From David Ruccio The same day I wrote that capitalism was coming apart at the seams, indicated by the shocking disparity between the compensation of corporate CEOs and workers, the Business Roundtable published its new statement of purpose of a corporation.* The 180 or so corporate executives who signed the statement declared that all their stakeholders, not just owners of equity shares, were important to their mission. Many business pundits, such as Andrew Ross Sorkin, greeted the new statement as a sign that the era of shareholder democracy (what he refers to as “shareholder primacy”) had finally come to an end and that a “significant shift” in corporate responsibility to society would be ushered in. Readers, however, had their doubts, most of them echoing JDK’s response to Sorkin’s

Topics:

David F. Ruccio considers the following as important: Uncategorized

This could be interesting, too:

tom writes The Ukraine war and Europe’s deepening march of folly

Stavros Mavroudeas writes CfP of Marxist Macroeconomic Modelling workgroup – 18th WAPE Forum, Istanbul August 6-8, 2025

Lars Pålsson Syll writes The pretence-of-knowledge syndrome

Dean Baker writes Crypto and Donald Trump’s strategic baseball card reserve

from David Ruccio

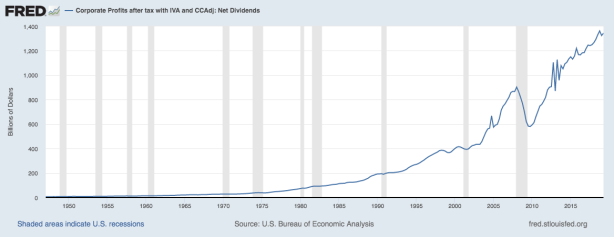

The same day I wrote that capitalism was coming apart at the seams, indicated by the shocking disparity between the compensation of corporate CEOs and workers, the Business Roundtable published its new statement of purpose of a corporation.* The 180 or so corporate executives who signed the statement declared that all their stakeholders, not just owners of equity shares, were important to their mission.

Many business pundits, such as Andrew Ross Sorkin, greeted the new statement as a sign that the era of shareholder democracy (what he refers to as “shareholder primacy”) had finally come to an end and that a “significant shift” in corporate responsibility to society would be ushered in. Readers, however, had their doubts, most of them echoing JDK’s response to Sorkin’s piece: “Talk is cheap.”

The fact is, over the past three decades, net dividend payments to shareholders have soared—from $178 billion in 1989 to $1.3 trillion in 2019 (that’s an increase of 630 percent, for those keeping track).** And much of the responsibility is laid at the feet of mainstream economists like Milton Friedman (pdf), who famously declared that “there is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits” and the only responsibility of corporate executives is to their employers, the shareholders—and corporate raiders such as Carl Icahn.

As I see it, the idea of shareholder democracy has merely served as a cover for any and all corporate decisions and strategies. When pushed to take on other responsibilities, or to make other decisions, the corporate defense has long been that it ran counter to the mission of maximizing profits or shareholder value.

In reality, corporations have never attempted to achieve just one objective or to maximize one value. One issue is that the usual objectives or values ascribed to corporate managers are ill-defined. There is neither singular meaning of profits (since, as they’re reported, they’re largely the result of a particular set of accounting conventions, defined over the fuzzy boundaries of the inside and outside of a corporate entity) nor a unique time frame (over what period are profits or dividends maximized—a week, quarter, year?).*** But the defense of such a corporate mission has served as a convenient excuse to resist pressures to make different decisions or adopt alternative strategies—such as increasing worker pay, improving working conditions, implementing environmentally sustainable practices, and so on.

My view, as I argued back in 2013, is that corporations have never done just one thing or followed a single rule. They do make profits (at least sometimes, depending on the definition and timeframe). But they also seek to grow their enterprises and destroy the competition and maintain good public relations and buy government officials and reward their CEOs and squeeze workers and lower costs and reward shareholders and implement new forms of automation and build factories that collapse and. . .well, you get the idea. In other words, they appropriate and distribute surplus-value in all kinds of ways depending on the particular conditions and struggles that take place over the shape and direction of their enterprises.

The problem inherent both in the new Business Roundtable statement of purpose and in the attempts by corporate critics to argue that corporations should take on additional social responsibilities is that corporations are already too central to the U.S. economy and society. They’re the main institution where the surplus is appropriated and then distributed—with all the consequent effects on the wider society. The private decisions of corporate entities, as decided by the boards of directors and implemented by the chief executives, are responsible for the Second Great Depression, the grotesque levels of economic inequality that have been growing for decades now, the global-warming crisis, and so much more. Why would anyone want to give corporations even more power or scope to decide how to solve those problems when they’re the root of the problem in the first place?

No, the only viable strategy is make corporations less important, to decenter the American economy and society from the decisions made by corporate directors and executives. That begins with fostering the growth of other types of firms (such as worker-owned cooperatives) and making sure that the workers employed by corporations play a significant role in corporations (including how much surplus there will be and how it will be utilized). That’s the best way of moving beyond the era of shareholder democracy to a real economic democracy.

Anything else is just cheap talk.

*I certainly don’t want to imply that the Business Roundtable was responding to my blog post. No, the fact that they felt it necessary to issue such a new statement of purpose is an indication that American corporations—and, with them, U.S. capitalism—have lost a great deal of legitimacy in recent years. As Farhad Manjoo [ht: ja] recently wrote,

A recession looms, and the nation’s C.E.O.s are growing fearful.

It isn’t the potential of downturn itself that has them alarmed — downturns come and downturns go, but whatever happens, chief executives, like cats, tend to land on their comfortably padded feet.

Instead, the cause of their fear appears to be something more fundamental. . .They’re worried that when the next recession breaks, revolution might, too. This could be the hour that the ship comes in: The coming recession might finally prompt the masses to sharpen their pitchforks and demand a reckoning.

**During that same period, average hourly earnings (for production and nonsupervisory workers) increased by only 140 percent—but corporate profits (after tax) rose by 570 percent.

***As I have long explained to students, that’s the myth that serves as the foundation of the neoclassical theory of the profit-maximizing firm: what exactly are corporate profits and over what time frame are they supposed to be maximized? The assumption of a profit-maximizing firm is equivalent to what one hears from many so-called radical economists, that “capitalists accumulate capital.” Again, no. Accumulating capital (that is, purchasing new elements of constant and variable capital) is only one of the many possible forms in which capitalists distribute the surplus-value they appropriate from their workers. Sometimes they accumulate capital, and other times they don’t. The presumption that they always seek to accumulate capital is the heroic story proffered by classical economists (so that, in their view, capitalist growth would take place), much as neoclassical economists today presume that capitalists maximize profits (so that, in their view, an efficient allocation of resources will result). Marxists presume neither that capitalists maximize profits nor that they always and everywhere accumulate capital.