Want a Public Option? Not So Fast, Say Health Insurers. Guess Who is Fighting It! Much of this is from an Op-Ed at MedPage Today authored by Wendel Potter. I have added to it as Wendel discusses the impact of insurance as a major influence on healthcare cost. It is one sided and the commentary ignores increased healthcare costs (pharma, hospitals, healthcare supplies, and doctors). I have touched upon both at MedPage Today and here. The nation’s largest healthcare insurers are making it clear to lawmakers of their opposition to campaign promises to establish a public option. Insurers are threating elected lawmakers with a massive, financed lobbying and PR campaign if they even try to pass a Public Option. In other words, the healthcare industry

Topics:

run75441 considers the following as important: Featured Stories, Healthcare, politics, public option

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Want a Public Option? Not So Fast, Say Health Insurers. Guess Who is Fighting It!

Much of this is from an Op-Ed at MedPage Today authored by Wendel Potter. I have added to it as Wendel discusses the impact of insurance as a major influence on healthcare cost. It is one sided and the commentary ignores increased healthcare costs (pharma, hospitals, healthcare supplies, and doctors). I have touched upon both at MedPage Today and here.

The nation’s largest healthcare insurers are making it clear to lawmakers of their opposition to campaign promises to establish a public option. Insurers are threating elected lawmakers with a massive, financed lobbying and PR campaign if they even try to pass a Public Option. In other words, the healthcare industry will lie to the public.

A Bit of Healthcare History Advocacy

I do not recall the minutia of the healthcare insurance campaign in the nineties’ however, this sounds like the threat of a similar campaign akin to what happened with Hillarycare and also the ACA. The healthcare insurance industry produced the infamous television the “Harry and Louise” commercial in an effort to rally public support against Hillarycare.

If the commercial was run today minus the voiceover (“The government may force us to pick from a few health care plans designed by government bureaucrats“), it would never occur to TV viewers Harry and Louise were talking about anyone other than their healthcare insurance company.

The Harry and Louise ad failed to recognize in a democracy, government was never supposed to be a “we and they” proposition. The ad made it such. The “we and they” relationship should have been between the patient and the healthcare insurer.

The healthcare insurance industry won in 1993 and we experienced a doubling of the costs of healthcare and similar increases in the insurance costs to pay for it.

With the passing of the ACA, healthcare insurance companies were given a 15 or 20% mark up on group or individual insurance to cover Overhead, etc. What is reflected by this markup are increases in costs of healthcare. For example, if Rituxan increases 17% (as shown in the link) from its whole sale cost from 2016 to 2018, the insurance companies take increases of 15 -20% of the difference between old and new whole sale price. In the link, you will see Rituxan had a price increase only due to new uses and not because of a cost increase to manufacture. Most recently, the cost of an infusion of Rituxan was $28,000 list. It is rent-taking.

Commercial Healthcare Insurance Approach

The Public Option is in its infancy in Colorado and Connecticut state legislatures and the legislators are hoping to establish state-based public option plans. All we are missing are the Congressional sycophants backing the healthcare Insurance lobby. I am confident it will come.

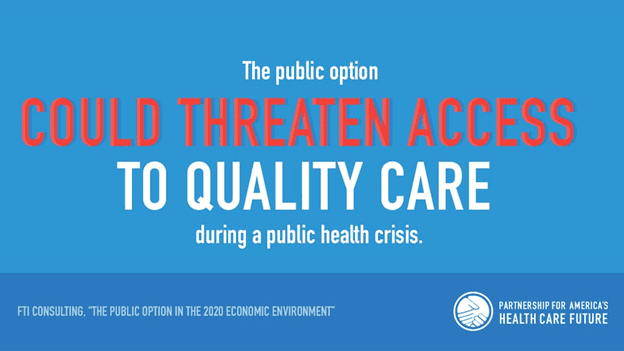

Partnership for America’s Health Care Future (PAHCF) produced the advertisement (shown above) in an attempt to spread fear about a public option in a similar manner as when the Harry and Louise ads did in 1993.

Comprised of a group of major pharmaceutical and insurance companies plus private hospitals, the Partnership had spent several months in 2018 lobbying members of Congress, running online ads, and working with the media. The effort was to drive down the popularity of Medicare for All which was gaining popularity in the Democratic party.

The Partnership membership included the American Medical Association (AMA), Pharmaceutical Research & Manufacturers of America (PhRMA), Federation of American Hospitals (FAH), and Blue Cross/Blue Shield. The money was spent in 2018 and political influence exerted in opposition to Medicare for All in Washington. The Partnership has now turned its attention to Colorado and Connecticut in opposition to a proposed Public Option.

Since then and on August 16, 2019: The American Medical Association withdrew from the Partnership for America’s Health Care Future. Politico. The AMA’s departure came after the expansion of opposition to Democratic healthcare proposals and the campaign against the public option and Medicare for All.

Why do insurers care so much?

