There are encouraging signs that Canada’s economy and labour market are improving after a period of stagnation brought about by the Bank of Canada’s aggressive interest rate hikes in 2022 and 2023. Newly released data for the third quarter of 2024 (July-September) shows the economy has continued to grow, albeit slowly. Consumer spending was the brightest light in the third quarter data: growing at an annualized rate of 3.5% (in real, inflation-adjusted terms), and constituting the largest single source of new demand. Stronger consumer spending is being supported by continued rapid growth in wages. Average wages are continuing to advance at annual rates of 4-5% (depending on the specific wage measure chosen). Wages remain strong despite the rise in unemployment since 2022 (from

Topics:

Jim Stanford considers the following as important: affordability, inflation, Uncategorized, wages

This could be interesting, too:

tom writes The Ukraine war and Europe’s deepening march of folly

Stavros Mavroudeas writes CfP of Marxist Macroeconomic Modelling workgroup – 18th WAPE Forum, Istanbul August 6-8, 2025

Lars Pålsson Syll writes The pretence-of-knowledge syndrome

Dean Baker writes Crypto and Donald Trump’s strategic baseball card reserve

There are encouraging signs that Canada’s economy and labour market are improving after a period of stagnation brought about by the Bank of Canada’s aggressive interest rate hikes in 2022 and 2023.

Newly released data for the third quarter of 2024 (July-September) shows the economy has continued to grow, albeit slowly. Consumer spending was the brightest light in the third quarter data: growing at an annualized rate of 3.5% (in real, inflation-adjusted terms), and constituting the largest single source of new demand.

Stronger consumer spending is being supported by continued rapid growth in wages. Average wages are continuing to advance at annual rates of 4-5% (depending on the specific wage measure chosen). Wages remain strong despite the rise in unemployment since 2022 (from 4.8% in July 2022 to 6.5% today), and the rapid slowdown inflation (now running at just 2% year-over-year).

This sustained strength in wages is surely causing much hand-wringing in both corporate boardrooms and at the Bank of Canada. It reflects the determined efforts of Canadian workers to win a fair share of the pie they produce: including through an upsurge in trade union action, and pressure (successful in most provinces) for significant increases in real minimum wages.

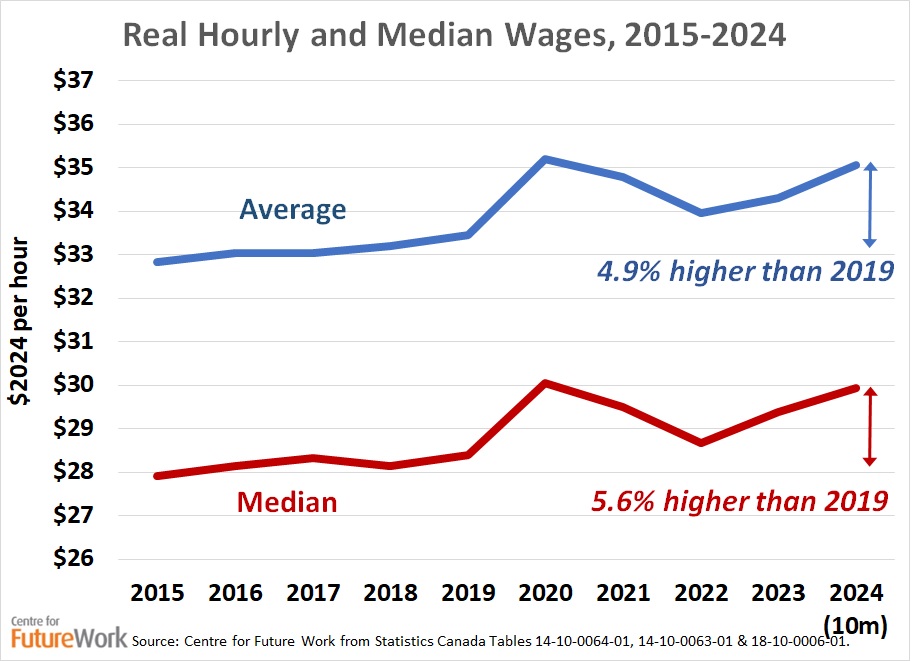

Wages have now been growing faster than prices for the last 18 months (and are currently growing more than twice as fast as the CPI). The resulting growth in the real purchasing power of wages has more than offset the decline in real wages that occurred during the initial outbreak of post-pandemic inflation.

Real wages are now about 5% higher than in 2019 (before the pandemic hit). Median wages have grown slightly faster than average wages, which indicates that proportional gains were somewhat stronger for lower-wage workers. (Please note that the 2020 peak in both series illustrated on the attached graph reflects a composition effect from huge job losses during the COVID pandemics, which disproportionately affected low-wage workers in retail, hospitality, and personal services; because of those job losses, the average wage for those who kept their jobs seemed to rise, but only until the return to work in those other industries pulled the average back down.)

