There are issues with Medicare which are easily fixed. Maggie Mahar was writing on healthcare at Angry Bear. I did the editing. I picked up on the issues with her on healthcare and have portrayed writers such as Merrill, Kip Sullivan, Charles Gaba, Steve Early, Susan Gordon, Andrew Sprung, etc. There are issues with healthcare such as cost. Then there are make believe issues such as Medicare being in trouble. The same is true of Social Security. A few tweaks here and there and the problems go away for 75 years. Read on with Merrill Gooz. ~~~~~~~~ Calls for radical transformation of the program ignore the trust fund’s history, and how much it rapidly responds to policy and the economic changes. Fellow healthcare writer Merrill Goozner

Topics:

Bill Haskell considers the following as important: Medicare, Merrill Gooz, social security

This could be interesting, too:

Joel Eissenberg writes Elon didn’t get the memo

Angry Bear writes Social Security, a “pretty good program and we can afford it”

Angry Bear writes Social Security and Its Administration in 2025

Bill Haskell writes “Less than 1 percent of Social Security payments are improper”

There are issues with Medicare which are easily fixed.

Maggie Mahar was writing on healthcare at Angry Bear. I did the editing. I picked up on the issues with her on healthcare and have portrayed writers such as Merrill, Kip Sullivan, Charles Gaba, Steve Early, Susan Gordon, Andrew Sprung, etc.

There are issues with healthcare such as cost. Then there are make believe issues such as Medicare being in trouble. The same is true of Social Security. A few tweaks here and there and the problems go away for 75 years.