Maintaining the status quo is profitable for the healthcare insurance industry. They do not want a new competitor disrupting the insurance market place especially one which streamlines the process as one payer to all hospitals like Medicare. The Public Option would begin to drive prices down and the fixed rate of 15 – 20% charges for group and individual insurance would be in jeopardy. What if the state tied in the Medicare or the VA pricing for drugs, operations, etc.?

The healthcare insurance industry is funneling millions of dollars of policyholders and taxpayers funds into the “front groups” to protect their ever-increasing profits. It is no-secret, the industry collects 15% on top of costs for group healthcare insurance plans and 20% on top of individual healthcare insurance plan costs as legislated through the ACA. This comes on top of an ever increasing healthcare cost from hospitals, pharma, and doctors regardless of whether there is an increased benefit from the procedure, supply, pharmaceutical, etc.

To add to this is the cost of submitting bills to different healthcare insurance companies each of which has different processes requiring additional manpower at hospitals, etc. Differences in billing practices require additional functional capability which translates into more people. Today’s clerical costs are approximately 15-20% of healthcare costs which does not exist in Single Payer .

A Public Option would minimize the differences in coverage and would include one payer of costs to servicers similar to what Medicare does. The local state Healthcare Futures organizations are attempting to block the passage of a Public Option.

Connecticut

As a result of the potential lower costs in a Public Option, the legislation in Connecticut is facing opposition from healthcare insurance companies. The legislation has the backing of State Comptroller Kevin Lembo and several Democratic legislators. Governor Ned Lamont (D) has remained silent on the bill to date.

The CEOs of five insurers doing business in the state are trying to move the Governor into their camp which include two companies based there. Both Cigna and Aetna, sent the Governor a letter this month implying they would move jobs out of the state if the public option bill became law.

Two years ago when lawmakers were bringing a similar bill to the governor’s desk, State Comptroller Kevin Lembo claimed Cigna CEO David Cordani threatened to leave Connecticut if a public option was established. the threat was made even though Cigna does not sell coverage on the state’s exchange and has few large group customers. Cigna acknowledged it lobbied against the bill but denied making a threat.

In response to the letter to the Connecticut Governor by the five insurers, Comptroller Lembo issued a statement noting that insurers posted record profits during the pandemic and asked;

“When will enough be enough (profits)? Or are legislators going to serve their constituents or allow five corporations determine what becomes law in our state?”

Colorado

The Colorado legislation gives private insurers 2 years to start the process of reducing healthcare and healthcare insurance costs. The public option would only go into effect if Insurance companies could not achieve the benchmarks set by the bill.

In both Connecticut and Colorado are offshoots of the Partnership for America’s Health Care Future (PAHCF). Residents of both states are hearing from these affiliate Health Care Futures. The Colorado’s Health Care Future is using the same messaging as Connecticut even though the legislation in that state is substantially different from the Connecticut bill.

One of the Healthcare Furure’s claims in Colorado is the public option would lead to less profitability of rural hospitals in the state causing them to close. Healthcare Futures fails to mention one of it funders (HCA Healthcare) reporting Colorado hospital’s profit margin being more than 40%.

Reality

Why ACOs?: We have only talked about the cost involved in having several hundred healthcare insurer analysts processing the bills from the thousands of ACO/hospital billing processors necessary to process the billing for each insurance company. The costs of utilizing commercial insurance has been estimated to be between 15 and 20% of the cost of healthcare in the US.

In single payer as advocated by Bernie Sanders (when there are no ACOs, etc.) Pramila Jayapal, and Kip Sullivan; there is one payer, budgets are set for hospitals by HHS not the ACO, fee schedules are established for doctors, and price ceilings are established for prescription drugs. The issue of ACOs is unmentioned by this article’s author. Congress included in the ACA (aka Obamacare) a section (Section 3022) requiring CMS to establish an ACO program within the traditional FFS Medicare program.

It is not clear why Congress chose to use ACOs. Congress was warned in 2008 by the Congressional Budget Office, ACOs would not save money for Medicare. The simplest way to describe ACOs is to say they are similar to HMOs. Like HMOs, they are corporations owning or contracting with chains of hospitals and clinics. ACOs also have the equivalent of enrollees or patients.

ACOs:

- attempt to keep their “enrollees” from seeking care outside their networks;

- bear insurance risk (that is, they are paid on a per-enrollee basis and in exchange are obligated to provide medically necessary services to their enrollees); and

- because they are risk-bearing organizations, they generate overhead costs similar to those created by traditional insurance companies.

Because ACOs resemble insurance companies, nearly half of them already have contracts with insurance companies to help them carry out insurance-related tasks. The largest insurance companies – Aetna, Humana, and United Healthcare, for example – are already deeply embedded in the ACO industry.

The only significant differences between ACOs and HMOs are:

- ACO “enrollees” are assigned to ACOs (usually without their knowledge) whereas HMO enrollees choose to enroll, and

- HMOs bear all insurance risk while ACOs split the risk of loss or savings with another insurer (in Medicare’s case, risk is shared with the Medicare program).

Both of these differences are being eroded. Many ACOs are saying they should be allowed to enroll people so they can restrict enrollee use of out-of-ACO providers, and some influential ACO proponents are proposing ACOs be paid premiums so they can absorb total losses and keep total profits.

