I wrote about how high house prices are correlaed with poor growth (partly because that which has gone up goes down). The data set was heroically collected by Jorda, Schularick, and Taylor who also used it for a paper which is actually very worth publishing (and published here). They find that high housing prices and rapid growth of total credit are correlated with greater severity and duration of the next recession.. I wonder if the bubble and credit growth variables are useful in predicting the occurance of a recession (as well as the severity and duration once one comes). I guessed that it is hard to predict turning points — in particular high asset prices & rapid expansion of credit may imply that there is trouble ahead, but not how far ahead. But I

Topics:

Robert Waldmann considers the following as important: US/Global Economics

This could be interesting, too:

Joel Eissenberg writes How Tesla makes money

Angry Bear writes True pricing: effects on competition

Angry Bear writes The paradox of economic competition

Angry Bear writes USMAC Exempts Certain Items Coming out of Mexico and Canada

I wrote about how high house prices are correlaed with poor growth (partly because that which has gone up goes down). The data set was heroically collected by Jorda, Schularick, and Taylor who also used it for a paper which is actually very worth publishing (and published here).

They find that high housing prices and rapid growth of total credit are correlated with greater severity and duration of the next recession..

I wonder if the bubble and credit growth variables are useful in predicting the occurance of a recession (as well as the severity and duration once one comes).

I guessed that it is hard to predict turning points — in particular high asset prices & rapid expansion of credit may imply that there is trouble ahead, but not how far ahead. But I couldn’t resist a logit with dependent variable “recession” for your definition of recession — a decline in real GDP starting in year t. Also (guessing it would work better) I looked at recession3 which is a peak in the current year or one of the two following years and recession5 which is a peak in the current year or one of the four following years..

To my surprise, the variables work really quite well I think (not surprisingly better for recession3 and recession5).

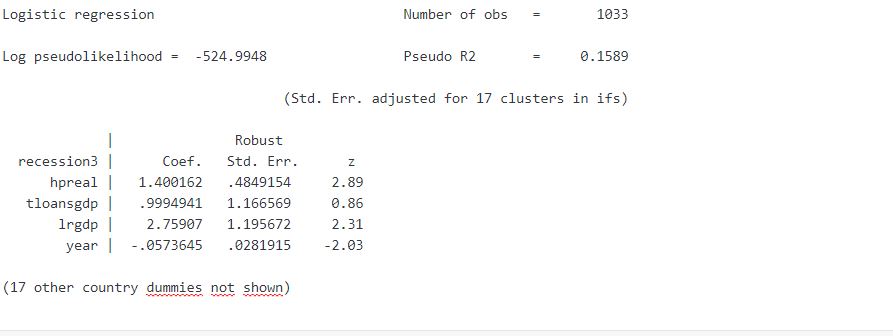

for recession 3 (year to year decline starting in any of three years of real gdp

logit recession3 hpreal tloansgdp lrgdp year cn* if year>1945, cluster(ifs)

hpreal is the nominal price of housing /cpi, tloansgdp is total loans/gdp, lrgdp is ln(rgdp per capita), there are country dummies

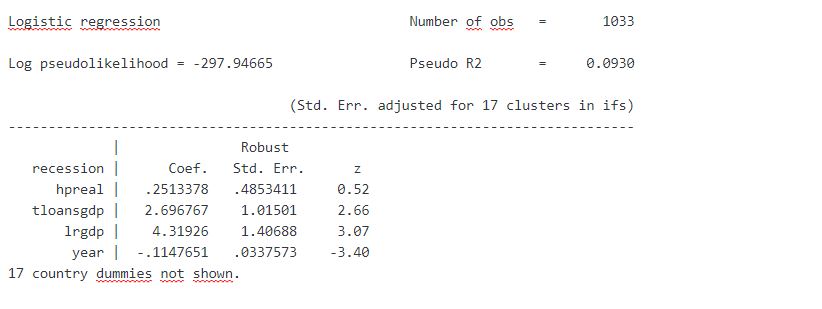

or just for recession (real gdo decline current year to next)

. logit recession hpreal tloansgdp lrgdp year cn* if year>1945, cluster(ifs)

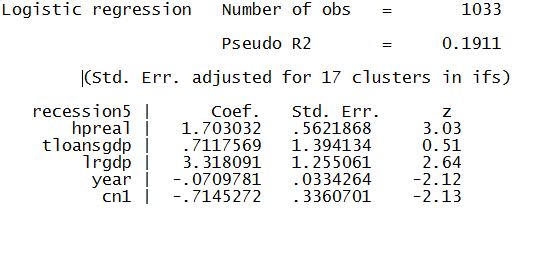

And with recession5

It works a little bit better if hpreal is filtered with a Hodrick Prescott filter (smoothing parameter from 100 to 4000 makes not so much difference) and the stationary part used in the regressions.

The index (x beta from the logit) makes it possible to classify years as preceeding recessions or not (again better for recession in next 3 years and better still recession in next 5 years).

The AUC (area under the curve) statistic gets as high as 0.8 for filtered hpreal (smoothing 1600) and recession5 — 0.5 is the expected value if the classification is random (if the index is worthless) and 1 means perfect classification.

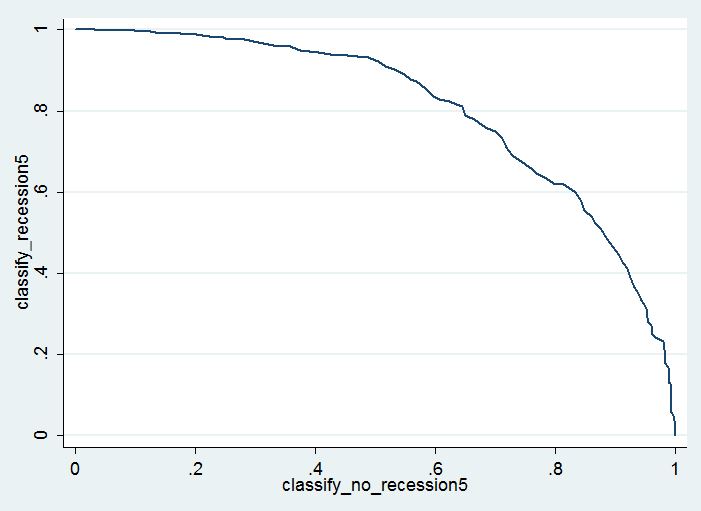

This is the star peforming correct classification frontier from

logit recession5 hpreal_1 tloansgdp lrgdp year cn* if ok, cluster(ifs)

The area under the curve is the statistic called AUC and, in this case is equal to 0.8025378

Correct classification frontier was a new concept for me (it seems that doctors talk about it a lot). It is generated by starting with a very low cutoff A and saying a recession will come if xbeta>A then moving up the cutoff A. So for very low A all recessions are called so correctly classified, but all years not followed by a recession in 5 years are miss classifiied. As A slides up to infinity it goes to all non recessions are correctly classified and no recessions are correctly classified.

The curve shows that a value so that half of recessions are predicted, only 10% of years not followed (within 5 years) by a recession are false alarms.