Academic Agent lost a bet to me on Twitter and was forced to respond to my post here on Austrian economics and the reality of relative price rigidity. He has now produced two videos in this debate.Here is Academic Agent’s first video response to my post:[embedded content]Before he uploaded the video, I predicted that his video would contain the following:(1) he would misrepresent the actual theories of Austrian economics;(2) he would attack straw-man misrepresentations of my post;(3) he would focus on minor arguments and weak evidence and largely ignore major arguments and strong evidence. These predictions are largely correct.First, Academic Agent misrepresents my argument and states that I think the word “rapidly” in relation to price flexibility means I think prices must change

Topics:

Lord Keynes considers the following as important:

This could be interesting, too:

Robert Vienneau writes Austrian Capital Theory And Triple-Switching In The Corn-Tractor Model

Mike Norman writes The Accursed Tariffs — NeilW

Mike Norman writes IRS has agreed to share migrants’ tax information with ICE

Mike Norman writes Trump’s “Liberation Day”: Another PR Gag, or Global Reorientation Turning Point? — Simplicius

Here is Academic Agent’s first video response to my post:

Before he uploaded the video, I predicted that his video would contain the following:

(1) he would misrepresent the actual theories of Austrian economics;These predictions are largely correct.

(2) he would attack straw-man misrepresentations of my post;

(3) he would focus on minor arguments and weak evidence and largely ignore major arguments and strong evidence.

First, Academic Agent misrepresents my argument and states that I think the word “rapidly” in relation to price flexibility means I think prices must change “immediately.” He is a pure liar. I do not interpret “rapidly” to mean “instantly” or “immediately,” but reasonably quickly in the short run (which might be days or perhaps a few weeks).

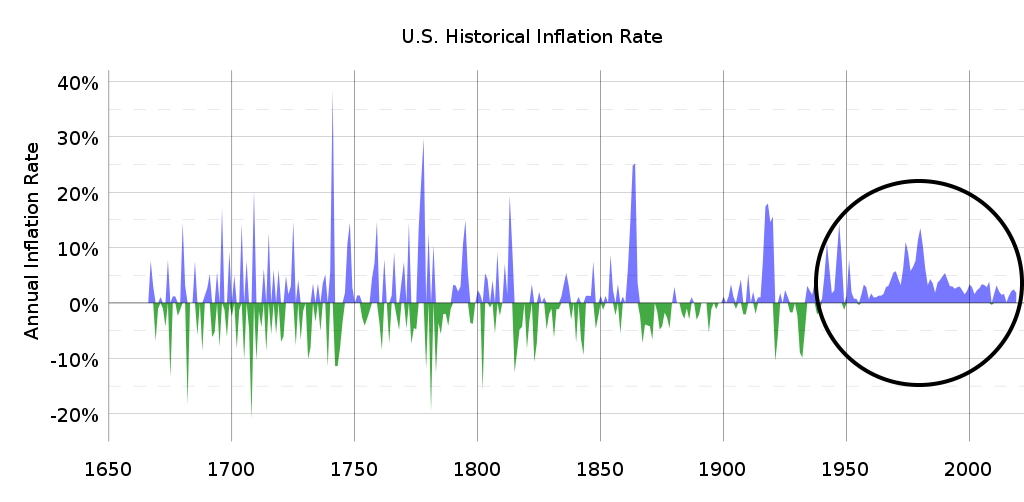

In my original bet with Academic Agent on Twitter, I asked him to also comment on this graph of historical inflation rates in the US:

The graph shows, after the late 1930s, a sharp decrease in volatility of price movements as compared with the 19th century, and the virtual disappearance of deflationary episodes even during recessions.

In short, this is clear, explicit, definitive proof that we live in a world of relative price rigidity, as stated in the quotation of Lachmann. You could find similar graphs from every Western nation where the same trend is perfectly evident.

Academic Agent chose to ignore this graph and the evidence it provides, which can only demonstrate what a dishonest hack he is, and proves that he chose to ignore the strongest evidence. Later he was forced to produce a second video dealing with this point, as we will see below.

Of the twelve quantitative studies on the average duration of price changes I cited, Academic Agent picked three, and ignored the most recent, best studies with massive data sets. He then selected some random commodities in his three cherry-picked studies and attempted to show that their price movements were driven by demand changes by reference to their sales data over time, correcting, he believed, for the rise in the general price level in particular relevant time periods.

But his attempt to disprove my original post by this tactic is utterly flawed. Academic Agent examined a handful of prices of some goods like steel and magazine prices and thought he showed that their price rises were determined by demand changes. But he simply begged the question and refused to consider that the price changes in question may have been caused simply by changes in the total average unit costs of the producers, which is entirely in line with cost-based mark-up pricing theory.

Worse still, Academic Agent refuses to even state whether he thinks cost-based mark-up prices exist or not. For a very long time on Twitter, Academic Agent vehemently refused to accept that cost-based mark-up prices even exist, then in the face of massive evidence presented to him hinted that maybe they exist, and then when pressed again evaded the issue or reverted to his original absurd position that they do not exist.

Notably, in an act of obvious dishonesty, he completely ignored the best evidence in the quantitative studies I cited. Consider these studies:

(1) Baudry, Laurent, Le Bihan, Hervé, Sevestre, Patrick, and Sylvie Tarrieu. 2004. “Price Rigidity. Evidence from the French CPI Micro-Data,” ECB, Working paper series No. 384There is not a word about these in Academic Agent’s video, and, worse still, he completely rejected the qualitative studies of face-to-face interviews, surveys and questionnaires of business-people, managers, CEOS and price administrators on the absurd objection that none of these studies has any validity.

https://ideas.repec.org/p/ecb/ecbwps/2004384.html

This paper uses a large dataset of prices from the non-farm business sector of the French economy. More than 750,000 products were tracked for price changes (that is, the time duration between two price changes of a product) from July 1994 to February 2003 (Baudry et al. 2004: 5). This study finds significant rigidity of consumer prices. The weighted average duration of prices was 8 months, but the authors calculate that extension of the data to include the whole French CPI would yield a weighted average duration of price change higher than 8 months (Baudry et al. 2004: 5–6). The study found that service prices are especially sticky: they typically last for a year (Baudry et al. 2004: 6).(2) Dhyne, Emmanuel, Álvarez, Luis J., Le Bihan, Hervé, Veronese, Giovanni et al. 2006. “Price Changes in the Euro Area and the United States: Some Facts from Individual Consumer Price Data,” The Journal of Economic Perspectives 20.2: 171–192.

This paper analyses large quantitative price data sets from numerous European nations, including Austria, Belgium, Finland, France, Germany, Italy, Luxembourg, the Netherlands, Portugal, and Spain. The major finding is that in the Euro area that average duration of price changes is 13 months (Dhyne et al. 2006: 176). The sectors that have the most price rigidity are services, non-energy industrial goods, and even processed food (Dhyne et al. 2006: 189). In particular, the services sector (the largest sector in most nations today) shows very strong downwards price rigidity: on average, only 2 price changes out of 10 are downwards in the services sector (Dhyne et al. 2006: 181). On average throughout various sectors, just 4 price changes out of 10 are decreases in prices (Dhyne et al. 2006: 180), which shows that there is a bias towards price rises in modern capitalist economies.

What is especially ridiculous here is that, in the past, Academic Agent has rejected a study by A. Blinder called Asking about Prices: A New Approach to Understanding Price Stickiness (1998) with the objection that its sample size was only 200 US businesses. Yet Academic Agent himself makes the sweeping conclusion that prices are flexible with a sample size of less than a dozen products!!

Moreover, there is another devastating problem with Academic Agent’s method of selecting of random prices in the video and analysing them, which is from the perspective of Austrian economics itself.

First, Austrians believe in Cantillon effects. A Cantillon effect is the idea that price level changes caused by increases in the quantity of money depend on the way new money is injected into the economy and where it affects prices first. Austrians think that new money spreads out altering the level of prices and structure of relative prices in a non-uniform way. Another way of saying this is that, although prices rise as the quantity of money increases, contrary to the naive Quantity Theory of Money, prices do not rise proportionally, but in a complex manner that depends on who received the money and how they spent it. (I would point out that, to the extent that money supply changes can induce price changes, Cantillon effects no doubt do happen, and in this respect Cantillon effects can be real, but the whole Quantity Theory of Money is itself flawed, so this point is rendered moot.)

But Academic Agent makes the assumption that all prices must have risen at the same rate as the general price level over time, which his own Austrian theory tells him is false.

Thus Academic Agent has fallen back on a vulgar Quantity Theory of Money view of inflation, which even the Austrian economists he appeals to reject.

