I’ve always loved Harry Browne’s Permanent Portfolio. The concept is so simple and clean – own equivalent ratios of assets that protect you in an “all weather” fashion: 25% stocks for growth/expansions 25% bonds for income/deflations 25% cash/t-bill for liquidity/recessions 25% gold for inflation hedging This portfolio is a close approximation of a Global Market Portfolio. It’s simple, diverse and covers all the bases that we might expect to encounter across an economic cycle. It’s also low fee and it’s got a ton of evidence and historical support to reinforce the concepts. My only beefs with the Permanent Portfolio are that this time might truly be different from when Browne created the portfolio in the 1980s mainly because: 0% interest rates mean that 25% of your money in cash/t-bills

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

I’ve always loved Harry Browne’s Permanent Portfolio. The concept is so simple and clean – own equivalent ratios of assets that protect you in an “all weather” fashion:

- 25% stocks for growth/expansions

- 25% bonds for income/deflations

- 25% cash/t-bill for liquidity/recessions

- 25% gold for inflation hedging

This portfolio is a close approximation of a Global Market Portfolio. It’s simple, diverse and covers all the bases that we might expect to encounter across an economic cycle. It’s also low fee and it’s got a ton of evidence and historical support to reinforce the concepts. My only beefs with the Permanent Portfolio are that this time might truly be different from when Browne created the portfolio in the 1980s mainly because:

- 0% interest rates mean that 25% of your money in cash/t-bills is way too much for most people.

- Gold relies on a monetary “faith put” that exposes 25% of your future returns to the risk that this “faith put” recedes or disappears.

I could write 100 pages on this portfolio and its pros and cons, but I want to focus on that last point – the faith put in gold.

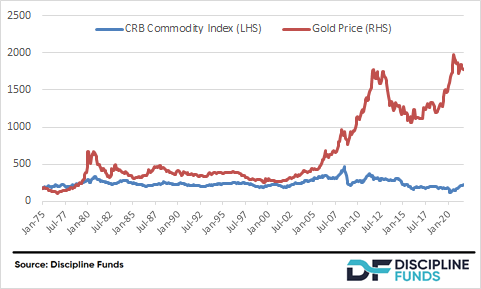

The basic argument is that gold has long been viewed as a monetary alternative to fiat money. Gold, at its core, is just another commodity and has real economic utility like other commodities. But gold has trounced other commodities historically. One explanation for this outperformance is that there is excess demand for gold because it’s become an alternative form of “money”. In short, gold has a long history of being a viable decentralized form of money that can serve as an alternative to centralized fiat money.

Enter Cryptocurrencies

One of the corollaries between cryptocurrencies and gold is that, as forms of money, they’re both grounded in the same decentralized concepts that make them useful alternatives to fiat. Gold has obvious impediments to its monetary utility in a modern economy – mainly the fact that its difficult to transport. Cryptocurrency fixes that. Personally, I find the long-term inflation hedging benefits of crypto to be somewhat less beneficial than many proponents believe. After all, all crypto is endogenous in the sense that it is literally created from nothing and can be borrowed into existence in exactly the same way that modern banks create synthetic “dollars” from nothing when they make loans. A “fractionally reserved” Bitcoin system with endogenous lending could be every bit as inflationary as the current fiat system with the main difference being that there isn’t a government there to pump trillions into the system on a whim. And that’s where the last 18 months and inflation hedging is pretty interesting….

A strange thing happened during COVID. The US government spent $6T to fight off the pandemic. As expected, the huge fiscal stimulus led to a somewhat uncomfortable level of inflation. But here’s where things get interesting – since the start of the pandemic in March 2020 the price of gold is up 6.5%. The price of Bitcoin, on the other hand, is up almost 10X. It’s not just a small difference. It’s an astounding difference. It’s the kind of difference that makes you wonder if people even believe that gold is an inflation hedge.

My personal view is that gold is absolutely money – a medium of exchange. But gold isn’t a good form of money because it’s an antiquated type of monetary alternative in a digital economy. Cryptocurrencies fix that even though they don’t necessarily fix the inflation issue. But I don’t think that matters. The fact that cryptocurrencies operate as a better medium of exchange means that the demand for them will dramatically outstrip the demand for gold as a medium of exchange.

But this is where the faith put premium gets interesting. If you believe, like me, that gold is mostly just a commodity with a monetary faith put then there’s a perfectly reasonable explanation for why gold has trounced commodities for several decades – in short, gold was always viewed as THE monetary alternative because it was the best option in a post gold standard mostly physical world. Therefore, it earned a premium over its basic commodity utility.

But when we look at the last 18 months we have to now ask ourselves why the CRB Commodity Index rose by 80% while gold did virtually nothing? Well, one partial explanation is that gold didn’t rise in value in the 18 months in large part because the “faith put” is transferring. In other words, a huge number of people are now actively selling gold in exchange for cryptocurrencies and primarily Bitcoin. As a result, the price of gold languished during a commodity boom in part because the faith put is reversing.

Am I right? I don’t know. But this is a fascinating potential sea change in alternative monetary theory as well as portfolio management. After all, if the faith put in gold is dying then we’re in the early process of a generational shift in the way people hedge their portfolios and view money.

About Post Author