These two banks are taking today about a combined B loan loss reserve from the Wuhan Virus... Citi and BofA reporting later this week probably count them in for another B so maybe B total from the 4 money centers... so far... Chase Bank & Wells Fargo Prepare for MASSIVE Round of Defaults on Credit Cards, #Mortgages & Business Loans... https://t.co/8puIWQm0CJ #ChaseBank #WellsFargo #recession #CreditCards #SBAloans — The Altruist Party - Economic Sustainability (@APCommerce1) April 14, 2020 This will act to reduce the bank system assets by the same amount.... so banking system Residual Value (A-L) will drop by the B plus what the rest of the system estimates for losses due to the virus... Here is a short paper from the Richmond Fed on the accounting treatment for this type

Topics:

Mike Norman considers the following as important:

This could be interesting, too:

Robert Vienneau writes Austrian Capital Theory And Triple-Switching In The Corn-Tractor Model

Mike Norman writes The Accursed Tariffs — NeilW

Mike Norman writes IRS has agreed to share migrants’ tax information with ICE

Mike Norman writes Trump’s “Liberation Day”: Another PR Gag, or Global Reorientation Turning Point? — Simplicius

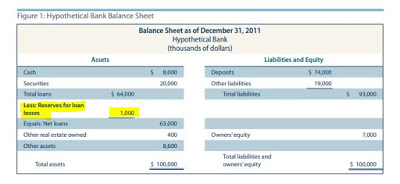

These two banks are taking today about a combined $10B loan loss reserve from the Wuhan Virus... Citi and BofA reporting later this week probably count them in for another $10B so maybe $20B total from the 4 money centers... so far...

Chase Bank & Wells Fargo Prepare for MASSIVE Round of Defaults on Credit Cards, #Mortgages & Business Loans... https://t.co/8puIWQm0CJ #ChaseBank #WellsFargo #recession #CreditCards #SBAloans— The Altruist Party - Economic Sustainability (@APCommerce1) April 14, 2020

This will act to reduce the bank system assets by the same amount.... so banking system Residual Value (A-L) will drop by the $20B plus what the rest of the system estimates for losses due to the virus...

Here is a short paper from the Richmond Fed on the accounting treatment for this type of transaction; you can see these transactions act to REDUCE the value of Loan Assets at the banks and will thus reduce Residual (A-L) and the total Leverage Ratio (A-L)/A .... these developments are accordingly generally bearish for risk assets...

You have to monitor the Fed's weekly bank reports as the weeks and perhaps months go by to see how bad this is going to get for Banking System Residual and Leverage...