Here are some things I think I am thinking about: 1) Is The Bond Bear REALLY Over Now? JP Morgan issued a bottom call in bonds yesterday. The basic thesis is that the Fed has shocked financial markets with its aggressive position on rates and the needed effect will filter through the economy and inflation data in the coming year. I largely agree with this. In February I said that rates would likely peak out around 2.5% on the 10 year and they’re currently at 2.85% so we’ve gone a little further than I expected. I’ve actually been shocked by the Fed’s aggressive rhetoric and to be honest I find it a little reckless and so far behind the curve that they’re creating very serious recession risk. My general thinking there is that we’re nearing the level where the relative 30 year mortgage

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

Here are some things I think I am thinking about:

1) Is The Bond Bear REALLY Over Now?

JP Morgan issued a bottom call in bonds yesterday. The basic thesis is that the Fed has shocked financial markets with its aggressive position on rates and the needed effect will filter through the economy and inflation data in the coming year. I largely agree with this. In February I said that rates would likely peak out around 2.5% on the 10 year and they’re currently at 2.85% so we’ve gone a little further than I expected. I’ve actually been shocked by the Fed’s aggressive rhetoric and to be honest I find it a little reckless and so far behind the curve that they’re creating very serious recession risk. My general thinking there is that we’re nearing the level where the relative 30 year mortgage (5-6%) puts a damper on the housing market and that going much higher would put the economy into recession.

My bigger concern now is that the Fed’s aggressive positioning creates the risk of a hard landing. In other words, they were behind the curve raising rates and then the inflation surprised them. So now they have to try to make up for lost ground, but in doing so they’re shocking the economy inside of a very brief window which has involved $35T of global asset price declines and surging unaffordability in real estate and other areas of the credit markets. So, instead of this methodical and surgical sort of stimulus unwind we’re just ripping the band-aid off.

Anyhow, all of this means that the worst of the bond bear market is likely over. Or, at least we won’t see the same level of volatility in high quality bonds because interest rate risk has declined. Of course, now we have to worry about whether interest rate risk will evolve into credit risk, but that’s a whole other matter.

