with high rates of debt, self-disconnection and overall fuel poverty.

Reconsolidation of the power of the large suppliers (big six) in the energy retail market – with over a dozen small suppliers going out of business, the energy retail market is again consolidated within fewer suppliers, reducing any supposed benefits of competition in the medium to longer term.

Many in the energy policy arena have presented a variety of policy ideas in response to high price volatility and the need for protecting household income. Earlier in the year, the EU commission discussed a set of ideas with its member states that considered the following measures: a single buyer passing-through electricity below market prices to consumers, financially compensating fossil-based fuel generators, a price cap in the wholesale electricity market, and a windfall profit tax. Here in the UK, the notion of a ‘green power pool’, presented by Professor Michael Grubb, has risen in prominence while the Chancellor has already committed to taxing the profits of oil and gas majors through his energy profits levy bill.

While a lot of these measures are focused on tinkering with market design, as either a short or long-term intervention, other civil society groups that are focused on fuel poverty and the climate have presented their own consumer focused measures such as a new social tariff for vulnerable groups, shifting levies from electricity bills and on to general taxation, free provision of energy up to a threshold for specific target groups, and greater cash support for low and vulnerable households.

These ideas do not preclude the urgent need for upgrading the UK’s leaky housing stock, fixing the capacity market that continues to subsidise more fossil fuel generators and scaling up renewables, which are all essential to keep bills and emissions low in the long term.

The following table takes a closer look at some of these measures that have garnered headlines recently, laying out a few pros and cons they carry. The purpose of this exercise is to offer a headline-level comparison of these ideas while acknowledging that a more detailed analytical modelling would be necessary in assessing their relative impact.

Targeted consumer group pay a lower unit price on electricity and gas compared to everybody else (in effect, a secondary price cap that is lower than the current default tariff cap).

Those on pre-payment meters will be default beneficiaries within a wider target group

Supplier costs still passed through, so higher bills for the rest

Mandated on all suppliers, additional to Wam Home Discount and price cap, auto enrolled

Advocated by the National Energy Action and a host of other civil society groups

Also referred as backstop or safeguard tariff

Lower bills for target groups

Incentive for energy demand reduction remains

Relatively low administration costs on suppliers, once supplier and DWP data is matched.

Would incentivise suppliers to hedge long term on behalf of this target base to keep costs low and safeguard against volatility.

Since offered as additional to existing support measures (WHD, Winter Fuel Payments etc.), it does not perversely exacerbate the significant variability within a wider ‘target group’.

Higher bills for the rest of the consumer base.

Even fewer incentives to switch suppliers once the market is more competitive

A fixed/rigid target group can still leave behind a lot of households that legitimately need support

Extreme volatility in the wholesale market, like the one witnessed the past year, will lead to considerable pressures on suppliers and a consequential impact on social tariffs.

Moving levies off electricity bills and possibly on to general tax

Two variations are one that includes all policy costs and another that only shifts legacy renewables and keeps the rest such as ECO or WHD.

The levies on an average bill amount to £160 today.

Widely accepted in civil society and across industry as a progressive move to make

Immediate impact, albeit small, on energy bills reduction while having a progressive redistribution of costs through tax.

Offers a minor reprieve from right wing rhetoric against levies on bills but the threat still remains when the focus might move to higher taxes.

If costs moved on to gas instead, it would significantly enhance the attractiveness of heat pumps and other electrical heating solutions while also benefiting off-gas grid customers that rely on electricity.

Removes artificial advantage for some small suppliers that are exempt from these levies

Moving levies onto gas does not support household bills in general and adds further stress to those who will find it difficult to make a switch to electrification

Moving costs of policy that are current (Energy Company Obligation, WHD) as opposed to legacy (Renewables Obligation) makes them vulnerable to cuts.

Wholesale prices are fixed for a period of time (say 3 years) for a targeted consumer base. This is based on wholesale price forecasts and an estimation of the threshold levels of energy bills for some households. In effect, a form of ‘hard’ price cap that does not move every three months.

If market prices go beyond that, suppliers get £ from a designated government. fund as part of a CfD, and if they go down, suppliers pay back to the fund.

Advocated by some energy suppliers. Not significantly different to the social tariff but paid by the exchequer rather than a redistribution of costs across energy bills.

Will need new legislation

Gives certainty on cost of energy bills and allows households to manage their disposable income better

Depending on the level that the price is set, other targeted support measures could be rationalised.

If combined with removing levies off bills, could see a considerable reduction and stabilisation of energy bills, completely cushioning vulnerable customers against bill rises.

