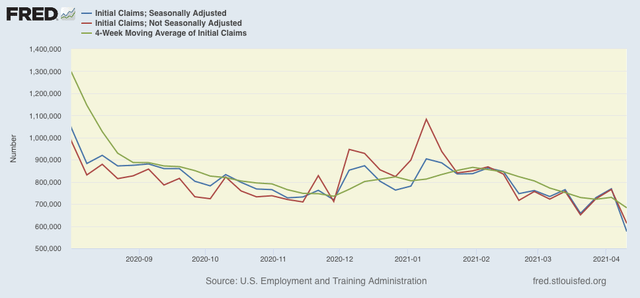

Jobless claims break on through – 1M+ jobs report for April looks likely As I have said for the past few weeks, new jobless claims are likely to the most important weekly economic data for the next 3 to 6 months. With the number of those vaccinated continuing to increase, I have been expecting a big increase in renewed consumer and social activities, with a concomitant gain in monthly employment gains – as we saw in the March jobs report.Four weeks ago I set a few objective targets: new claims to be under 500,000 by Memorial Day, and below 400,000 by Labor Day. This week was a major advance towards those targets. On a unadjusted basis, new jobless claims declined by 152,833 to 612,919. Seasonally adjusted claims declined by 193,000 to

Topics:

NewDealdemocrat considers the following as important: jobless claims, US EConomics, US/Global Economics

This could be interesting, too:

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Bill Haskell writes Families Struggle Paying for Child Care While Working

Joel Eissenberg writes Time for Senate Dems to stand up against Trump/Musk

Jobless claims break on through – 1M+ jobs report for April looks likely

As I have said for the past few weeks, new jobless claims are likely to the most important weekly economic data for the next 3 to 6 months. With the number of those vaccinated continuing to increase, I have been expecting a big increase in renewed consumer and social activities, with a concomitant gain in monthly employment gains – as we saw in the March jobs report.Four weeks ago I set a few objective targets: new claims to be under 500,000 by Memorial Day, and below 400,000 by Labor Day.

This week was a major advance towards those targets.

On a unadjusted basis, new jobless claims declined by 152,833 to 612,919. Seasonally adjusted claims declined by 193,000 to 576,000 (with last week’s number being adjusted upward by 25,000). The 4 week average of claims also declined by 42,250 to 683,000.

Here is the close up since last August (recall that these numbers were in the range of 5 to 7 million at their worst in April of last year):

Note that I have discontinued the YoY comparisons since we would be comparing against the very worst weeks of the initial lockdowns last year.

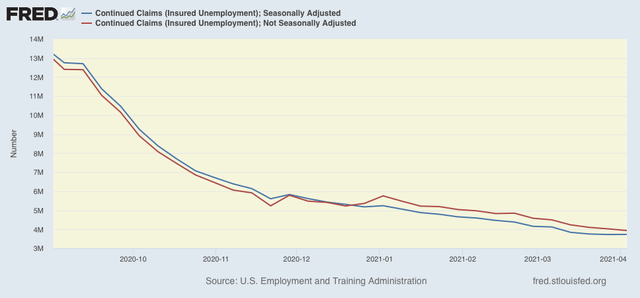

Continuing claims, which historically lag initial claims by a few weeks to several months, and which are reported with a one week lag, in something of an unusual occurrence, failed to make another new pandemic low this week. While the unadjusted number did decline 87,991 to 3,936,696, which was a new low, the seasonally adjusted number of continuing claims rose by 4,000 to 3,731,000:

Seasonally adjusted continued claims are at levels last seen in the summer of 2011, when weekly jobless claims were just over 400,000 and the unemployment rate was 8.2%.

In the last 4 weeks, since the March reference week for the jobs report, initial claims have declined on average by 68,750 m/m. This kind of decline has happened less than a dozen times since data started to be collected almost 60 years ago, and even in normal times has typically been associated with strong monthly employment gains on the order of +350,000. When we had a similar decline last August, the monthly gain in jobs was about 1,600,000.

In other words, barring big revisions or a reversal next week, April’s jobs report could easily show well over 1,000,000 new jobs added.

Let me close, however, with the caveat I added last week: I am growing more concerned at the big spike in new coronavirus cases from the now-dominant UK variant in Michigan and the Northeast. the recent decline in deaths has plateaued and may have begun to increase slightly. It is at least reasonably possible that this will counterbalance progress on the vaccine front for the next 2 to 3 months.