I have added little to this commentary. Economist Dean Baker has taken a position on various aspects of the economy. A positive position which you will see many other commentaries trashing. We avoided one hell of a recession to date which would have been the equal to the 2008 collapse due to Wall Street’s addiction to gambling. You will not hear the news media promoting this. I will be posting more on this issue. Meanwhile, there exists a lot of talk about SS draining the pockets of the young. There are no subsidies to Social Security today and is it ran short of funds in 2034, here are solutions such as MMT. We could avoid issues in 2034 by small incremental increases in SS taxes for both employees and companies which would go unnoticed. The US

Topics:

Angry Bear considers the following as important: CEPR, Dean Baker, DeanBaker, politics, social security, Taxes/regulation, US EConomics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

I have added little to this commentary.

Economist Dean Baker has taken a position on various aspects of the economy. A positive position which you will see many other commentaries trashing. We avoided one hell of a recession to date which would have been the equal to the 2008 collapse due to Wall Street’s addiction to gambling. You will not hear the news media promoting this. I will be posting more on this issue.

Meanwhile, there exists a lot of talk about SS draining the pockets of the young. There are no subsidies to Social Security today and is it ran short of funds in 2034, here are solutions such as MMT. We could avoid issues in 2034 by small incremental increases in SS taxes for both employees and companies which would go unnoticed. The US always prefers a catastrophe to get it to do something. Onward to Dean Baker . . .

Social Security and Medicare: Fun with Numbers Time, Center for Economic and Policy Research, Dean Baker

As a Thanksgiving present to readers, Washington Post columnist Catherine Rampell decided to tell us again how old-timers are robbing from our children with their generous Social Security and Medicare benefits. This is always a popular theme at the WaPo, especially around the holiday season.

The story is infuriating for four reasons:

- Even by the calculations highlighted in the piece, Social Security is not a big subsidy to retirees,

- Medicare appears to be a large subsidy only because our healthcare system is so inefficient,

- What counts as a government payment, as opposed to a market outcome, is arbitrary, and

- We pass on a whole society to our children, focusing on these programs to the neglect of the larger social and physical environment is close to absurd.

Social Security

The Social Security program has always been reasonably well-funded, even as slower growth and the upward redistribution of income over the last five decades have hurt the program’s finances. It is now facing a shortfall in a bit over a decade. Thebgap between scheduled benefits and taxes is not exceptionally large, as calculated by Gene Steurele and Karen Smith, Rampell’s source.

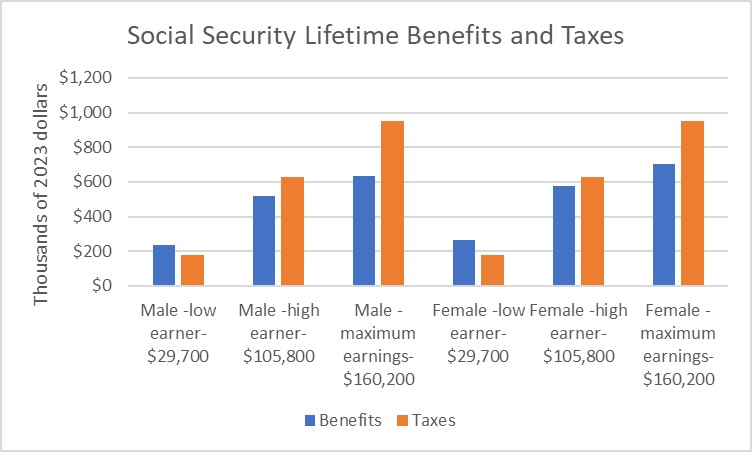

Source: Steurele and Smith, 2023.

The chart below above shows Steurele and Smith’s calculations for lifetime Social Security benefits and taxes, for people turning 65 in 2025, for men and women at different earnings levels. There are a few points worth noting on these calculations.

The calculations are highly stylized. They are assuming a worker puts in 43 years from age 22 to age 65 always earning the same wage relative to the overall average. This means that their wage rises year by year in step with inflation and the increase in average wages. No one actually would follow this pattern.

