“Who got rich off the student debt crisis?” – Reveal (revealnews.org), James B. Steele and Lance Williams A bit of a story of how we got to this student loan debt debacle. It is long, tedious, and not exciting. And this is only part of it. In 2016, 42 million people were owing .3 trillion in student debt. It is or was a profit center for Wall Street and also the government. I suspect Wall Street still gets its cut from student loans. Their cut even though the Government makes the loans. Here is how we got into this mess. Albert Lord is a 70-year-old former accountant who became a multimillionaire executive by managing student loans. The story of how America got into the Student Loan Debt Crisis starts with him. For Albert Lord,

Topics:

run75441 considers the following as important: Education, Featured Stories, politics, student loans, US EConomics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

“Who got rich off the student debt crisis?” – Reveal (revealnews.org), James B. Steele and Lance Williams

A bit of a story of how we got to this student loan debt debacle. It is long, tedious, and not exciting. And this is only part of it.

In 2016, 42 million people were owing $1.3 trillion in student debt. It is or was a profit center for Wall Street and also the government. I suspect Wall Street still gets its cut from student loans. Their cut even though the Government makes the loans.

Here is how we got into this mess.

Albert Lord is a 70-year-old former accountant who became a multimillionaire executive by managing student loans. The story of how America got into the Student Loan Debt Crisis starts with him.

For Albert Lord, student loans became his road to riches. As the CEO of Sallie Mae he built it into a financial colossus through fees, interest, and commissions on billions of dollars of federally guaranteed student loans. Yearly he was delivering handsome profits to investors. For Lord himself, and besides pay, he was rewarded with stock eventually worth hundreds of $millions.

The source of his wealth was with the loans students needed to attend college. Today, it is not hard to find or know someone young or old burdened by these student loans. Growing along side of those thousands of students and former students burdened by student loan debt was a growing private and profitable industry thriving off of their debt. Albert Lord helped to grow it by privatizing Student Loans.

The federal government had relinquished its control of the student loan program to corporate businesses whose goals were profits over diplomas and education. Private equity companies and banks were controlling the flow of the federal loan dollars. Giving loans to students with little financial means was done on a bet they would graduate and make enough to pay the loans back. Loans they could not afford at times while the companies and banks were collecting fees and government fees to hound students in default for payment.

The privatized student loan industry has largely succeeded in preserving its status in Washington since the eighties. Congress kept passing new laws limiting the forgiveness of loans up till 2005 when it became impossible to do so. Student loans remain the only consumer debt incapable of being discharged in bankruptcy except in rare cases. It is one of the banking industry’s lobbying triumphs. Then Senator Joe Biden was spearheading many of the laws restricting bankruptcy.

Stagnating incomes for the middle-class and others has made it difficult for many to afford loans to pay increasing college costs. Reducing support for state college and universities just pushed the costs of college on to students and their parents. If state support was similar to the percentages paid in 1980, more would have gone to higher education.

Continued support to public higher education as they had in 1980 (79%), investments of $500 billion would have occurred in university systems. This is based on an analysis of data from the U.S. Bureau of Economic Analysis. State and federal budget cuts were reducing college funding serving the neediest students. If state support had even remained at 54% of the total for state universities and colleges, contributions would be more than 1980’s $500 billion to public colleges and universities. Instead, contributions dropped to 37%. A lot of ifs going on here . . .

