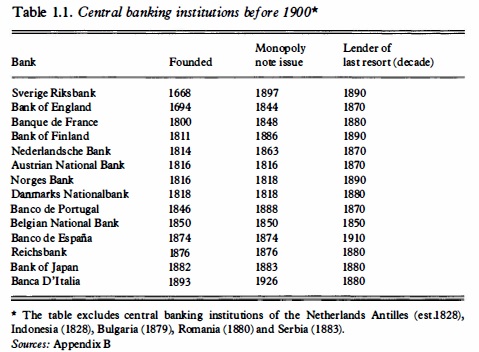

Next semester I'll be teaching a senior seminar on the history of central banks. The idea is to blend economic history, history of economics ideas and monetary theory in equal parts. And I decided to post on some of the topics I'll discuss in the class, very much like Robert Paul Wolff's tutorials in his blog The Philosopher's Stone, but probably in a less instructive and interesting way than the ones he posts (see this multi-part tutorial on Marx that starts here, and continues here and here and so on; last of nineteen parts here). In the same spirit, I'll suggest some readings for those interested in the topic. An obvious place to start is with the paper "The changing role of central banks" by Charles Goodhart, or for an alternative interpretation by yours truly go here. Central banks are among the oldest institutions employed for macroeconomic policy management around the world. The oldest central banks are old indeed (as can be seen in the table below, from Capie, Fischer, Goodhart and Schnadt's book The Future of Central Banking*). They precede monetary theory and macroeconomics as fields of study. More surprisingly, central banks even came before the development a more coherent set of general economic principles, developed by classical political economy authors.

Topics:

Matias Vernengo considers the following as important: History of central banks

This could be interesting, too:

Matias Vernengo writes Handbook of the History of Money and Currency

Matias Vernengo writes Classical Political Economy and the Evolution of Central Banks

Matias Vernengo writes Classical Political Economics and the History of Central Banks

Matias Vernengo writes Adam Smith on the origins of first generation public banks

None other than Adam Smith, an ardent critic of monopolies in general, was very keen about the Bank of England, a quasi-monopoly after all, arguing that it was “the greatest bank of circulation in Europe” and that it acted “not only as an ordinary bank, but as a great engine of the state.” In this view, at least, Smith was in accordance with several mercantilist authors, which, otherwise, he criticized harshly. Smith was apparently concerned that competition, meaning free entry, in the banking sector would lead to a multitude of undercapitalized “beggarly bankers” that would, in turn, lead to a heightened risk of “frequent bankruptcies.” However, Smith’s views are less contradictory than one might think, since the modern ideas of market efficiency have less to do with the theories developed in the late 18th century and early part of the following by classical political economy authors, than with the marginalist ideas developed in the last quarter of the 19th century. In particular, for Smith efficiency or the division of labor is connected to the broader question of capital accumulation and the wealth of nations, rather than the narrow question of allocative efficiency, and the notion that resources are fully utilized.

Further, Smith suggests that efficiency is ultimately dependent on the expansion of demand, or in his words that “the division of labor is limited by the size of the markets.” In that sense, not only did Smith emphasize the forces of demand, rather than supply in the process of long run growth, but also he was aware of the existence of processes of cumulative causation. His famous vent for surplus is the typical example of a cumulative process. Larger markets for British goods would lead to the necessity to provide for increasing demand and lead to an improvement of the conditions of production, an expansion of the division of labor, which would lead to cheaper and higher quality products, which, in turn, would lead to higher demand.

The demand-led process of accumulation suggests that Smith was well aware that institutions that favored and facilitated the access to markets and allowed for the expansion of demand were an important element in the development of market economies. Further, the idea of cumulative causation suggests that size and scale matter, and that increasing returns are a pervasive feature of market economies. Hence, the Bank of England, which was at the center of financial development, which allowed the expansion of international trade ventures, and more directly through its role in financing the state and the naval expansion of England, opening markets for British products, was an essential element for capital accumulation. Smith was, as much as the mercantilist authors that he criticized, very much in favor of the expansion of markets, which accounts for his favorable views about the Bank.

Nevertheless, it would be the role of the BoE during the inconvertibility period (1797-1821), associated with the Napoleonic Wars, that would indelibly mark the views about the Bank, and hence much of what economists think about central banks, in the minds of latter generations. The inconvertibility period led to the famous Bullionist Controversy, central for the development of monetary theory. The acceleration of inflation marked this period, and several authors known as Bullionists, most prominently David Ricardo, would be critical of the Bank’s policies. Bullionists, a name derived from their call to a return to the Gold Standard (i.e. bullion), argued that inflation was caused by the overissuing of paper money by the Bank.

Bullionists saw the return to the Gold Standard as a necessary step to maintain price stability. Central banks should not control money supply, and the solution demanded a strict impersonal rule to provide price stability. The idea that the Bank of England had to be the guardian of the value of the pound, and that price stability was paramount was enshrined in this particular period. Interestingly enough, the Bank of England still did not have during the Bullionist Controversy the monopoly of the issuing of bank notes, which would only be obtained after Sir Robert Peel’s Bank Act of 1844.

Bullionists saw the return to the Gold Standard as a necessary step to maintain price stability. Central banks should not control money supply, and the solution demanded a strict impersonal rule to provide price stability. The idea that the Bank of England had to be the guardian of the value of the pound, and that price stability was paramount was enshrined in this particular period. Interestingly enough, the Bank of England still did not have during the Bullionist Controversy the monopoly of the issuing of bank notes, which would only be obtained after Sir Robert Peel’s Bank Act of 1844.

The Bank Act, which separated the banking and issuing departments of the Bank to guarantee that overissue would not take place, consolidated the modern concept of central banks and established that price stability would be the only policy concern. The additional feature of the Victorian central bank was the increasing preoccupation with financial stability, which resulted from the frequent crises, and which led to the development of the role of the lender of last resort (LOLR), advanced by Henry Thornton and later by Walter Bagehot.

The Victorian view of central banks was only challenged in the 1930s, in the aftermath of the Great Depression and as a result of the Keynesian Revolution (something discussed in this paper). But in the last thirty years or so the Victorian view of central banks, concerned only with inflation, has been reestablished, even if the theoretical justification is slightly different. The last global crisis has undermined the theoretical basis for the Independent Central Bank (ICB) and Inflation Targeting (IT), and the widespread use of unconventional policies (like Quantitative Easing, QE) indicated a certain degree of flexibility in the face of the crisis, but there has been little institutional change. In the next post (in the tutorial) I will deal with the era before central banks, and the reasons for their emergence.

* The First and Second Banks of the United States are not included in the table, but could certainly be considered as part of the club of early central banks.