Read on with Merrill Gooz.

~~~~~~~~

Calls for radical transformation of the program ignore the trust fund’s history, and how much it rapidly responds to policy and the economic changes.

Fellow healthcare writer Merrill Goozner at Gooznews . . .

The House Republican Study Committee last week unveiled its latest plan to cut Social Security and Medicare. Even some rightwing conservatives are tearing their hair out.

“What a terrible idea,” Sen. Josh Hawley (R-MO) told reporters on Capitol Hill. “If Republicans want to be in the minority party forever, then go ahead and endorse that.”

He was only referring to the plan’s call to postpone the retirement age to 67, which would force working class people to work more years at more physically taxing jobs before receiving benefits from a program they paid into for their entire working lives. People in the bottom half of the income distribution are much more dependent on Social Security for their retirement income than wealthier people.

Democrats, including President Biden, immediately pounced on the idea of cutting retirement programs, which was endorsed by at least 160 House Republicans. Biden . . .

“Not on my watch.”

One way to describe the soon-to-be-coronated Republican standard bearer’s position on the issue is that he consistently supports both sides. Here’s how Perplexity.ai described his position (I prefer it to ChatGPT as an artificial intelligence search engine because it gives sources for its responses, which allows the user to doublecheck and evaluate their quality ):

“Trump’s stance on this issue has been inconsistent, with his administration proposing budget cuts to Social Security and Medicare programs but also emphasizing protection for these programs during his campaign rallies.”

Its cited sources were CNN, NBC and The Hill, an inside-the-Beltway publication.

Blame the trust fund

Since I focus mostly on health care, let’s start with the Republican Party’s rationale for cutting Medicare.

The plan’s lead-in to its first paragraph on the issue said it all: “Looming insolvency” (bold face in the original). “The Republican Study Committee Budget would help save this critical program and protect seniors from the devastating 11 percent across-the-board cuts resulting from the Hospital Trust Funds insolvency in 2031.”

I first heard reference to the looming insolvency of the Medicare trust fund in the early 1980s. During the steep recession of the early Reagan years, the accumulated surpluses in the trust fund actually did face exhaustion. Increases in the payroll tax in 1983 and 1986 (signed into law by president Reagan) eliminated the threat.

This threat has been resuscitated nearly every election year since, thanks in part to the constant harping by the deficit hawks at the Committee for a Responsible Federal Budget, whose board includes a long list of retired conservative politicians and government officials (mostly Republican but a few Democrats).

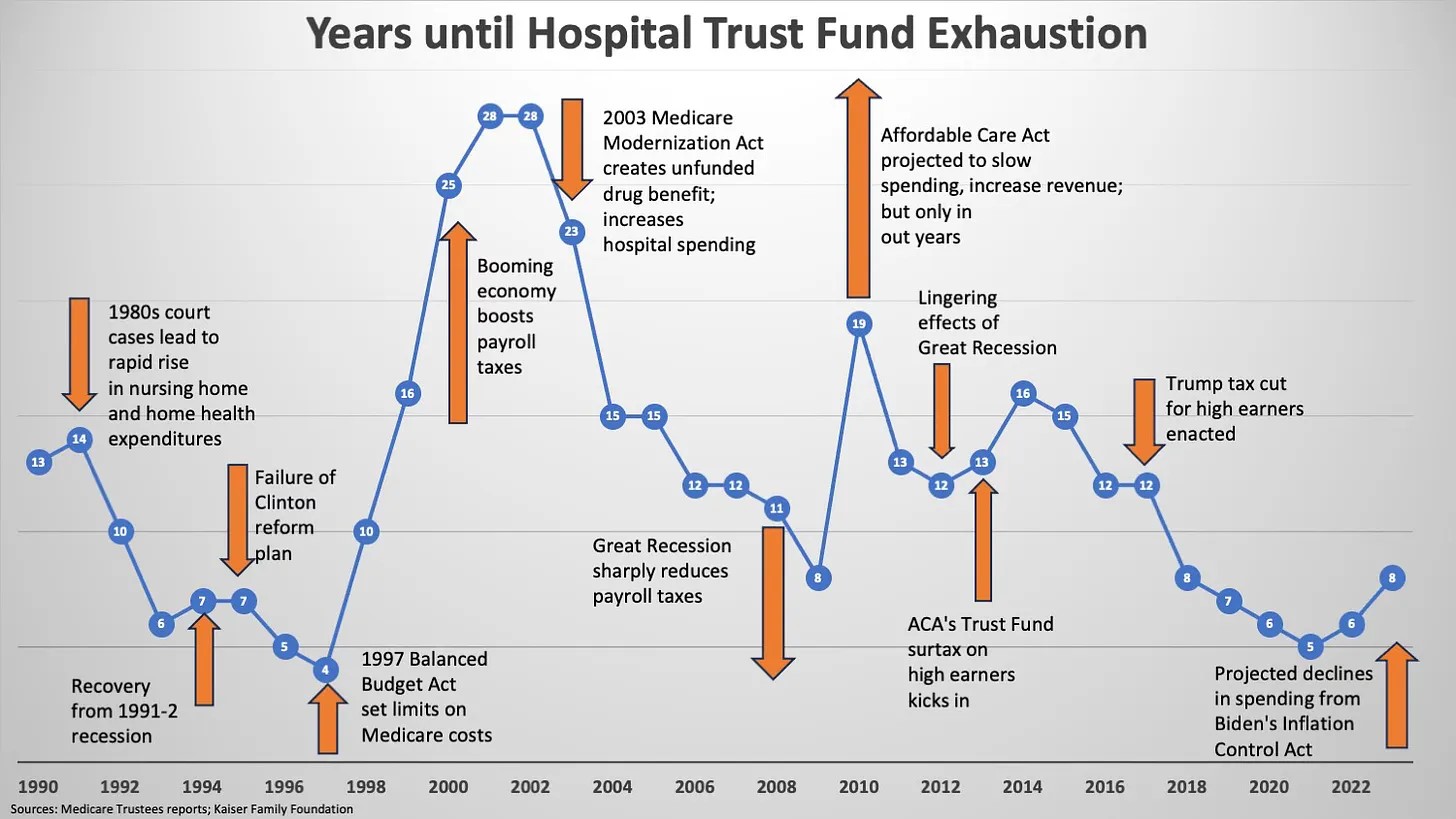

But is the threat real? Le’s review the history of the Medicare trust’s fund “exhaustion date” — now projected for 2031 in the most recent Trustees report. A new report is due by the close of business on March 31 — less than a week away.

What we see from the below chart is that the trust fund’s exhaustion date has swung wildly over the past 30-plus years, ranging from a high of 28 years in the future to as low as four years in the future. When one delves into the reasons offered each year by the trustees, one finds that that hospital trust fund solvency in highly responsive to changes in policy and changes in the economy.

A constantly moving goal post

{kind=link}

It’s easy to understand how changes in the economy effect trust fund solvency. When the economy is growing and unemployment is low, tax collections — the Medicare hospital trust fund relies on the 2.9 percent payroll tax, half paid by workers and half paid by their employers — are high. The trust fund’s exhaustion date gets pushed farther into the future. During recessions, the opposite occurs.

