Andrew Sprung writes about the ACA. I read him quite often as his posts are expert analysis of the ACA and healthcare. Mostly recently this commentary was posted by Andrew on the benefits of getting a Bronze plan as opposed to a Gold plan if facing large out of pocket expenses (premiums + deductibles). “XPOSTFACTOID” Mostly about the ACA: Obamacare to Trumpcare. Bronze plans are terrible. Bronze plans are often the best choice. In discussion of the ACA marketplace (and health insurance generally), deductibles are often used as a stand-in for out-of-pocket costs. Now here cometh David Anderson to remind us that a plan’s maximum out-of-pocket cost (MOOP) can be just as important — and that the MOOP often does not particularly correspond to metal level.

Topics:

run75441 considers the following as important: Healthcare

This could be interesting, too:

Bill Haskell writes Families Struggle Paying for Child Care While Working

Joel Eissenberg writes RFK Jr. blames the victims

Joel Eissenberg writes The branding of Medicaid

Bill Haskell writes Why Healthcare Costs So Much . . .

Andrew Sprung writes about the ACA. I read him quite often as his posts are expert analysis of the ACA and healthcare. Mostly recently this commentary was posted by Andrew on the benefits of getting a Bronze plan as opposed to a Gold plan if facing large out of pocket expenses (premiums + deductibles).

“XPOSTFACTOID” Mostly about the ACA: Obamacare to Trumpcare.

Bronze plans are terrible. Bronze plans are often the best choice.

In discussion of the ACA marketplace (and health insurance generally), deductibles are often used as a stand-in for out-of-pocket costs. Now here cometh David Anderson to remind us that a plan’s maximum out-of-pocket cost (MOOP) can be just as important — and that the MOOP often does not particularly correspond to metal level.

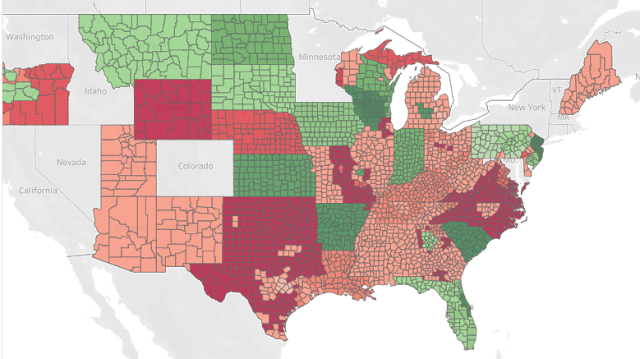

The highest allowable MOOP at all metal levels is $8,150 (a travesty by international rich country standards). Here is David’s mapping of the range of MOOP for gold plans in HealthCare.gov states. Dark green is $2,500 MOOP; dark red is $8,150.

As David points out, bronze plans will be a better deal for anyone who knows they’ll hit the out-of-pocket max. As he’s pointed out elsewhere (and in passing here), it takes a lot more spending to hit the high max in a gold plan — say, $30,000 — than in a bronze plan. That’s because once you meet your deductible (likely to be relatively low in a gold plan with high MOOP), a high percentage of ensuing costs will be covered in a gold plan until the MOOP is reached, at which point coverage goes to 100% for ensuing costs (if you stay in network).

And as I’ve noted before, for an unsubsidized enrollee, the window in which the lower overall out-of-pocket spending in a higher metal level will outstrip the higher premium cost is usually pretty narrow. Where premium pricing is more or less proportionate to actuarial value (and in the ACA marketplace, it often isn’t), you have to spend a good amount on healthcare, but not as much as a short hospital stay will likely cost, for a higher metal level plan to pay off, especially one with a higher MOOP. (As health insurance Jenny Hogue points out, a three-day hospital stay will likely max out any MOOP.)

This leads to two dissonant conclusions:

1) By international standards bronze plans are a travesty. Deductibles average around $6,000, MOOP around $7,000. That’s a huge amount of financial exposure for “insured” not-wealthy people — leaving aside further exposure to cost through balance billing, narrow networks, and insurers’ refusal to pay for prescribed treatments.

2) For individual market enrollees who earn more than 200% of the Federal Poverty Level and so are not eligible for strong Cost Sharing Reduction subsidies (which keep MOOP under $2,500 for silver plans), bronze plans are usually the rational choice. That may not be true where ACA marketplace quirks throw up gold or silver plans at a steep discount, or for people with substantial chronic healthcare costs but no catastrophic costs, but it’s true more often than not. It’s especially true in the era of silver loading*, when bronze plans are free or super-cheap for many people with incomes in the 200-400% FPL range. Witness the exodus out of silver since 2017 (the last year with no silver loading) among enrollees in that income range:

Enrollment by Metal level at 201-400% FPL, 2017-2019

HealthCare.gov states:

The steep increase in gold as well as bronze enrollment reflects the impact of silver loading, which in many areas has made gold plans available for less than the cost of benchmark silver. Bronze has become the metal level of choice at this income level, however — and all the more so for the unsubsidized.

In the runup to ACA passage, various conservative and maverick observers floated plans to federally fund catastrophic insurance, sometimes with an associated commercial market for coverage below the catastrophic threshold. Bronze plans are essentially catastrophic coverage. In the silver loading era, bronze plans are available free to over half of on-exchange enrollees (enrollees with incomes below 200% FPL fortunately have mostly stuck to silver plans enhanced with CSR, which reduce out-of-pocket costs to something approaching income-appropriate levels).

Healthcare advocates in various states are considering and proposing various creative measures to boost health insurance access and affordability (see New Mexico). Question: could a state in which free bronze plans are widely available foster a commercial market or self-sustaining state-run plan offering supplemental first-dollar coverage, capped at, say, $5,000 or $7,000 coverage per year? Guaranteed issue, comprehensive coverage to that level — how much would it have to cost to be self-supporting?

UPDATE: As actuary Gabriel McGlamery points out, a straight-up capped-benefit plan offering comprehensive coverage to the coverage limit would be illegal, as only very limited plan types (listed here) are not subject to the ban on coverage caps. These include accident and specific illness plans, which are sometimes bundled together as supplement individual market coverage, as described here. Fixed indemnity plans are also allowed as supplemental plans if their benefits are not coordinated with any other plan.

P.S. Any state action of this sort to reduce high OOP in ACA plans would be a form arbitrage, taking advantage of pricing anomalies caused by silver loading. That is, if the federal government is offering 60% AV coverage at a steep discount, add some extra AV at cost. In some ways it’s easier to imagine a red state doing this — encouraging a medically underwritten supplemental insurance market.

Bronze Plans are Terrible. Bronze plans are often the best Choice, XPOSTFACTOID, Andrew Sprung, February 17, 2020