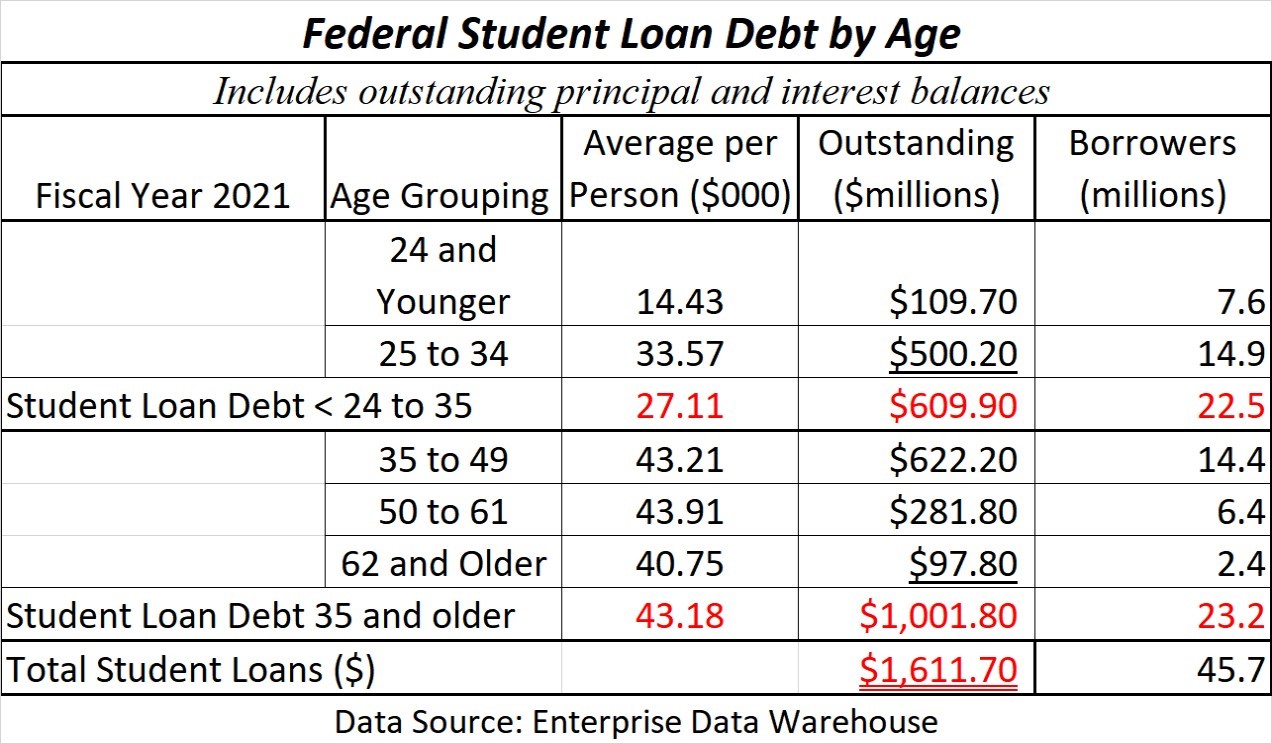

In 2014, there was less student debt per person than today and still the same impact. Forty million Americans bearing $1.3 trillion in debt. The impact of which was altering lives, relationships, and retirement. End of Year 2021, the numbers have grown to 45.7 million holding $1.62 trillion in debt. The average debt in 2014 using the numbers above was $32,500 as and grew to $35,300 in 2021.

It has been said students taking out educational loans should do so with their eyes wide open (Bill Bennet, Secretary of Education – Reagan). It is kind of hard to do so with For-Profit schools as the rules and the costs keep changing. If you are not current on payments, they would call you out of class in front of everyone. Going to For-Profit schools such as Corinthian, it was difficult to get the necessary information as an adult much less a person of 18. The latter would gain a far better understanding of what they were involved if they were joining the military. To make matters worse too few on the outside were understanding the issues of student loans. Most of all, no forgiveness for any reason.

It was bad enough in life when the agencies wanted their money. In one case in death, the agency collected on a student loan.

“Murdered, but still on the hook” – Reveal (revealnews.org)

It was not like schools were warning or educating students of the hazards of taking a student loan. In some cases, they advised students to go into forbearance after leaving college. Students in forbearane could end with increasing loans and having to pay interest before touching principal.

I am whining here a bit in driving the point home

Former head of the Department of Education Bill Bennett calls Biden’s forgiveness regressive and punishing those who were fortunate enough(?) to be able to pay back loans. In which case, letting students declare bankruptcy is regressive as it lets the borrower off the hook whether they deserve it or not. In comparison, when there are cost over runs on government projects, does the supplier pay the difference or the government?

A likelihood of the $1.6 trillion today being much of it is penalties, fees, interest accruing on the original balance. The transferring of records from private industries has been mismanaged so much it is impossible to know the original loan amounts. Does anyone believe a student would borrow $400 thousand as depicted here?

Or maybe there is a chance the 2.4 million former students 62 years of age or older can pay off the average $41,000 they each owe?

I am going to move on with this as I want to get to explaining how student loans became very profitable. Back to the sixties.

Offering up ways to gain advanced education and attacking racial injustice, Johnson’s Higher Education Act of 1965 was passed by Congress. States which were opposing such efforts were bypassed by the Federal Government (sound familar?). It was meant to ensure any student wanting to go to college would be able to through federal scholarships and loans. A noble goal . . .

Johnson stressed;

“This nation could never rest, while the door to knowledge remained closed to any American.”

Before the law, most Americans wanting to go to college had to finance it themselves. Meaning? Paying out of their own pockets, securing a scholarship, or taking out an expensive private loan(s) from commercial banks. With the passing of the Higher Education Act of 1965, students could get a less costly student bank loan. A loan with a Federal Government guarantee.