But the trust fund’s solvency and projected exhaustion dates are also responsive to policy changes that affect how government dollars for health care are spent. The 1997 Balanced Budget Act signed by President Clinton slapped limits on hospital and physician reimbursement rates, which set the stage for a major extension of program solvency. The unfunded Medicare Modernization Act of 2003 that established the drug benefit, enacted under President George W. Bush to ensure his reelection, reversed that momentum.

Similarly, the Trump administration’s tax cuts for corporations and wealthy individuals in 2017 reversed the effects of the higher payroll tax collections that had been included in President Obama’s 2010 Affordable Care Act. The Biden administration’s Inflation Control Act, which included for the first time limits on some drug prices including some used in hospitals, pushed the exhaustion date farther into the future.

Indeed, if one wants to draw a general rule from the above chart, the solvency of the Medicare trust fund improves under Democrats and worsens under Republicans. The exception in recent decades was the first term of the Clinton administration, when his health care reform plan failed and Republicans led by Newt Gingrich won control of both houses of Congress.

What’s the plan?

The latest not-so-new plan from the House Republicans would turn Medicare into a voucher program, which they refer to as premium support. They plan to combine program’s hospital, physician and drug benefits (Parts A, B, and D, respectively) into a single plan, which would be offered by private insurance companies. Seniors would receive a legislatively determined level of support to purchase plans. The rest would have to come out of pocket.

The level of support could be set either as a dollar amount or as a percentage of the traditional Medicare plan, which would still be available to seniors. One way to describe it is “Medicare Advantage for All.”

That could turn out to be a disaster for the millions of seniors, a majority of whom are anxious to save money through reducing their upfront out-of-pocket health care costs. Wealthier seniors who remain in traditional Medicare would be able to buy supplemental plans as many do now. The less wealthy will continue to flock to MA plans for their lower up-front premiums.

But they could wind up being hit with huge out-of-pocket expenses when they become seriously ill. The size of those payments would depend on the level of premium support offered by the Republican Congress that enacted the plan. The lower the level of support, the higher the out-of-pocket expenses.

Do you trust the Republicans to set a generous level of support? If so, someone who owns Truth Social has some stock he’d like to sell you.

What about Social Security?

Last year, the trustees of the Social Security trust fund projected it will run out of money in 2034. That date has bounced around, but has been set somewhere between 2030 and 2040 for most of the past four decades. That’s because the demographics of the country — how many old people will be collecting benefits in future years — are easily calculated. The precise date is largely dependent on the state of the economy — how many people are working and paying the flat payroll tax.

And that’s why there’s an easy fix for the projected shortfall (which, if unaddressed, could reduce benefits by about 23% in 2034). All you have to do is apply the payroll tax, which is currently capped for people earning over $168,600 a year, to all income.

The growth in income inequality has made Social Security’s finances more precarious. As people in the highest income brackets took home a larger slice of the total income pie, less of the nation’s total income was taxed to provide retirement benefits for the elderly.

In 1977, Congress set the share of national income that should come under the Social Security payroll tax at 90 percent. Today, only 83 percent of national income is taxed, a reflection of a greater share of national income going to those in the highest brackets.

Eliminating the cap would end the trust fund’s gap for the foreseeable future. Even if we apply the tax only to those earning over $400,000 a year would stabilize long-term financing for the program, according to legislation introduced by Sen. Sheldon Whitehouse (D-Rhode Island).