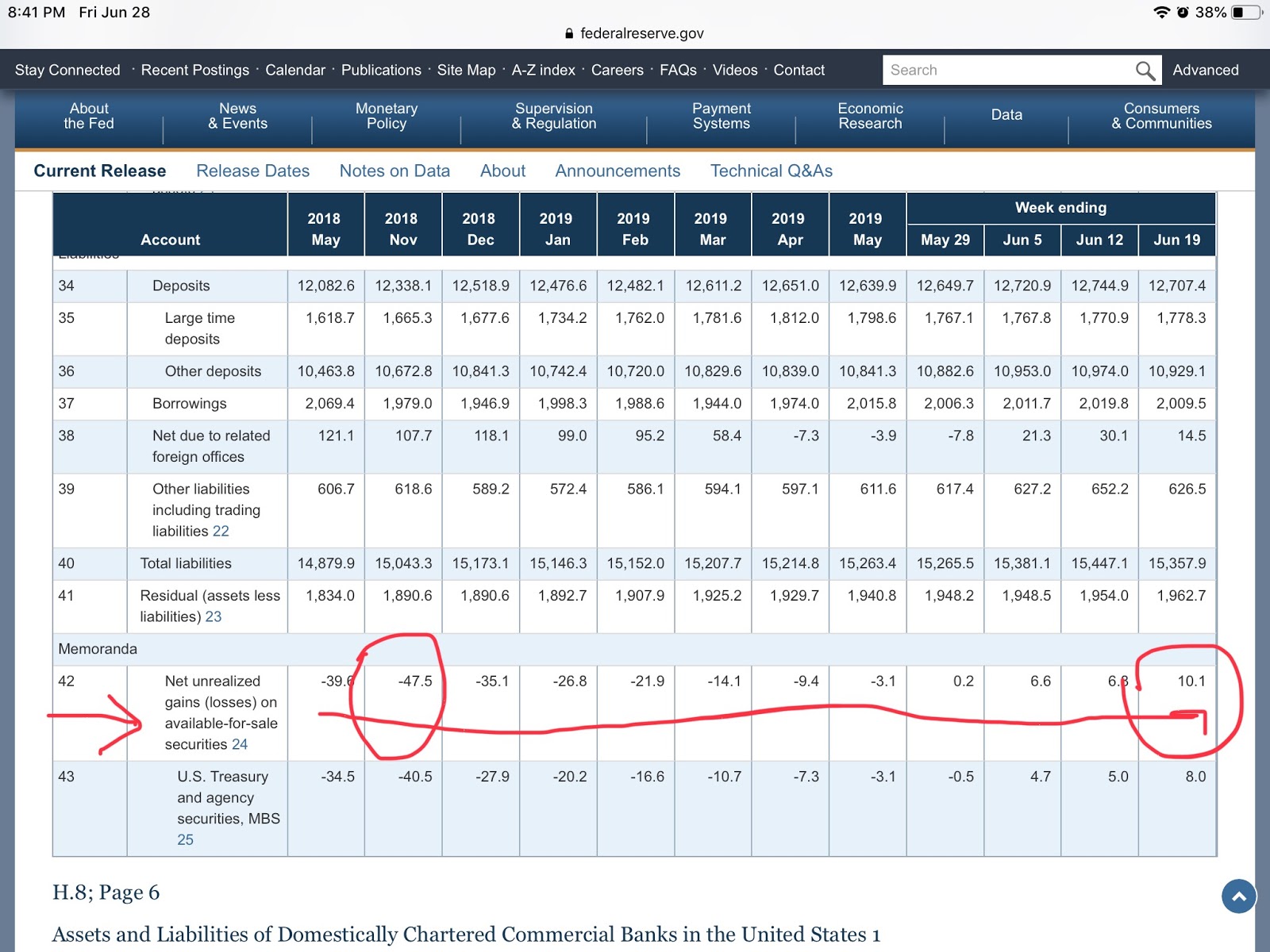

Cut below from today's nsa H.8 report showing 'Unrealized Gain (Loss) on Available for Sale Securities': You can see how Fed interest rate increases in 2018 caused a discount in the $trillions of CCAR required out-sized Tier1 quality Bank Assets to a near B LOSS by the time of the last December rate increase in late Q4 of 2018; and the corresponding reduction in equity share index prices where we saw those indexes off about 20% by Christmas Eve from the previous Q3 highs as this severe reduction in bank asset prices due to the change in the Fed's rate policy reduced the numerator in bank regulatory ratios which caused a corresponding reduction in total asset prices in the denominator in order to maintain a constant target regulatory ratio...Now compare that to today (June 19th) under

Topics:

Mike Norman considers the following as important:

This could be interesting, too:

Robert Vienneau writes Austrian Capital Theory And Triple-Switching In The Corn-Tractor Model

Mike Norman writes The Accursed Tariffs — NeilW

Mike Norman writes IRS has agreed to share migrants’ tax information with ICE

Mike Norman writes Trump’s “Liberation Day”: Another PR Gag, or Global Reorientation Turning Point? — Simplicius

Cut below from today's nsa H.8 report showing 'Unrealized Gain (Loss) on Available for Sale Securities':

You can see how Fed interest rate increases in 2018 caused a discount in the $trillions of CCAR required out-sized Tier1 quality Bank Assets to a near $50B LOSS by the time of the last December rate increase in late Q4 of 2018; and the corresponding reduction in equity share index prices where we saw those indexes off about 20% by Christmas Eve from the previous Q3 highs as this severe reduction in bank asset prices due to the change in the Fed's rate policy reduced the numerator in bank regulatory ratios which caused a corresponding reduction in total asset prices in the denominator in order to maintain a constant target regulatory ratio...

Now compare that to today (June 19th) under 'debt ceiling!' conditions where the current fixed amount of risk free UST bonds are highly bid under fiscal deficit conditions and this has now swung to a $10B unrealized GAIN in these Tier1 quality asset prices for a net $60B swing in bank equity and the resultant increase of equity share index prices back to near the old highs of 3Q 2018 in the mid 2900s on S&Ps.

This portends a similar further increase adjustment of these 'unrealized gains' and thus a nice further increase in bank regulatory ratios to support increased bank asset prices (bullish) if there is a Fed policy reversal to a rate decrease as many predict at the July meeting.

We'll see...

Or.... this all just could be part of a giant dialectic trained Liberal Art moron figurative "neo-liberal conspiracy!!!"...

Or... as Tom posits 5 posts down thread.. these unqualified assholes currently administering our numismatic system are going to change the "framing" aka their figurative language and presto! this is somehow going to magically provide them with a proper and constructively useful understanding of the regulatory accounting abstractions involved...

TIP: I wouldn't hold your breath waiting for that one...