An important similarity between ACOs and HMOs: ACOs have failed to cut Medicare’s costs, just as the CBO predicted.

–

Healthcare Insurance: The author discusses healthcare insurance issues. Today, for-profit insurers are bigger, richer, and more powerful. Recent mergers and acquisitions have enlarged these companies to the point of CVS Health being #5 on the Fortune 500 list of American companies and UnitedHealth Group is #7.

Their growth has been at the taxpayers’ expense. Seventy-two percent of United Healthcare’s revenues in the U.S. during the first quarter of 2021 came from government business through Medicare Advantage, Medicare Supplement plans, and the state Medicaid programs they manage. For several quarters during the pandemic, those programs have been the biggest source of enrollment growth.

Medicare Advantage has become a cash cow for big insurers. MA insurers are known to conduct business right at or to the line of what is considered ethical and legal and often crossing it to maximize profits. A recent analysis by HHS found CMS was overcharged by Humana ~ $200 million in just a single year (2015).

Health insurers treating millions of seniors have overcharged Medicare by nearly $30 billion over the past three years alone (2016 – 2918). Federal officials say they are moving ahead with long-delayed plans to recoup at least part of the money.

Officials have known that some Medicare Advantage plans overbill the government by exaggerating how sick their patients are or by charging Medicare for treating serious medical conditions they cannot prove their patients have.

Medicare Advantage Insurers spend huge amounts lobbying Congress to keep the federal spigot flowing. They have ramped up Washington lobbying budgets this year in an effort to protect their profits and to secure funds to cover laid-off workers’ COBRA premiums. The companies Insurers also lobby to keep a public option at bay.

America’s Health Insurance Plans spent more money lobbying Congress during the first 3 months of this year. An ~ $3.9 million was spent this last quarter which was more than any prior quarter. A big player in Medicare Advantage and Medicaid, Centene increased its first quarter lobbying spend by 80%.

The big insurers are bigger and more profitable today having figured out how to game the system to their advantage in Washington and state capitals. They are prepared to spend whatever it takes to maintain the advantage. With certainty, it can be said they are protecting against the Public Option which can provide healthcare insurance at a lesser cost. Maintaining the status quo and the emphasis on profits versus care suits them.

–

Competition: Passing the ACA, the Risk Corridor and the Herfindahl – Hirschman Index

Early on when the ACA was coming to pass, Dems needed every Senator they could muster to pass a resolution before they could pass the ACA using Reconciliation. The one hold out was the Senator from Aetna, Joe Lieberman.

“if the bill remains what it is now, I will not be able to support a cloture motion before final passage.” In other words, Lieberman will support a filibuster.”

Joe’s strength was in not voting with the the Democrats for Cloture which required 60 votes unless the Public Option was eliminated from the ACA. Once Cloture was passed, the ACA required 51 votes as the risk of a filibuster was prevented. Without the Senator from Aetna, the ACA would have never passed and the Public Option was blocked.

Another reason insurance companies are in command is the elimination of the Risk Corridor Program with the insertion of Section 227 by House Representatives Upton and Jackson into the Cromnibus Bill – 2014

The impact of Section 227 was; Co-ops going bankrupt, insurance companies withdrawing from the exchanges leaving some areas with one healthcare provider, constituents losing insurance as policies were canceled, and premiums increasing. Co-ops were competition to insurance companies and less costly.

The intent of the ACA Risk Corridor program was to cover losses resulting from acquiring too many risky people during any one year up to a three year adjustment period. At the end of the 3 year period, healthcare insurance companies and Co-ops were expected to have balanced losses with profits.

The ACA Risk Corridor Program was similar to the Republican Part D Risk Corridor Program which is a continuous year after year program. They got theirs and defeated the Democrats version of it for the ACA.

The Herfindahl-Hirschman Index measure of market concentration and is used to determine market competitiveness. Results of using the HHI as a measure of competition showed that market concentration increased amongst hospitals, specialty physicians, and primary care physicians over the last decade.

One study found that 90 percent of U.S. metropolitan areas were highly concentrated for hospitals; 39 percent for primary care physicians; and 65 percent for specialty physicians. Another study, which looked at the average concentration across all provider types, found that 90 percent of metropolitan areas met or exceeded the 2,500 HHI threshold for a highly concentrated market.

There is more to this to make a separate post on it as it worsens . . .

Conclusion

The author of the articles points a condemning finger at the Healthcare Insurance industry which does deserve a portion of the blame for high and rising healthcare costs. However, healthcare insurance is also a reflection of what it has to cover and provide for in reimbursement of healthcare costs.

There are any number of written articles calling out the increased costs of hospitals, healthcare supplies, pharmaceuticals, procedures, and surgeries which give credence to the rising costs of healthcare. Much of healthcare insurance costs are involved in the clerical function of healthcare processing billings which involves numerous people.

This is not new information and it leaves me wondering why just insurance was talked about in his article. Oh and healthcare insurance would not be the only opposed to a Public Option.