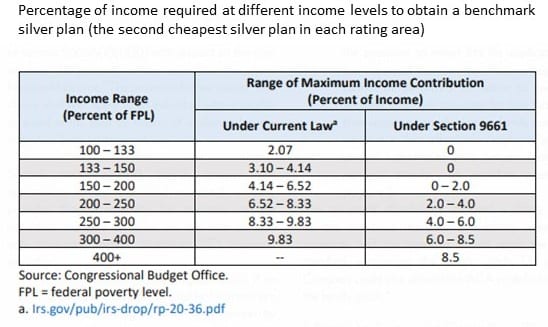

What I am writing about today is the up-and-coming changes to the PPACA resulting from the signing of the American Rescue Plan Act of 2021 by President Joe Biden. This is not Medicare-for-All or Single Payor; however, it is a big leap forward in making healthcare affordable for the next two years. Improved affordability will come with cost analysis and the impact on pricing and reduced administrative costs. I have touched upon those costs in early posts. Less Costly Healthcare Insurance for All Ranges The first chart shows “Before 2021 Covid Relief Bill passing” income percentages (under Current Law), and after the “Covid Relief Bill passes” income percentages (Under Section 9661). The Income Range sets the lower and upper parameters

Topics:

run75441 considers the following as important: American Rescue Plan, Healthcare, politics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

What I am writing about today is the up-and-coming changes to the PPACA resulting from the signing of the American Rescue Plan Act of 2021 by President Joe Biden. This is not Medicare-for-All or Single Payor; however, it is a big leap forward in making healthcare affordable for the next two years. Improved affordability will come with cost analysis and the impact on pricing and reduced administrative costs. I have touched upon those costs in early posts.

Less Costly Healthcare Insurance for All Ranges

The first chart shows “Before 2021 Covid Relief Bill passing” income percentages (under Current Law), and after the “Covid Relief Bill passes” income percentages (Under Section 9661).

The Income Range sets the lower and upper parameters (percentage) for income to qualify for a particular income range.

Please note the greater than 400% FPL Cost is capped at 8.5% of Income which was not available previously. Keep in mind an employer sponsored family healthcare plan is ~$20,000 annually .

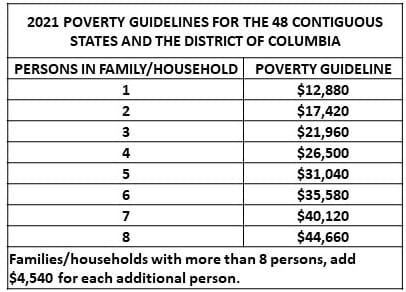

I have included household Poverty Guidelines by family size for the lower 48 states in the next chart. For Hawaii and Alaska, the parameters can be found at HHS Poverty Guidelines For 2021.

How this Bill Passed and More of Its Content

Simply speaking, Senate Democrats sent the American Rescue Plan Act of 2021 to the House. Republican’s are still working on their bill from 2008.

The American Rescue Plan Act of 2021 sent to the House reduces the percentage of income needed to buy a benchmark plan.

The benchmark Tier two Silver plan remains the same. High Actuary Value at incomes up to 200% FPL (94% or 87%). Low Actuary Value above the 200% income threshold (73% or 70%) . Incomes below 150% FPL are free.

The new subsidy schedule extends through 2022. A new Congress with courage will have to extend it via subsequent legislation. Or Congress may be bold enough for Single Payer.

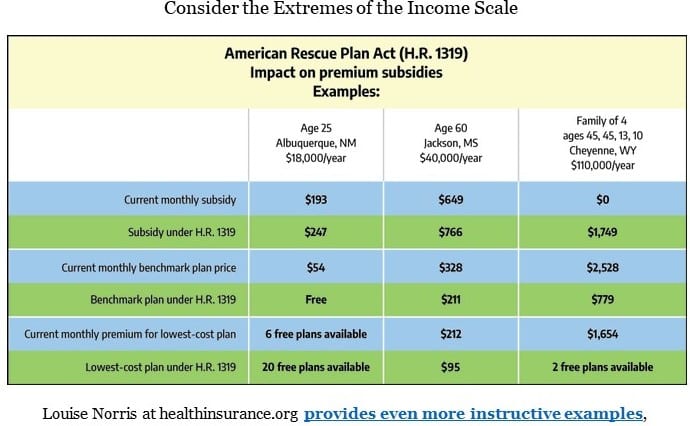

The Cost Factor

Examples; ACA versus American Rescue Plan

If Extended beyond 2 years there could be 3 million new enrollees” in the next 3-4 years under this subsidy schedule. This is in line with CBO projections. The 3-million is more than a quarter of the currently uninsured who will become subsidy-eligible (half of which will come from the 3.4 million uninsured as taken from 400% FPL to Kaiser’s estimate of 8.9 million current subsidy-eligible uninsured).

Seventy-five percent of the uninsured haven’t signed up in the past due to cost. Forty Percent of the these uninsured are eligible for free coverage, zero-premium high-deductible bronze plans. When asked, if they shopped in last two years? . . . 75% have not done so(KFF Cynthia Cox).

In explaining the lack of knowledge, KFF’s Cynthia Cox points to news coverage touting unsubsidized premiums which average $478 per month for a Tier Two benchmark Silver plan for a 40 year-old.

“People don’t know that almost no one pays that. And as several veteran enrollment assistors have told me, the toxic Republican vilification of marketplace coverage over many years still has its effect: throughout the red states, there are still many uninsured who won’t touch “Obamacare.”

While Biden’s American Rescue Plan is an improvement, there is still a high cost factor for everyone and those > 400% FPL even with an 8.5% cap. It is better than the the absolute cliff before but the cliff still exists.

Bring on Single Payer!

Joe Biden’s American Rescue Plan Act of 2021