The more-than-complete recovery of real wages in Canada after the pandemic is among the most successful of any industrial country. The U.S. is another country where real wages have recovered, even more strongly than in Canada – and, again, the strongest gains were received by lower-income workers. In contrast, real wages in most European countries and Australia remain several percentage points below pre-pandemic highs.

Thanks mostly to rapid growth in wages, household incomes have increased significantly in Canada in the last year: up by 7.5% in nominal terms, and over 4% in per capita terms. Again, that is significantly faster than inflation. That growth in incomes, combined with lower interest rates (which the Bank of Canada has now cut 4 times, for a total of 1.25 percentage points) and improving confidence, underpins relatively strong consumer spending. Barring another major global shock, it is likely these results will continue strengthening in coming months. (Unfortunately, there are many candidates for potential global shocks, ranging from Donald Trump’s threatened tariffs to escalation of war in the Middle East or Ukraine.)

These improving economic results stand in contrast, however, to a continuing sense in media and popular discourse that Canadians are angry and pessimistic about the economy. Political polls indicate the federal government is very unpopular (similar to incumbent governments in many other countries), with economic concerns seemingly top of mind for voters. Hyper-polarized social media, and the generally conservative bias of commercial mass media, reinforce the Conservative Party’s mantra that “Canada is broken” due to taxes, deficits, and general economic mismanagement.

This dissonance between positive economic indicators and persistent negative sentiment (especially expressed around politics) remains a puzzle to economists. Some traditional explanations do not hold water:

- Some argue that even if the average real wage has increased, that doesn’t imply that all workers experienced the same gains. Of course that is true – but the nature of an average is that there are almost as many people who got even better wage increases, as who received below-average gains. And the stronger growth in the median wage confirm that the gains, if anything, were even stronger for lower-wage workers.

- Some argue the consumer price index (CPI) used to compute real wages isn’t a ‘true’ measure of inflation. There are certainly some living costs (particularly housing) that are imperfectly captured by the CPI. But, again, there are also ways in which the CPI overstates true inflation (by ignoring the impact of quality improvements or substitution effects by consumers).

I believe the portrayal of rising real wages and strong household incomes above is an accurate depiction of what is happening in Canada’s economy. But as an economist, I cannot explain the contrast between those numbers and apparent sentiment. This negativity is especially visible in political surveys. In contrast, surveys of consumer economic sentiment (such as the Conference Board of Canada index) show gains in confidence this year.

A similar puzzle bedeviled the Democratic side in the recent U.S. election. U.S. economic performance since the pandemic was by far the strongest of any industrial economy (thanks in large part to very strong fiscal stimulus), and wide swaths of society experienced documented economic gains. But anger over the economy (perhaps fostered by negative reporting in the media, and virulent social and alternative media) was the major reason identified by researchers for gains in Republican support. (Claims of a Republican landslide, of course, are far-fetched: Trump received 50% of the presidential vote compared to 48.4% for Kamala Harris. Only in the U.S., with its byzantine electoral system, could this be construed as a “clear victory”.)

Two interesting journalistic reports have tried to make sense of the gap between economic outcomes and mass psychology. Ontario opinion pollster David Herle addressed the economic and psychological dimensions of the ‘affordability’ crisis in a recent episode of his influential podcast, The Herle Burly. The podcast featured myself and Armine Yalnizyan. Listen to our full discussion here.

In response to popular concerns about the cost of living, the federal government recently announced a temporary two-month ‘holiday holiday’ on GST payments on a selected range of products (including some prepared foods and children’s toys). In promoting this measure, Finance Minister Christia Freeland described it as an effort to combat the so-called ‘vibecession’: that is, persistent negative sentiment that, if it restrains consumer spending, could actually hold back the economy. (As noted above, consumer spending and reported sentiment are both growing, suggesting again that the ‘vibecession’ may be more of a concern in the political arena than in the actual economy.)

CBC journalist Abby Hughes pursued this idea of ‘vibecession’, including an interview with the U.S. economist who coined the term. She also interviewed me on the gap between economic and political indicators. Please see Hughes’ interesting feature article here.

Without being complacent about the challenges many workers face surviving in Canada’s harsh and unequal economy, the successes of Canada’s labour market institutions (like strong trade unions and higher minimum wages), which repaired real wages better & faster than most other OECD countries, should be acknowledged and, indeed, celebrated.

Defending and strengthening those institutions (which are now being targeted by Conservatives, and their “Canada is broken” mantra), and fighting for other policies to address bigger material challenges facing workers (especially the housing crisis, which needs a mass non-market strategy to resolve), may be a more progressive response to ‘vibecession’ than either temporary tax cuts or a simple-minded crusade to “throw the bastards out”.

The overarching task for trade unions and progressive political movements is to ratify the legitimate anger of working class people over their constrained life prospects (even if they are getting somewhat better, on average!), help them identify the main culprits for that situation (corporate power and greed), and then channel that anger in directions that will make life better for workers – rather than feeding a burn-it-to-the-ground mentality that is feeding right-wing populism here, and around the world.