President Richard Nixon and Congress in 1972 expanded the program. The creation of a quasi-governmental agency, Student Loan Marketing Association, or Sallie Mae was taking charge administratively. Their role was to increase the amount of money available for student loans.

It is at this point, things start going in the wrong direction.

Viewed as an expansion of Johnson’s Program, Sallie Mae established a market for federally backed student loans. Banks loaned to students, and Sallie Mae bought the loans from the banks, increasing the pool of money available for loans.

The children of Johnson’s Great Society who were benefiting from student loans were now having children of their own. They were needing and the same government student loans. Its role was changing and even more so with Clinton being the catalyst for change.

With the 1992 election, Clinton initiated through Congress revisions of the student loan program making the federal government the direct lender of the loans besides the insurer. The program was eliminating the middlemen, Sallie Mae and banks, by making loans directly to students. Calling the program Direct Loans, banks were competing against a government run program not bound by the need for profits. Interest rates were lower.

Two years passed and Republicans won control in Congress.

Same old story of Republicans winning the 1994 elections and Congress moving against Direct Loans and for the privatization of Sallie Mae. Clinton gave in to the privatization of Sallie Mae to save it. Privatization had its dramatic impact. The Department of Education still oversaw student loans, but the message out of Congress couldn’t have been clearer. Bureaucrats, step aside and let the private market run the loan program efficiently.

A full array of new services were parceled out among government agencies and contractors. From making loans to collecting premiums and penalty fees. All of this consolidated under Sallie Mae’s umbrella.

A New Sheriff in the Student Loan Town

Albert Lord became CEO of Sallie Mae in 1997. Under Lord, Sallie Mae grew by leaps and bounds. Free of government control, it emerged as the dominant company in the field. The chief competition to Sallie Mae was the Education Department’s direct loan program. Since its adoption in 1993, the program was gaining popularity on college campuses. It was capturing more and more of the student loan market by the time Sallie Mae was privatized.

Sallie Mae’s marketing strategy undermined the federal program. Undermining the federal programs in unscrupulous ways. The company was paying colleges to drop out of the federal program and make Sallie Mae the campus student loan provider. It was paying college financial loan officers to serve as consultants on Sallie Mae advisory boards. It hired a New Jersey agency $15 million to steer business to Sallie Mae.

As a side note, I remember the reporting of the issues with college employees benefiting from Sallie Mae attention. Some of it being monetary and others not so direct. My children were taking out student loans.

Sallie Mae employees were manning university call centers fielding questions from students. Students thought they were getting advice from college loan officers. Sallie was sponsoring trips and cruises for financial aid officers hoping to influence them. Other student loan lenders were also engaging in similar practices. These were unethical practices I would not take advantage of as a Purchasing Manager. The Department of Education was not in the practice of budgeting entertainment for financial aid officials with free cruises on the Potomac.

The Department of Education was facing financial industry lobbying and congressional opposition. It was also struggling to maintain Clinton’s direct loan program.

In 2001, President George W. Bush took office in and cut the program further including similar actions to the VA. By 2007, Direct Loans share of the student loan market declined by more than 40 percent.

Public versus Private Loans

The majority of student loans come from the federal government. The Federal Reserve Bank of New York estimated more than 90 percent of the $1.3 trillion (2016) in outstanding student loans were government loans.

The government either directly issued these loans or backed them through a private company. The rest were private student loans by banks and companies which were not guaranteed by the government. In some years, private student loans were making up as much as 20 percent of the total debt of graduating seniors (College Access & Success in Oakland, California [an authoritative source].

Whatever the figure for private loans may be, most education experts say federal loans are preferable for students because they are less costly than private loans. Even after passing legislation denying bankruptcy, government loans were providing more consumer protections and repayment options.

During this period of time, Lord created an integrated student loan operation encompassing every phase of the burgeoning industry. Sallie Mae became a financial juggernaut. A decade after privatization, Sallie Mae’s stock price rose by 1,900 percent. Much of which, Albert Lord had in his portfolio.

From 1999 to 2004, Lord’s compensation topped $200 million. From 2010 to 2013, when students began to shoulder more and more debt, Sallie Mae’s profits were $3.5 billion. Lord retired in 2013. The following year, Sallie Mae spun off most of its student loan business into a new company, Navient. Navient is another story which Alan Collinge of Student Loan Justice Org can tell you much about it.

The rest of the story is common knowledge which I have been writing about for a decade now.

In debt and out of hope: Faces of the student loan mess – Reveal (revealnews.org)

Who got rich off the student debt crisis? – Reveal (revealnews.org)