They are likely to earn less early in their career and more later in their career. They also are likely to have some years of little or no earnings. This is especially the case for women who are likely to spend some time outside of the paid labor force caring for children or parents. These adjustments would generally lead to higher benefits relative to taxes.

The second point is that the calculations assume that everyone lives to age 65 at which point they start to collect benefits. Some people will die before they can collect benefits, so we are looking at the benefits for workers who survive to collect benefits. (Social Security also has survivors’ benefits that go to spouses and minor children of deceased workers, so their tax payments are not necessarily a complete loss.)

The third point is that Steurele and Smith have opted to use a 2.0 percent real (inflation-adjusted) interest rate to discount taxes and benefits. This is a standard rate to use in this sort of analysis, but one could argue for a higher or lower rate. A higher rate would make the program seem less generous, while a lower rate would raise benefits relative to taxes.

As can be seen, they are projecting low earners will receive more in benefits than they pay in taxes. An important qualification here is that there is a large and growing gap in life expectancies between low and higher earners. These calculations assume that everyone of the same gender has the same life expectancy regardless of their income. This means the benefits will be somewhat overstated for low earners and understated for high earners.

Ignoring the life expectancy issue, the chart shows that projected benefits end up being less than taxes once we get to high earners ($105,800 in 2023). For men projected lifetime taxes exceed benefits by $106,000. For women the gap is smaller at $49,000, reflecting their longer life expectancy.

Moving to maximum earners, people who earn the income at which the payroll tax is capped ($160,200 in 2023), the gaps become larger. In the case of men, projected lifetime taxes exceed benefits by $319,000. For women, projected lifetime taxes are $249,000 more than benefits.

There are some simple takeaways we can get from the Steurele and Smith analysis. First, for low and middle-wage earners Social Security does indeed pay out more in benefits than workers pay in taxes. However, the gap is not very large. For average earners, who got $66,100 in 2023, (not shown to keep the size of the graph manageable), the gap is $3,000 for men and $46,000 for women.

For higher income earners taxes actually exceed benefits. In the case of maximum earners, these excess payments are actually fairly large, as noted $319,000 for men and $249,000 for women.

This raises an interesting issue, if we are looking to cut benefits to reduce the “subsidy” to the elderly provided by Social Security. We can cut back benefits by a substantial percentage for low earners to bring their lifetime benefits more closely in line with their lifetime taxes, but do we really want to reduce retirement benefits for people who had average earnings of $29,700?

We can make some cuts for more middle-income workers, but someone earning $66,100 during their working lifetime was not terribly comfortable, and there is not much subsidy here to start, especially with men. When we get to higher earners, taxes already exceed benefits. We can still make cuts to their benefits, but we would not be taking back a subsidy by this calculation, we would be increasing their net overpayment to the program.

It’s also worth noting who is a high earner in this story. The high earner had annual earnings of $105,800 in 2023. President Biden promised that he would not raise taxes on couples earning less than $400,000. That puts his cutoff of $200,000 at almost twice the high earner level, and the calculation of lifetime benefits and taxes turns negative at a considerably lower income than the stylized high earner.

These calculations show that if we just take Social Security in isolation and want to reduce the subsidy implied here we either have to cut benefits for people who are not living comfortably by most standards, or we have to cut benefits for people who are not currently receiving a subsidy. We may decide that the latter is good policy, but we should be clear that it is not taking back a subsidy.

There is an important qualification to this discussion. Married couples will generally do better in these calculations than single workers. This is because the spousal benefit allows the spouse to collect the greater of their own benefit or half of their spouse’s benefit. Also, a surviving spouse will receive the greater of their own or their deceased spouse’s benefit. For these reasons, lifetime benefits for couples will generally be higher relative to taxes than for single individuals.

