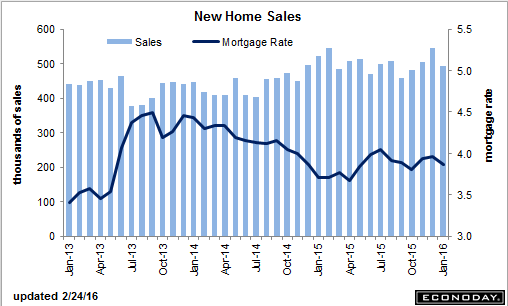

Challenging to put a good spin on this one, but they gave it their best shot, as the wheels are coming off at every turn: New Home SalesHighlightsA downturn out West helped pull new homes sales down a steep 9.2 percent in January to a lower-than-expected annualized rate of 494,000. The level, however, is still respectable given that there is no revision to December which stands at a very solid 544,000. Sales in the West, which is a key region for the new home market, fell 32 percent in the month which pulls down the region’s year-on-year rate to minus 24 percent. The South and Midwest show only marginal year-on-year contraction with the Northeast, the smallest new home region however, up sharply.Price discounting seems to be at play as it was in yesterday’s existing home sales report. The median price fell 5.7 percent in the month to 8,000 for a year-on-year decline of 4.5 percent. Sales had been ahead of prices before this report but not anymore, with a nearly double-digit year-on-year pace now falling into contraction at minus 5.2 percent.Supply has been very slow to enter the market, the result largely of constraints in the construction sector. But more new homes did enter the market in the month, up 2.1 percent to 238,000 and supply relative to sales, given the slowdown in sales, is up sharply, to 5.8 months vs 5.1 months.

Topics:

WARREN MOSLER considers the following as important: housing, Treasury

This could be interesting, too:

Nick Falvo writes Subsidized housing for francophone seniors in minority situations

NewDealdemocrat writes Declining Housing Construction

Nick Falvo writes Homelessness among older persons

Bill Haskell writes Q3 Update: Housing Delinquencies, Foreclosures and REO

Challenging to put a good spin on this one, but they gave it their best shot, as the wheels are coming off at every turn:

New Home Sales

Highlights

A downturn out West helped pull new homes sales down a steep 9.2 percent in January to a lower-than-expected annualized rate of 494,000. The level, however, is still respectable given that there is no revision to December which stands at a very solid 544,000. Sales in the West, which is a key region for the new home market, fell 32 percent in the month which pulls down the region’s year-on-year rate to minus 24 percent. The South and Midwest show only marginal year-on-year contraction with the Northeast, the smallest new home region however, up sharply.Price discounting seems to be at play as it was in yesterday’s existing home sales report. The median price fell 5.7 percent in the month to $278,000 for a year-on-year decline of 4.5 percent. Sales had been ahead of prices before this report but not anymore, with a nearly double-digit year-on-year pace now falling into contraction at minus 5.2 percent.

Supply has been very slow to enter the market, the result largely of constraints in the construction sector. But more new homes did enter the market in the month, up 2.1 percent to 238,000 and supply relative to sales, given the slowdown in sales, is up sharply, to 5.8 months vs 5.1 months.

The slope for the housing sector has been volatile but is trending upward. Price discounts will help boost sales but will also pull down home-price appreciation which has been a central area of strength for household wealth.

This is from the not so reliable survey organization that tends to overstate things. And it now has the service sector in contraction and the spin is bad as well:

PMI Services Flash

Highlights

In what could be a chilling indication of trouble ahead, the February flash for the service PMI slipped below breakeven 50 to 49.8 for the weakest reading since the government shutdown of October 2013.New orders are still growing but at the slowest pace in nearly six years with contraction in backlog orders the most severe since early 2014. The 12-month outlook, though still positive, is the least positive in 5-1/2 years. Employment in the sample is still growing but for how long is a question. Price data are not favorable, with inputs down and growth in selling prices at a 5-month low.

The breakdown in the service sector, a breakdown however still isolated to this report, would leave the economy without a central point of strength. The declines here do suggest that domestic demand could be on the downswing and falling in line with sinking demand overseas.

These are up a bit this week but still depressed historically and the comps vs a year ago will soon get a lot tougher:

From the way the yield has been falling on the 10 year tsy seems market participants don’t see the same economic strength the Fed sees: