Busting the natural rate of unemployment myth Almost sixty years ago Milton Friedman wrote an (in)famous article arguing that (1) the natural rate of unemployment was independent of monetary policy and that (2) trying to keep the unemployment rate below the natural rate would only give rise to higher and higher inflation. The hypothesis has always been controversial, and much theoretical and empirical work has questioned the real-world relevance of the idea that unemployment is independent of monetary policy and that there is no long-run trade-off between inflation and unemployment. My own view on the subject is that the natural rate hypothesis does not hold water simply because the relations it describes have never actually existed. The only thing that

Topics:

Lars Pålsson Syll considers the following as important: Economics

This could be interesting, too:

Lars Pålsson Syll writes Schuldenbremse bye bye

Lars Pålsson Syll writes What’s wrong with economics — a primer

Lars Pålsson Syll writes Krigskeynesianismens återkomst

Lars Pålsson Syll writes Finding Eigenvalues and Eigenvectors (student stuff)

Busting the natural rate of unemployment myth

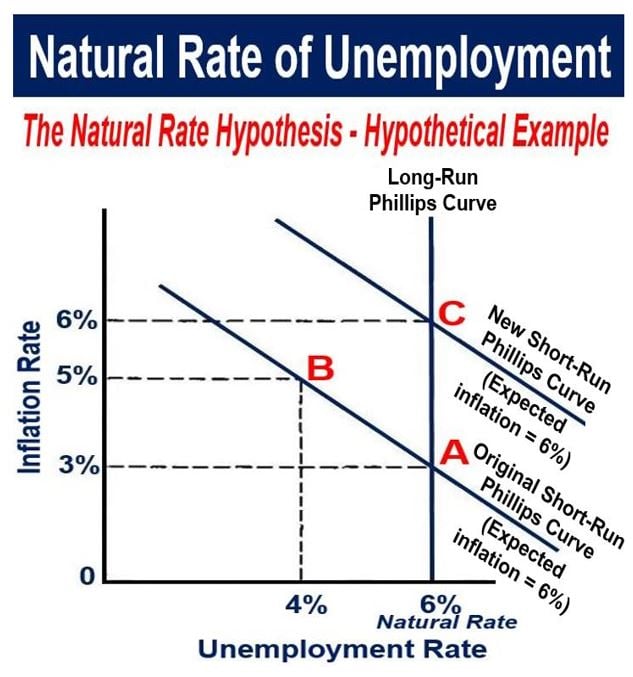

Almost sixty years ago Milton Friedman wrote an (in)famous article arguing that (1) the natural rate of unemployment was independent of monetary policy and that (2) trying to keep the unemployment rate below the natural rate would only give rise to higher and higher inflation.

The hypothesis has always been controversial, and much theoretical and empirical work has questioned the real-world relevance of the idea that unemployment is independent of monetary policy and that there is no long-run trade-off between inflation and unemployment.

The hypothesis has always been controversial, and much theoretical and empirical work has questioned the real-world relevance of the idea that unemployment is independent of monetary policy and that there is no long-run trade-off between inflation and unemployment.

My own view on the subject is that the natural rate hypothesis does not hold water simply because the relations it describes have never actually existed.

The only thing that amazes yours truly is that although this is pretty common knowledge, so-called ‘New Keynesian’ macroeconomists still today use it — and its cousin the Phillips curve — as a fundamental building block in their models. Why? Because without it ‘New Keynesians’ have to give up their (again and again empirically falsified) neoclassical view of the long-run neutrality of money and the simplistic idea of inflation as an excess-demand phenomenon.

The natural rate hypothesis approach (NRH) is not only of theoretical interest. Far from it.

The real damage done is that policymakers who take decisions based on NRH models systematically implement austerity measures and kill off economic expansion. The unnecessary and costly unemployment that this self-inflicted and flawed illusion eventuates, is something New Classical and ‘New Keynesian’ advocates should always be kept accountable for.

If the [NRH] and rational expectations are both true simultaneously, a plot of decade averages of inflation against unemployment should reveal a vertical line at the natural rate of unemployment … This prediction fails dramatically.

There is no tendency for the points to lie around a vertical line and, if anything, the long-run Phillips is upward sloping, and closer to being horizontal than vertical. Since it is unlikely that expectations are systematically biased over decades, I conclude that the [NRH] is false …