Who gets the money? Follow the assets. by Steve Roth Originally Published at Wealth Economics This post by Judd Legum at Popular Information (read and subscribe!) prompts me to revisit the issue of share buybacks. This passage in particular: It seems eye-popping. But is it? Even (especially?) finance and econ types don’t really understand buybacks from a big-picture, macro, national-accounting perspective. Here’s a shot at explaining it. Corporate “Wealth” is Household Wealth As is our wont here at Wealth Economics, let’s start with the household-sector balance sheet. It’s the only measure we’ve got of our collective, national wealth: assets and net worth. It’s the top of the accounting-ownership pyramid. Everything else

Topics:

Steve Roth considers the following as important: Buybacks, Taxes/regulation, US EConomics

This could be interesting, too:

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Bill Haskell writes Families Struggle Paying for Child Care While Working

Joel Eissenberg writes Time for Senate Dems to stand up against Trump/Musk

Who gets the money? Follow the assets.

by Steve Roth

Originally Published at Wealth Economics

This post by Judd Legum at Popular Information (read and subscribe!) prompts me to revisit the issue of share buybacks. This passage in particular:

It seems eye-popping. But is it? Even (especially?) finance and econ types don’t really understand buybacks from a big-picture, macro, national-accounting perspective. Here’s a shot at explaining it.

Corporate “Wealth” is Household Wealth

As is our wont here at Wealth Economics, let’s start with the household-sector balance sheet. It’s the only measure we’ve got of our collective, national wealth: assets and net worth. It’s the top of the accounting-ownership pyramid. Everything else “telescopes” onto that balance sheet. In the basic accounting, households are where “national” wealth “comes home.”

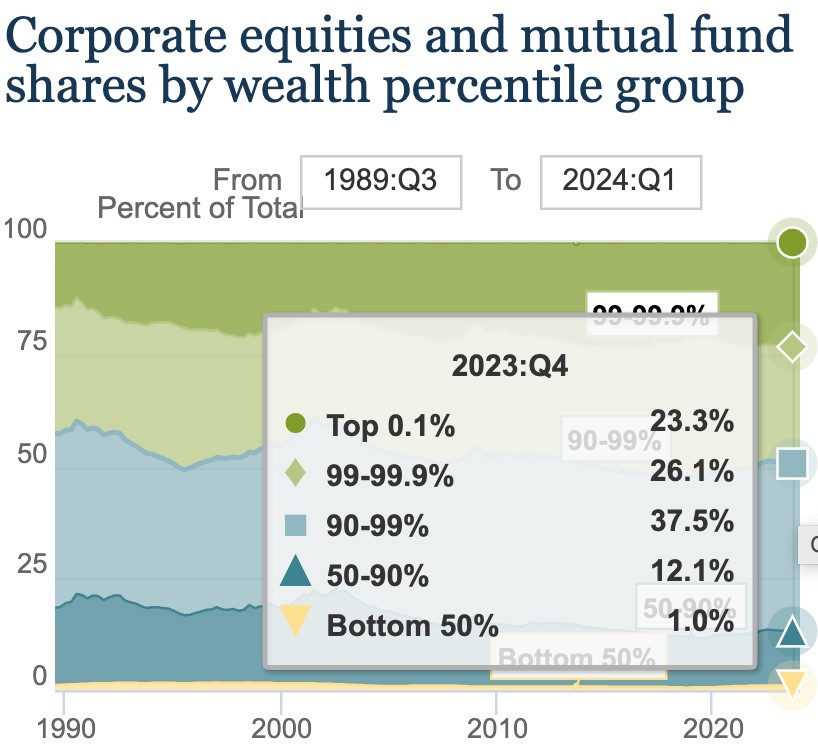

In particular: the household sector “owns” the firms sector. The “asset-cap” value of firms’ equity shares at current market prices sits on the household balance sheet as one asset category: equity shares — 90% of which are owned by the top-10% of wealthholders.

So when government delivers benefits to corporations (like subsidies or tax cuts), it’s ultimately delivering assets onto (top-10%) households’ balance sheets. The delivery mechanism might be dividends/distributions, interest payments (mostly to banks — which are also owned by top-10% shareholders), or via stock buybacks.

Buybacks are Just Asset Re-Allocation

Again, think about the balance sheets. When a firm buys back shares it transfers M assets to some households, who “give back” their shares (which disappear). The households that sell their shares have more M assets, and less equity shares. For them it’s just an asset swap — portfolio reallocation.

Meanwhile the firm is smaller; the cash outlay means it has less assets. But assuming some shareholders have exited, each remaining household that doesn’t sell back their shares holds a larger percent share of that smaller company — for net zero change in their assets. Their balance-sheet equity holdings, and portfolio allocations, are unchanged.

But: looking into the firm they still own, the composition and nature of their holdings has changed: the firm’s management is deciding, for shareholders, to swap cash in hand for more potential future reward — and risk. They’re “leveraging up.” (Often quite explicitly; actually taking out bank loans to fund the buybacks.) So in an only-somewhat stylized sense the remaining shareholders are just doing an asset-swap as well (mostly without even knowing it’s happening).

By contrast: distributions via dividends just deliver M assets to all shareholders. They all hold more M assets and less equity (again, because the distribution means the firm has less assets).

The Tax Issue

What about Trump’s once and future corporate tax cuts? First off (I’ve written about this before), buybacks are a massive tax-avoidance scheme. With dividends, all shareholders get income that they have to pay taxes on in full at the dividend/cap-gains rate (they’re currently the same). With a buyback, only the selling shareholders get cash, and they’re only taxed on the difference between their selling price and what they originally paid for the shares — their capital gains. Those de minimus taxes starve the beast — with the eternal right-wing goal of reducing government revenues so they can drown it in a bathtub.

So Judd Legum gets some excruciating details somewhat wrong, though the thrust is right. If firms get a tax cut, that straightforwardly benefits their (top-10%er) shareholders. The firms’ choice of distribution mechanism — dividends or buybacks — doesn’t change that. But with dividend distributions, at least more of that windfall government gift gets taxed back.

None of this addresses the other big issue with buybacks: price manipulation and “insider trading” by C-suiters. (Yet another big mechanism driving insane and increasingly concentrated wealth — The Great Satan.) I hope to come back to that issue in a future post.