The Medicare Subsidy and the Broken Healthcare System Story

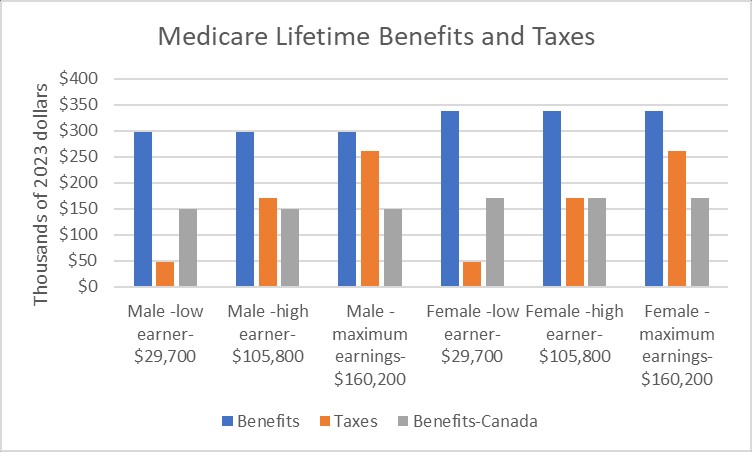

The Steurele and Smith analysis shows much larger subsidies for the Medicare program, as shown below.

There are a few qualifications to these calculations that should be noted. First, the same caveats about earnings patterns noted with the Social Security calculations also apply to the projected value of Medicare taxes.

Second, the differences in life expectancies by income matter here also when assessing the size of the tax penalty or subsidy. The program is less generous for low earners than shown in this figure and more generous for high earners.

The third point is, unlike the designated Social Security tax, the Medicare tax is not capped. This means people earning above the Social Security cap will be paying more taxes to support the program. For very high earners ($185,000 for men and $207,000 for women), projected taxes would exceed benefits. The size of the tax penalty increases further up the income scale.

Finally, high-income people also pay a designated Medicare tax on capital income, like dividends and capital gains. For these people, it is virtually guaranteed their Medicare taxes exceed their projected benefits.

With these caveats, we see the same general story as with Social Security, where there is more of a subsidy for lower earners than higher earners. While the overall gaps are larger for Medicare, projected benefits exceed taxes by a larger amount, this changes less with income than in the case of Social Security.

This is due to the fact that, unlike Social Security, the payout is not designed to be progressive, with all retirees getting in principle the same benefit.[1] This is qualified by the fact that higher-income retirees can expect to receive benefits for a considerably longer period of time, making the benefit regressive.

I have added a third bar to this graph, labeled “Benefits-Canada.” This is a calculation of what the cost of benefits would be if we paid the same amount per person for our healthcare as Canada does. The Medicare program appears as a huge subsidy to beneficiaries primarily because we pay so much more for our health care than people in other wealthy countries.

According to the OECD, we pay 57 percent more per person than Germany, 107 percent more than France, and 99 percent more than Canada. This sort of massive gap can be shown with U.S. costs relative to every other wealthy country. We don’t get any obvious benefit in terms of better healthcare outcomes from this additional spending. Life expectancy in the United States is considerably shorter than in most other wealthy countries.

The “Benefits-Canada” bar allows us to assess the value of Medicare benefits if our healthcare costs were more in line with those in other countries. It multiplies the projected value of Medicare benefits by the ratio of per person health care costs in Canada to costs in the United States (50.3 percent).

As can be seen, if we calculate Medicare benefits assuming we pay as much for our health care as people in Canada, most of the calculated subsidy goes away. Low earners still receive a substantial subsidy, $102,000 for men and $122,000 for women, but this quickly goes away higher up the income ladder.

If we assume Canadian health care costs, a high-earning male has a net Medicare tax penalty of $21,000, while a high-earning woman has a net tax penalty of just under $1,000. For those earning at the Social Security maximum, the net tax penalty for men is $111,000, and for women it’s $91,000.

The implication of this calculation is that the seemingly large subsidies that Medicare provides to retirees is not due to the generosity of benefits, it is due to the fact that we overpay for our healthcare. Medicare is not providing a large subsidy to retirees, it is providing a large subsidy for drug companies, medical equipment suppliers, insurers, and doctors. (In case you are wondering, people in the U.S. are not generally paid much more than people in other wealthy countries. Our manufacturing workers get considerably lower pay.)

We pay roughly twice as much in all of these categories as people in other wealthy countries. It is misleading to imply that these overpayments are generous to retirees. While all of these interest groups have powerful lobbies, which makes it politically difficult to bring their compensation in line with other wealthy countries, we should at least be honest about who is getting subsidized by the high cost of our Medicare program.