So even if Academic Agent could overcome the devastating contradictions and problems with his original video, he still would not prove that most prices are rapidly responsive to demand changes, since, logically, his method for analysing how prices changed in response to demand is invalid by his own Austrian theory!

After selecting some random commodities like magazine prices and attempting to show their price movements were driven by demand changes, Academic Agent then absurdly claims victory and made the conclusion to his first video here:

As we can see, Academic Agent’s conclusion – which is a questionable sweeping generalisation given his tiny sample size even if we put aside the other criticisms – is that “Fluctuations in supply and demand are reflected in real-world prices” (note carefully that he specifies he really is talking about real-world prices here).

But within a few hours his whole conclusion collapsed when I challenged him on Twitter to explain the graph of historical US inflation rates above and to explain the downwards price rigidity clearly evident in the graph.

His reply was predictable:

So Academic Agent effectively admitted that he himself thinks that central banks, through their money creation, impede downwards price flexibility in a very significant way.

I then challenged him to explain how he could possibly defend these two mutually contradictory propositions:

(1) real-world prices are highly flexible upwards and downwards in response to supply and demand changes as required in Austrian economics, orOf course, this charlatan pretended there was no contradiction, refused to even state which one he thought was correct.(2) there is massive downwards price rigidity caused by central banks.

Later he produced this comical second video in response to the paradox:

In video 2, Academic Agent now utterly contradicts his original video and argues that only purely abstract or imaginary prices as imagined in Austrian economics in the absence of central banks are highly flexible upwards or downwards in response to demand changes.

But in his original video he was perfectly explicit that he was attempting to defend the proposition that real-world prices (not abstract or imaginary ones) were flexible upwards or downwards in response to demand changes:

So Academic Agent has switched the terms of his argument in the second video in a blatant contradiction analogous to (but not exactly the same as) the Fallacy of Equivocation. In fact, Academic Agent has committed a grossly dishonest violation of basic standards of honest argumentation, because in the standard Fallacy of Equivocation a crucial term is used in a slippery, non-explicit manner where it can have ambiguous or multiple meanings. But Academic Agent is such a lazy hack and charlatan he blatantly switches the explicit meaning of the key term in the debate between the two videos.

In the first video, the key term is “real-world prices” (that is, actual prices in the real world). In the second video, Academic Agent switches to “abstract or imaginary prices” as imagined in Austrian economics in the total absence of central banks (and presumably other state interventions).

Anybody rational can see that this is a contemptibly dishonest intellectual tactic that allows him to evade answering the question whether real-world prices are actually and really highly flexible, both upwards and downwards, in response to demand changes.

Finally, even though there certainly is significant relative price rigidity downwards, the fundamental cause of this is not, as Academic Agent thinks with his lazy Quantity Theory of Money fable, the money creation of central banks.

In reality, the fundamental driver of relative price rigidity downwards are these two factors:

(1) the institutional reality that most prices are cost-based mark-up prices with a bias to move upwards rather than downwards, andThe fact is that money supply growth is simply an intermediary factor here.(2) widespread relative downwards money wage rigidity, which feeds into (1).

Long-run inflation of the money supply is necessary to sustain long-run inflation, so, in that respect, central-bank money expansion is a necessary condition for long-run inflation, but central-bank money creation is not the primary causal origin of upwards movements in prices and downwards relative price rigidity. The primary causal factors are the two listed above. So Academic Agent doesn’t even understand the fundamental cause of downwards relative price rigidity. Instead, he is a lazy Quantity Theory of Money advocate. He is even too stupid – as we have seen above – to understand and properly apply the Austrian objections to the Quantity Theory of Money via Cantillon Effects in his analysis!

If Academic Agent were an honest intellectual, he would be capable of giving direct, explicit, non-evasive answers to these questions:

(1) do cost-based mark-up prices exist in the sense described here?Of course, Academic Agent will never provide clear answers to these questions, because being minimally honest and clearly answering them would refute his two videos.(2) if Academic Agent thinks cost-based mark-up prices exist, to what extent are they used in modern Western market economies?

(3) why did Academic Agent ignore the best, most recent quantitative studies I cited in my original post, especially Dhyne et al. 2006 and Baudry 2004, which both show significant price rigidity?

(4) Are real-world prices (not abstract or imaginary prices in the absence of central banks) highly flexible downwards or not, given his Quantity Theory of Money view, in the presence of central banks?

(5) if the answer to question (4) is “no,” then how can actual, real-world prices be highly flexible, both downwards and upwards, in response to demand changes?