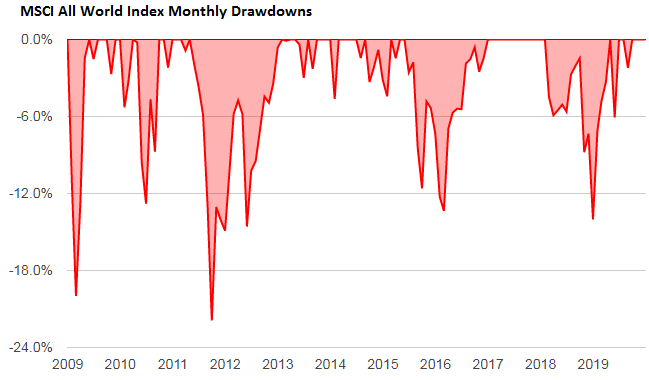

The stock market was sneaky strong this past year. The MSCI All World Index was up 27% in 2019. The S&P 500 was up 31%. Those are big numbers when you consider that the global stock market averaged a return of about 6% in the last 10 years and 8.5% in the last 15 years. It’s often tempting to look at an environment like the current one and think “gosh, I should have been more aggressive, maybe I should be more aggressive in the future?” Now, this might not be an inappropriate mentality. But you have to keep things in perspective. Even if we exclude the 50%+ declines during the financial crisis the MSCI All World Index still suffered six 10%+ drawdowns during the current bull market. (Source: Portfolio Visualizer) This is important because, as I’ve described previously, the stock

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

The stock market was sneaky strong this past year. The MSCI All World Index was up 27% in 2019. The S&P 500 was up 31%. Those are big numbers when you consider that the global stock market averaged a return of about 6% in the last 10 years and 8.5% in the last 15 years. It’s often tempting to look at an environment like the current one and think “gosh, I should have been more aggressive, maybe I should be more aggressive in the future?” Now, this might not be an inappropriate mentality. But you have to keep things in perspective. Even if we exclude the 50%+ declines during the financial crisis the MSCI All World Index still suffered six 10%+ drawdowns during the current bull market.

(Source: Portfolio Visualizer)

This is important because, as I’ve described previously, the stock market has to fall in order for its rises to be sustainable. To experience the long-term good you have be willing to experience the short-term bad. Sometimes that bad is really really bad. And typically those really bad periods are when everything is bad which is what makes stock market crashes so behaviorally risky – they compound your financial risks at the exact wrong times in life.

This is why you need to be skeptical of the lure to chase returns. I always tell people to bring things back to first principles and remember why you allocate your savings in the first place:

- Remember, the financial markets are not where we get rich. We get rich making real investments on primary markets earning a living and selling actual goods and services to other people. Then we take some of that saved income and allocate it to secondary markets like the stock and bond market in a manner that helps us achieve some financial goal. Therefore, it is always better to think of your portfolio as a savings portfolio and not some high flying sexy “investment” portfolio.

- A Savings portfolio doesn’t mean no risk. Your savings portfolio doesn’t need to be ultra boring like a savings account. But it probably needs some balance of capital preservation and capital growth. This is why leaning too heavily towards the stock market can be risky. While it gives you more capital growth potential it exposes you to excess preservation risk.

- Try to establish a target return. Most people don’t need double digit returns in their savings portfolio. Of course that would be nice, but again, that means the bad will come with the good. In my experience most people actually need far lower returns than they think. Over the course of my career I consistently find that people need a stable real return (maybe 4-6%) and often have unrealistic dreams of stable 10% returns (returns you’ll only get in the stock market and returns that certainly won’t be stable). More importantly, by sacrificing some of the upside you will often increase your long-term returns by helping avoid the behavioral mistake that people make by being too aggressive.

- Find your max pain point. Most people cannot stomach their net worth falling by 20%+. This means they cannot stomach a very high stock market allocation. That’s fine. A 50/50 stock/bond portfolio generated 7.5% per year in the last 10 years and had just one 12% drawdown. It achieved 68% of the upside of the stock market with 50% of the volatility. There’s nothing wrong with taking a more balanced approach if it helps you sleep better at night.

The good times are good for a reason. Things are getting better. Don’t get me wrong. I am not super pessimistic or anything like that. But you have to keep yourself grounded when times are good because it’s the booms that sow the seeds for busts. No one knows when the bust will come but one thing is for certain – you don’t want to find out what your real risk profile is when the bust is happening because that’s when you’ll make all the emotional mistakes that often lead to financial ruin. So keep your expectations realistic and don’t let a big bull market lure you into doing something that might create an inconsistency with your financial goals and your behavioral profile.