If the cap is sustained over a reasonable time frame, it could be fiscally neutral as renewables have a depressing effect on wholesale prices.

Reduces the burden of hedging for suppliers against a specific consumer base

A form of price control which is anathema to many in government and the leading opposition

Significantly undermines the ‘supposed’ benefits of competition and switching.

The cost to the exchequer is unpredictable and could be considerably high during significant market volatility.

While the policy can be fiscally neutral, consistently low wholesale prices could have the perverse effect of imposing higher bills on vulnerable customers, which could be argued is the price of this stabilising effect.

A designated public procurement institution participates in energy market and hedges on behalf of a targeted consumer base by procuring long term supply contracts (or Asian options as this MIT paper suggests)

Public procurer sets a fixed ‘strike price’ and a set volume of energy (MWh) to procure based on an expected demand profile of the consumer base it is trying to protect. if the average spot price of energy over the course of a specific period (say, a month) goes beyond the strike price, the payoff would be the difference between the strike price and the average market price.

Energy generators participate in auctions to supply at fixed prices set by the purchasing public entity, for several years ahead. The premium associated with fixing prices is passed on through the standing charge on energy bills of the impacted consumer base.

This is in some ways similar to the ‘green power pool’ idea except it retains the exposure of counterparties to short term market signals (eg. curtailing generation in times of negative pricing)

Stabilises prices for a specific customer base over a period of time (>5 years) without artificially fixing the price

Not too dissimilar from the administrative wholesale price described above but incentives for demand response to price signals remain in the short term.

Retains the integrity of the market and cost reflectiveness but introduces a regulated, public entity to hedge on behalf of vulnerable consumers.

Cost of hedging i.e. premiums might remain high for the foreseeable future, resulting in no considerable reduction in energy bills for targeted customers.

Might encourage other suppliers to ignore this market segment altogether.

Subsidising price setters to artificially reduce their generation cost and thereby reduce wholesale price and the inframarginal rents that cheaper, and often renewable energy generators, accrue

Involves subsidising gas and coal power plants by capping their generation costs and paying for it through additional government borrowing

Proposed by Spain and Portugal as a short term response to the crisis

Reduces the impact of high gas prices on energy bills, given the current market design

Reduces the inframarginal rent for non-gas, non-CfD generators which the govt. Is currently trying to levy a windfall tax on.

Subsidy for gas, either short term or long term, is an incentive to sustain its consumption when it should in fact drive cleaner alternatives.

Creates perverse incentives by pushing gas up the dispatch merit order, ahead of cleaner alternatives.

Only deals with gas, which is the current driver of high energy prices but does not address the causes of any other future volatilities.

Once committed can be politically difficult to walk away from.

Proposed by RAP, this measure temporarily decouples wholesale prices with gas prices while setting a cap on wholesale prices based on the current price cap, an administered price or the price of the most expensive ‘non-gas’ generator.

The mechanism is for price shocks and is triggered when non-gas generators are expected to make abnormal revenues (2 – 3x their levelised cost).

Has the benefit of reducing prices universally and not just for a targeted group

Addresses the issue of marginal generators such as gas plants from setting the clearing price for the wholesale market without fully undermining the investments made in renewable energy technologies through their inframarginal rents.

Is temporary by design and the mechanism ends once prices fall down within a moderate range.

It is focused on price spikes but during periods of sustained high prices, it might change the incentive structure for renewable generators.

A new, flexible energy element of UC

An energy element of UC introduced, which is pegged to the price cap. As and when the cap goes up, so does the standard allowance on UC, automatically, and vice versa.

Benefit cap is lifted and is implemented alongside auto enrolment of UC.

Is much more price reflective of the changes to the cap every three months as opposed to UC uplifts in April every year in line with inflation in September the year before.

Targets some of the most vulnerable households that are in receipt of means tested benefits and is very easy to roll out

Politically palatable when considering that this does not necessarily contribute to a permanent rise in UC allowance (like the £20 uplift during the pandemic)

Targeted support measure thereby missing out on the wider consumer base that are currently facing very high energy bills.

Variable, progressive tariffs based on usage where higher energy usage is charged higher per unit consumed

A specified block of energy, deemed essential for daily needs, is free, with a steep but progressive rise in tariffs after that. Proposed by the Fuel Poverty Action coalition as part of their Energy 4 All campaign.

Scheme could be made more targeted with the free block of energy offered to a specific group (eg. fuel poor)

Offers a universal minimum energy for all households for free, ensuring no cases of self disconnection or creating conditions for eating vs heating choices.

Implicit incentive to keep energy consumption low and therefore drive energy efficiency measures.

High energy consumption of households with a disabled member, multiple children, electrically heated homes or an energy inefficient property could suddenly result in a steep rise in the cost of energy (assuming no additional support measures are made available).

Those on pre-payment meters might still lose out with much higher tariffs as a result of enhanced cost recovery measures from suppliers.

Will require a full roll out of smart meters but would possibly make the introduction of time-of-use tariffs redundant.

Invite existing renewable and nuclear generators, currently benefiting from the RO framework, to enter into new long term contracts through the CfD auction mechanism. This could involve the introduction of a new ‘pot’ that is dedicated to legacy renewables.

Price stability of a CfD mechanism might be more attractive for some generators than the ongoing volatility, despite profiting from very high rents currently.

Proposed auctions would deliver even lower prices than the latest round of auctions as generators would have serviced a good portion of their debt already.

If current high wholesale prices remain in place, this could result in considerable savings for consumers.

Strike price for CfD auctions could be set at levels considerably higher than wholesale prices, leading to an overall loss for consumers. These are in scenarios where wholesale prices plummet after implementing this scheme.

Participation is very poor from legacy renewables

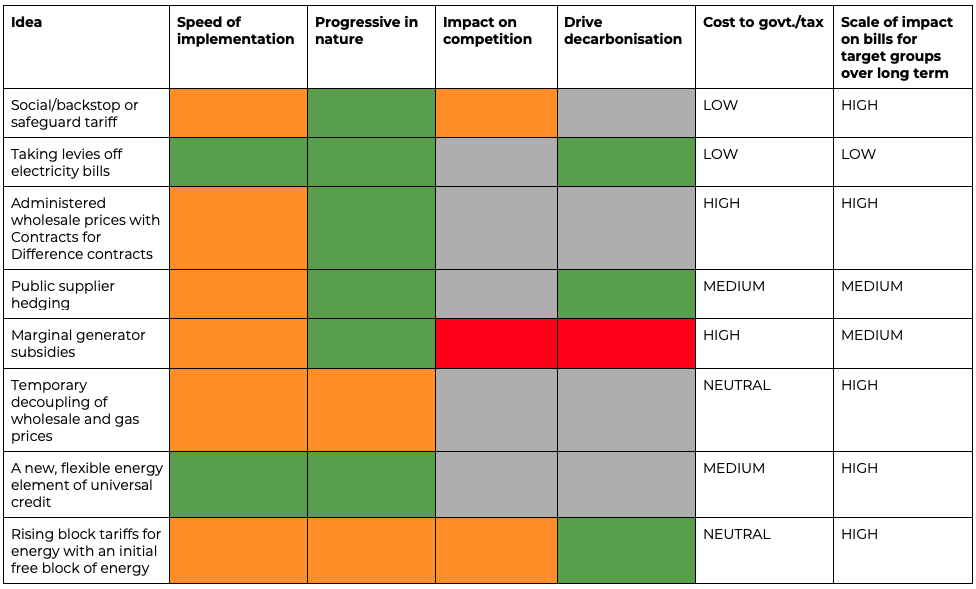

The following table further contrasts the above measures against a set of key indicators.

Key:

Intervention in the energy markets is always fraught with unforeseen and unintended consequences. However, for political leaders, particularly in Europe, the desire to be seen as doing something is high, potentially leading to the undoing of a lot of the existing market regime and state aid rules. Some of the above ideas carry a time lag and will require detailed consultation with stakeholders before being implemented, so are not suitable as short-term support measures. Therefore, direct fiscal support for households remains the most effective and efficient way of dealing with this crisis in the next 3 – 6 months. As NEF has argued before, boosting benefits further along with specific targeted interventions will again be necessary.

The Chancellor’s support package in May was based on the price cap reaching £2800 in October, but those forecasts are already out of date with new figures indicating a rise to £3000 with a further jump to roughly £3300 in January. Ordinary families cannot withstand such a shock, especially considering the steep rise in the price of other essential goods. Removing the two-child limit and the benefit cap for those on means-tested benefits are additional measures the government has to urgently implement to avoid driving hundreds of thousands into deeper poverty.

The choice for the new government and a new chancellor is clear: prioritise short-term interventions that put money into the pockets of those who need it most or, as Martin Lewis warns, face a winter of discontent.

If you back a recovery plan based around great public services, protecting the planet and reducing inequality, please support NEF to build back better.