Here are some things I think I am thinking about on this beautiful Saturday morning…. 1) Are buybacks propping up the stock market? One of the more annoying narratives going around these days is this idea that buybacks are propping up the stock market. I was reminded of this yesterday while reading a Ned Davis Research piece which said the stock market would be 19% lower without buybacks. Let’s think about this rationally…. This sort of thinking assumes a hyper inefficient market where corporations can essentially dupe investors into buying stock that is overpriced with no fundamental underlying support. It’s like we all know the S&P 500 should only be at 2,200, but we’re all just being kinda stupid and allowing ourselves to buy it at 2800. Now, I’m no efficient market lover, but I

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

Here are some things I think I am thinking about on this beautiful Saturday morning….

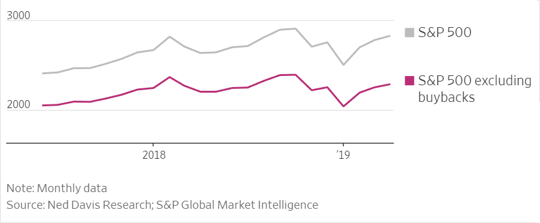

1) Are buybacks propping up the stock market? One of the more annoying narratives going around these days is this idea that buybacks are propping up the stock market. I was reminded of this yesterday while reading a Ned Davis Research piece which said the stock market would be 19% lower without buybacks. Let’s think about this rationally….

This sort of thinking assumes a hyper inefficient market where corporations can essentially dupe investors into buying stock that is overpriced with no fundamental underlying support. It’s like we all know the S&P 500 should only be at 2,200, but we’re all just being kinda stupid and allowing ourselves to buy it at 2800. Now, I’m no efficient market lover, but I also don’t think the market is hyper inefficient like this. I mean, people do lots of stupid things, but I don’t believe markets are this stupid. Said differently, when corporations buy back shares I think investors consider all the other factors that impact corporate earnings and come to the conclusion that a share repurchase is not harmful to future fundamentals. In other words, the market prices the return of cash pretty much the way it should.

Furthermore, share buybacks are a cash distribution from retained earnings just like dividends are. All else equal, this should INCREASE future corporate profits since this cash distribution is now available for the selling shareholder to spend. So, while a share repurchase or dividend decreases the cash balance at one entity it frees up that cash balance to be spent on other goods and services thereby adding to the profits of another firm (assuming the selling shareholder doesn’t also save the cash). In essence, a corporation that buys back shares is saying “hey, we have all this saved up cash that we can’t find anything smart to do with so you take it and do something with it!”. This should be an aggregate good for the economy since the company is disbursing cash it would otherwise hold under the mattress. So, there’s a real fundamental reason that buybacks are good for corporations and the economy because they return cash that the corporation would otherwise save. In this sense, buybacks aren’t just “financial engineering” and the presumed manipulation that goes with the narrative that buybacks “prop up” the stock market.

So, do buybacks prop up the stock market? If you mean that cash disbursements are some sort of manipulative market action then I think that’s wrong. Do buybacks make the stock market higher than it otherwise would be? Probably, because the corporations are returning cash they would otherwise retain thereby adding to future corporate profits. So, it’s fine to say that the stock market is higher than it might otherwise be, but that’s because there’s a perfectly rational reason for it – in the aggregate buybacks return cash and add to corporate profits in the the same way that dividends add to future profits by giving saved corporate cash to households who can now spend it back into the economy.

2) China is going to dump their T-Bonds and crash the bond market. I feel like I’ve been debunking this narrative for most of the last decade, but like many market myths it just doesn’t die.¹ In any case, here’s a story about that.

Let’s think about this rationally. The US T-Bond market does about half a trillion dollars a day in volume. China holds about $1.1T of T-Bonds. So, that’s about 2 day’s worth of volume. Now, this is by no means a small amount. But we have to be careful about the narrative around flow of funds because this is one of the most nefarious myths around. The basic thinking is that China can control the market because they are a large buyer. We see narratives like this all the time where people assume that large flows mean that the flows will control the fundamentals. But this puts the cart before the horse in the exact same way that the misconceptions about buybacks does. Just like a buyback does not necessarily impact the fundamentals of the underlying corporation, neither does China’s buying and selling of T-Bonds impact the underlying fundamentals of T-Bonds.

Now, in a very crude sense, the pricing of T-Bonds is simple. In essence, bond buyers look at the rate of inflation and price bonds to be compensated for incurring that risk plus some buffer. So, T-Bonds pretty much always sell at the rate of inflation plus a premium. If T-bonds are sold at a yield of 3% tomorrow and inflation is 2% then the bond buyer has about a 1% real buffer. Not great, but better than cash and over time it has about the same credit risk. Now, if China decides they’re going to sell all of their bonds and yields jump to 4% then that is going to result in a huge imbalance of demand from buyers who see that juicy 2% inflation buffer as too good to pass up. In other words, millions of buyers like me will suddenly pounce on this opportunity to improve their risk free real returns. This will presumably drive the price back down. In fact, it should drive the price right back down to where it was before since nothing fundamentally changed about the T-Bond market, the economy or future inflation risk. The idea that yields will jump to 4% and stay there can only hold if China fundamentally changes something about the economy or the bond market. Of course, they don’t so there’s no reason to assume prices wouldn’t correct back to where they were before.

There are lots of other reasons why China won’t sell their T-Bonds, but we should be very clear about the pricing dynamics here. China cannot crash the bond market because their secondary market buying and selling will not change the fundamentals of the US government, the US economy or really anything. So there’s no reason to panic over this.

3) It’s Rubio! Here’s a report from Marco Rubio trashing the idea of maximizing shareholder value, buybacks and other stuff. He cites far left wing economists extensively which is pretty strange. There’s really no nice way of putting this – Marco Rubio has to be one of the most confused politicians around.²

Now, I’ve covered the many myths around maximizing shareholder value in the past (see here). In short, left wing economists have confused all sorts of basic financial concepts en route to demonizing corporations for trying to earn a profit. The buyback demonization is a common one. Short-termism is another one. This one’s easy to debunk so let’s just focus on that for a second.

The basic idea around short-termism is that corporations focus too much on the short-term when managing the company. This supposedly leads to excessive share repurchases to boost near-term EPS and can incentivize executives to be paid in stock which they “manipulate”. But a corporation is a perpetual entity. Its long-term viability is the result of its short-term actions. And if these short-term actions are fundamentally bad for the corporation then the company will not succeed in the long-term. In other words, if you think buybacks are manipulative and bad for corporations or that executive comp via share issuance is bad then you should pray for these corporations to mismanage their cash in this manner because that means these corporations will become less competitive and potentially go out of business.

Of course, the whole reason corporations perform buybacks is because they’re generally successful and end up with more cash than they know what to do with. These firms are successful precisely because their operations have been so successful in the long-term that they end up with what looks like a short-term problem of having to return massive amounts of cash to shareholders. Basically, the firm thinks so long-term that they now have a short-term problem of excess cash flow. So, none of this even makes sense in the first place.

Now, in fairness, Rubio is touching on an important issue. Corporations do save too much. They aren’t investing enough. But that’s not because of the concept of shareholder value maximization and short-termism. It is, ironically, largely due to policies enacted by Conservatives like Marco Rubio who give trillion dollar tax cuts to corporations and allow nonsense like trickle down economics to persist.

¹ – Ah, this is probably because I’ve been writing about this exact topic for the last decade.

² – I know Donald Trump exists. You don’t have to remind me.