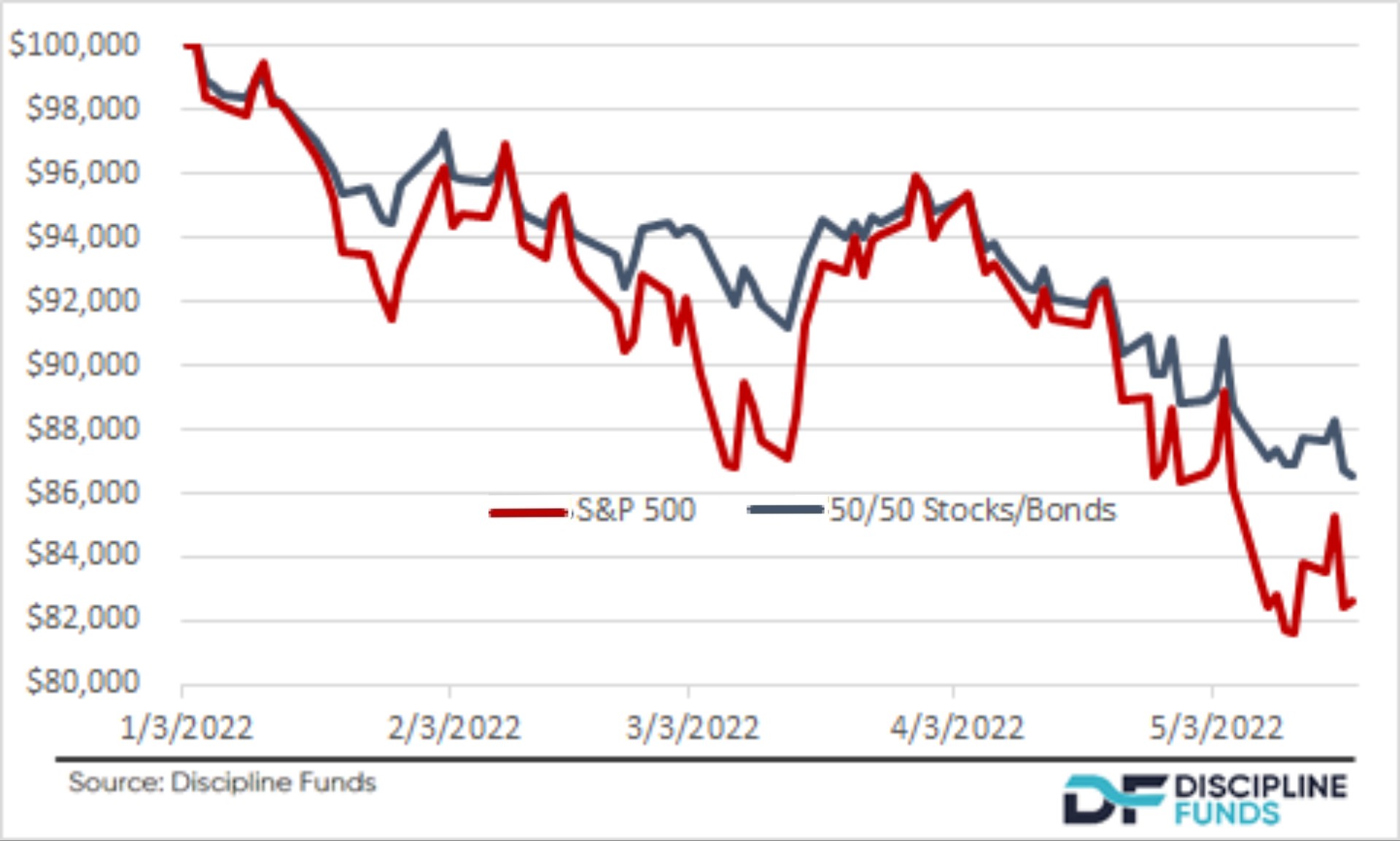

2) Bonds are STILL Working.

Speaking of bonds – they’re still doing their job. The S&P 500 is down 18.2% year-to-date. But a 50/50 stock/bond portfolio is down just 13.4% because bonds have outperformed stocks by a large margin despite the worst bond bear  market in decades. This is massively underdiscussed in this market. Even with a historic downturn in bonds you’re still getting almost 5% of outperformance from a diversified allocation to bonds.

market in decades. This is massively underdiscussed in this market. Even with a historic downturn in bonds you’re still getting almost 5% of outperformance from a diversified allocation to bonds.

And this is likely to become even more magnified if the stock decline continues because bonds, in the long-run, are just fixed income streams. The longer you hold them the less volatile they become. The only reason Q1 was such a volatile period for bonds is because we had a historically sharp interest rate jump in a very short amount of time. But now it’s becoming clear that the economy is slowing and inflation is likely to moderate. If anything the likelihood of policy easing is rising now as the risk of recession increases. This means that if the stock market continues to remain rocky this year the outperformance of bonds is likely to become even more exaggerated.

In fact, I am relatively excited about bonds for the first time in a long while. I’d been writing, for years, that I was having trouble constructing conservative portfolios that could meet a 4% withdrawal rule, but with the rise in rates that’s no longer a problem.

3) Virtue signaling investment strategies.

I’ve written a decent amount about ESG investing in the past. My general view is that you shouldn’t moralize your investing. In short, the only relevant metric for moralizing investments is legality. If the business is legal then it’s deemed moral by the government. For instance, we might argue that Exxon Mobil is an immoral company because they use fossil fuels. Sure, but XOM also helps make the fuel that literally drives a lot of the global economy. Or, a better example might be that XOM is now one of the largest investors in renewable energies. We can moralize about how we subjectively analyze a business, but the reality is that “morality” is a great big gray area and what’s moral to you might be immoral to someone else. And when you start getting morally emotional about your investments you become a stock picker. And when you become a stock picker you become someone who earns lower after tax returns than someone who indexes. And then your moralizing actually hurts your bottom line which hurts your ability to do good in the world.

My general view on ESG investing is that it’s mostly virtue signaling. It’s a subjective approach to moralizing certain firms in the process of selling the appearance of “doing good” when most of the ESG funds that exist are really just high fee versions of index funds. And it’s no surprise that ESG funds have gotten absolutely clobbered in the last year as they divested huge amounts of the market in what amounts to little more than a game of stock picking with higher fees.

Anyhow, I was gob smacked by all of this as I read how Tesla was being dropped by ESG funds because they no longer meet the subjective criteria assigned by S&P. Or, along similar lines, please read this entire article about whether we need to moralize Mayonnaise because it might be perceived as evil. Sigh.

Look, don’t get me wrong. I am not a bad person just because I am defending Mayonnaise and Tesla. I don’t even like Mayo, but we need to be really careful about how we mix our politics, emotions and biases with our investing strategies. There are good places to use your money in a morally conscious manner – the stock market isn’t that place.

About Post Author