What Do Subsidies Mean, When the Government Structures the Market?

There is another aspect of these calculations that should have jumped out at people when I noted that the designated Medicare tax is not capped and also applies to capital income. The taxes that are designated for these programs are arbitrary. We can designate other taxes that people pay as being Social Security and Medicare taxes, and apparent subsidies will disappear.

In fact, the idea that we can make a clear distinction between income that people have somehow earned, and income that is given to them by the government, is in fact an illusion. The government structures the markets in ways that allow some people to get very wealthy and keep others on the edge of subsistence.

Those who make big bucks in the healthcare industry are just one example. While our trade policy was quite explicitly designed to open the door to cheap manufactured goods, we actually have increased the barriers that make it difficult for foreign-trained doctors to practice in the United States.

We have made patent and copyright monopolies longer and stronger. The government subsidizes bio-medical research and then gives private companies monopoly control over the product. In a recent example, we paid Moderna to develop a COVID vaccine and then gave them control over it, creating at least five Moderna billionaires.

We have allowed our financial sector to become incredibly bloated, creating many millionaires and billionaires, even as we demand efficiency elsewhere. We give Elon Musk and Mark Zuckerberg Section 230 protection against defamation suits that their counterparts in print and broadcast media do not enjoy.

And, as was recently highlighted with the UAW strike, our CEOs make far more than the CEOS of comparably sized companies in other wealthy countries. The difference is as much as a factor of ten in the case of Japanese companies. This is not due to the natural workings of the market, this is the result of a corrupt corporate governance structure that allows the CEOs to have their friends set their pay.

Yes, I am again talking about my book (it’s free). It is absurd to obsess about tax and transfer policy while ignoring the ways in which the government structures the market to determine winners and losers. It is understandable that the right would like tax and transfer policy to be the focus of public debate, since the default is a market outcome that leaves most money with the rich.

However, it is beyond absurd that people who consider themselves progressive would accept this framing. We can structure the market differently to get more equitable market outcomes. This should be front and center in public debate. Unfortunately, the right wants to hide the fact that we can structure the market differently, and progressives are all too willing to go along.

Future of the Planet

There is a final point on the sort of generational scorecard implied by these calculations of Social Security and Medicare benefits. We don’t just hand our children a tax bill, we hand them an entire economy, society, and planet.

If we experience anything resembling normal economic growth, average wages will be far higher twenty or thirty years from now than they are today. Will the typical worker see these wage gains? That will depend on distribution within generations, not between generations.

We also see costs from items like the military. When I was growing up in the 1960s we paid a much larger share of our GDP to support the Cold War. (Young men were also drafted.) We will again pay lots more money for the military if we have a new Cold War with China. The implied taxes don’t figure into the Social Security and Medicare calculations, but will be every bit as much of a drain on the income of people in the future as taxes for these programs.

And, we should always have global warming front and center. If we paid off the national debt and eliminated the programs to support retirees, but did nothing to restrain global warming, our children and grandchildren would not have much reason to thank us. First and foremost, we must give them a livable planet.

Phony Answers to a Phony Question

The whole subsidy to retiree story is a diversion from the many important issues facing the country. Even the core idea, that we don’t adequately support the young because we give too much to the elderly is wrong.

We saw this very clearly in the debate over the extension of the child tax credit. As with everything in Congress, much is determined by narrow political considerations. Republicans had no interest in giving President Biden and the Democrats a win, but the bill could have passed without Republican votes.

The deciding factor was the refusal of West Virginia Senator Joe Manchin to support the bill. Senator Manchin was very clear on his concerns. He didn’t argue that we were spending too much on retirees, he didn’t want low-income people to have the money.

This is in general the story as to why we don’t have adequate funding for early childhood education, children’s nutrition, day care and other programs that would benefit children. There is a substantial political bloc that does not want to fund these programs. And, they still would not want to fund these programs even if we didn’t pay a dime for Social Security and Medicare.

1 This is not strictly true, since the premium payment that retirees make for Part B and Part D of the Medicare program depends on income in retirement.