Share the post "Three Things I Think I Think – Bubble Spotting Edition" Here are some things I think I am thinking about: 1) Dean Baker says bubble spotting is easy. Dean Baker was among the few people who spotted the housing bubble fairly early. In a recent blog post he goes through how he identified it and asserts that this was “easy”. He says it was inexcusable for policymakers to be blindsided by it. Hmmm. I don’t know about that. I remember the housing bubble quite well because I too was adamant that there was a bubble. I will never forget the first time I laid eyes on the Case Shiller real price adjusted housing chart around 2005. This was 100+ years of data with an outlier so huge that you had to be a buffoon to say this was anything normal. But I am not sure how useful that really would have been for policymakers. After all, by the time an asset bubble has developed and been identified it’s too late. Policymakers don’t have the tools to stop asset bubbles from mean reverting. I mean, what else could the Fed have done? They were raising rates rapidly. They were monitoring financial conditions and lending in the overnight market. But the Fed cannot control the quantity of loans that are made, how loans are made or how many people purchase homes.

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

Here are some things I think I am thinking about:

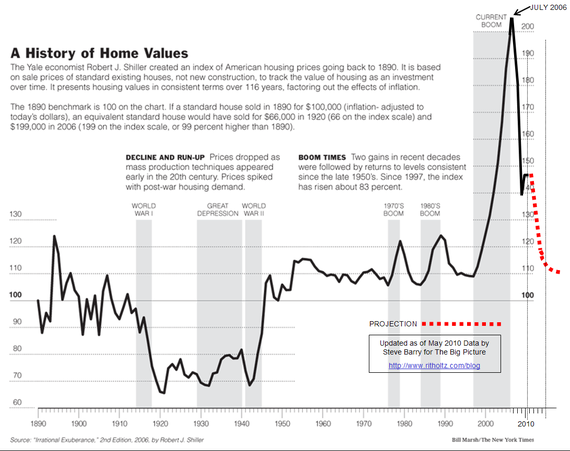

1) Dean Baker says bubble spotting is easy. Dean Baker was among the few people who spotted the housing bubble fairly early. In a recent blog post he goes through how he identified it and asserts that this was “easy”. He says it was inexcusable for policymakers to be blindsided by it.

Hmmm. I don’t know about that. I remember the housing bubble quite well because I too was adamant that there was a bubble. I will never forget the first time I laid eyes on the Case Shiller real price adjusted housing chart around 2005. This was 100+ years of data with an outlier so huge that you had to be a buffoon to say this was anything normal. But I am not sure how useful that really would have been for policymakers. After all, by the time an asset bubble has developed and been identified it’s too late. Policymakers don’t have the tools to stop asset bubbles from mean reverting.

{kind=link}

I mean, what else could the Fed have done? They were raising rates rapidly. They were monitoring financial conditions and lending in the overnight market. But the Fed cannot control the quantity of loans that are made, how loans are made or how many people purchase homes. These elements are outside of the control of policymakers yet we act like policymakers have this Archimedean Lever over the economy. It doesn’t quite work like that. The housing bubble might not have been difficult to identify, but no one knew how devastating it was going to be and policymakers certainly didn’t have tools that would have eliminated its negative impact.

2) Dean Baker says negative rates are stupid. (If you think I have a man crush on Dean Baker then you’re wrong). Now that that’s out of the way….He is dead right about negative interest rates. Dean says negative interest rates are a tax on the banking system that will just get passed on to bank customers.

This is one of those times where economic theory and reality totally diverge. In theory, the natural rate of interest is negative which means the price of money needs to be lower. So, if policy makers would just cut rates then we’d adjust the price of money back towards its equilibrium rate and the economy would adjust accordingly. Except this isn’t at all how the overnight interest rate influences the broader economy. If the Fed sets the overnight rate at a negative rate then banks are incurring a cost to maintain deposits. They might not pass this negative rate on directly to their customers (who would hold deposits they had to pay for), but they will raise other banking costs to try to maintain their profit margins. This just hurts depositors. How is that good for the economy?

We’re already seeing this happen around the world. The theory just doesn’t mesh with the reality. And while many economists keep revising their estimate of the natural rate of interest lower, they refuse to revise this theoretical concept out of their economic models.

3) I seem to have run out of Dean Baker related material so, since the world has had a pretty crappy week I’ll just leave this video of a fat panda falling all over the place to brighten your day: