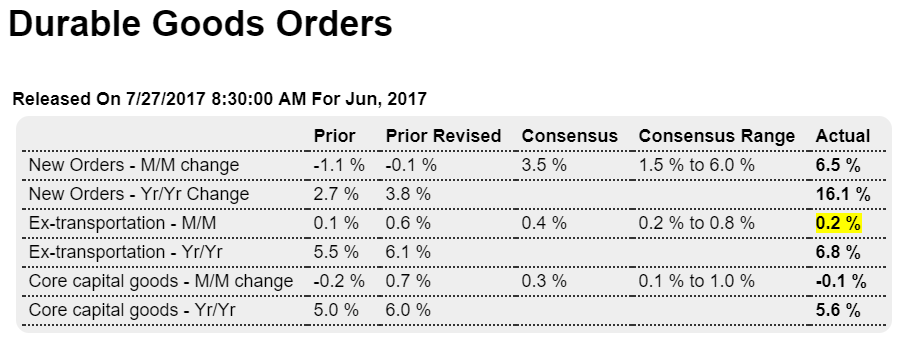

The theme of today’s data seems to be higher q2 gdp than otherwise, but for the wrong reason- over production- as spending weakened and unwanted inventories rose. Nice headline number for durable goods orders but most of the gain was in civilian aircraft which happens every year about this time. However, as previously discussed, the manufacturing sector is chugging along at modest levels after the large dip from the drop in oil related capital expenditures about 2.5 years ago: Highlights Aircraft orders don’t dribble out day by day, they come in big monthly batches and an especially big one in June that masks otherwise mixed results. Total orders surged 6.5 percent to top Econoday’s consensus for a 3.5 percent gain and high estimate for 6.0 percent. But when excluding

Topics:

WARREN MOSLER considers the following as important: Uncategorized

This could be interesting, too:

tom writes The Ukraine war and Europe’s deepening march of folly

Stavros Mavroudeas writes CfP of Marxist Macroeconomic Modelling workgroup – 18th WAPE Forum, Istanbul August 6-8, 2025

Lars Pålsson Syll writes The pretence-of-knowledge syndrome

Dean Baker writes Crypto and Donald Trump’s strategic baseball card reserve

The theme of today’s data seems to be higher q2 gdp than otherwise, but for the wrong reason- over production- as spending weakened and unwanted inventories rose.

Nice headline number for durable goods orders but most of the gain was in civilian aircraft which happens every year about this time. However, as previously discussed, the manufacturing sector is chugging along at modest levels after the large dip from the drop in oil related capital expenditures about 2.5 years ago:

Highlights

Aircraft orders don’t dribble out day by day, they come in big monthly batches and an especially big one in June that masks otherwise mixed results. Total orders surged 6.5 percent to top Econoday’s consensus for a 3.5 percent gain and high estimate for 6.0 percent. But when excluding transportation equipment that includes a 131 percent surge in civilian aircraft, orders could manage only a 0.2 percent gain which is below the 0.4 percent consensus and just making the low estimate.

But tipping the balance back in favor of strength is a 1 point upward revision to May where the decline is now only 0.1 percent. The ex-transportation reading gets a 1/2 point upward revision to a 0.6 percent gain with core capital goods (nondefense ex-aircraft) really showing strength, now at plus 0.7 percent vs a small initially reported decline.

But the readings for June aren’t that great with core capital goods moving back into the negative column at minus 0.1 percent. Other areas of weakness include motor vehicles which have been suffering and where the June decline is a sizable 0.6 percent.

For the second-quarter as a whole, however, June’s non-aircraft weakness is offset by the big gains in May. And specifically for Friday’s GDP report, a 0.4 percent June rise in inventories will be a solid plus with a 0.2 percent rise for shipments of core capital goods, that follows 0.4 and 0.2 percent gains in May and April, a modest plus.

But for forward momentum, the weakness in June doesn’t point to building strength for July. Durable orders have not been consistently strong this year though there are more favorable aspects to today’s report than unfavorable with the second-half outlook for the up-and-down factory sector now a bit more upbeat.

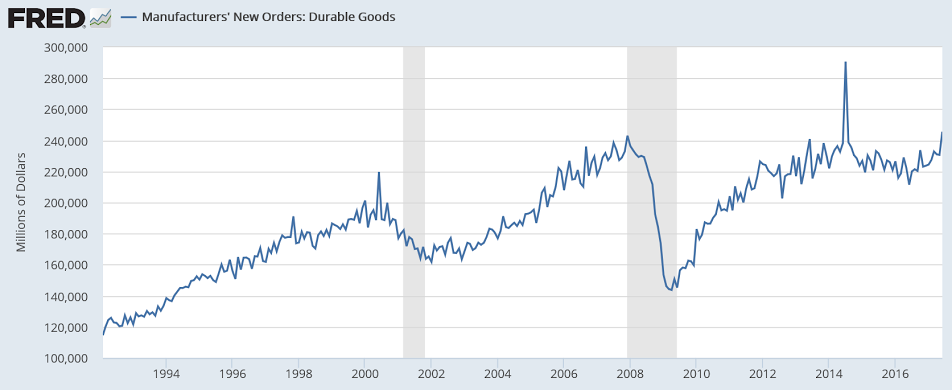

This chart is not adjusted for inflation:

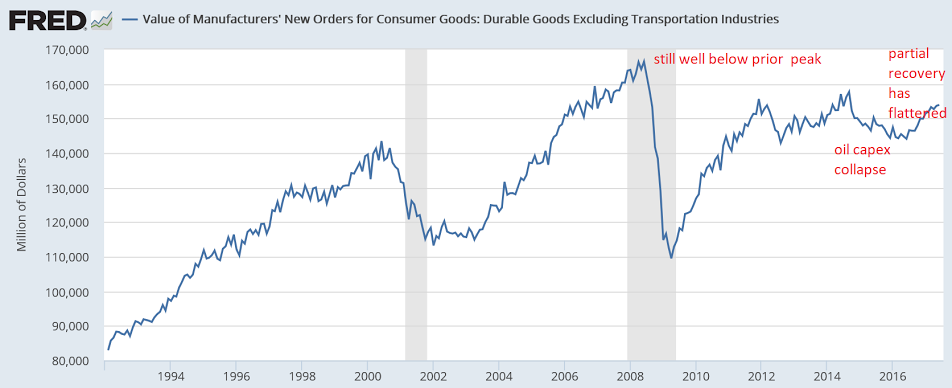

Not including aircraft orders:

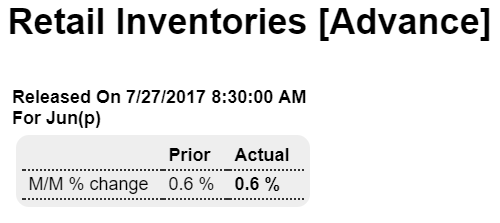

Looks like spending shortfalls are resulting in unsold inventories (not good):

Highlights

Retail inventories will be adding to second-quarter GDP, rising 0.6 percent in both June and May. Rising inventories are a plus for GDP but a challenge for retailers where sales have been flat and suggest that the inventory build may be unwanted.

Same here:

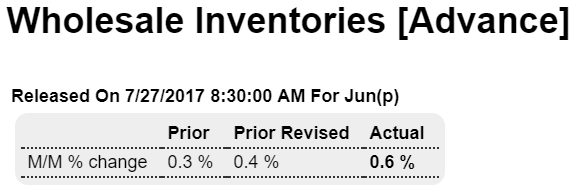

Highlights

Wholesale inventories in June are a plus for second-quarter GDP, rising a sizable 0.6 percent following May’s revised 0.4 percent build.

More signs of a weakening US consumer, as imports of consumer goods fell as domestic

inventories rose:

Highlights

Net exports in second-quarter GDP look to get a break as June’s goods deficit is a smaller-than-expected $63.9 billion vs expectations for $65.0 billion. Exports surged 1.4 percent in June led by food products but also including a big gain for capital goods exports and also vehicle exports. Imports of goods fell 0.4 percent with sizable declines for industrial supplies and consumer goods.

In another plus for second-quarter GDP, advance data on wholesale and retail inventories, which were also released with the goods report, both rose 0.6 percent.

The burst in exports is a positive not only for GDP but for a factory sector which, as reflected by this morning’s durables report, is still mixed but looking better.

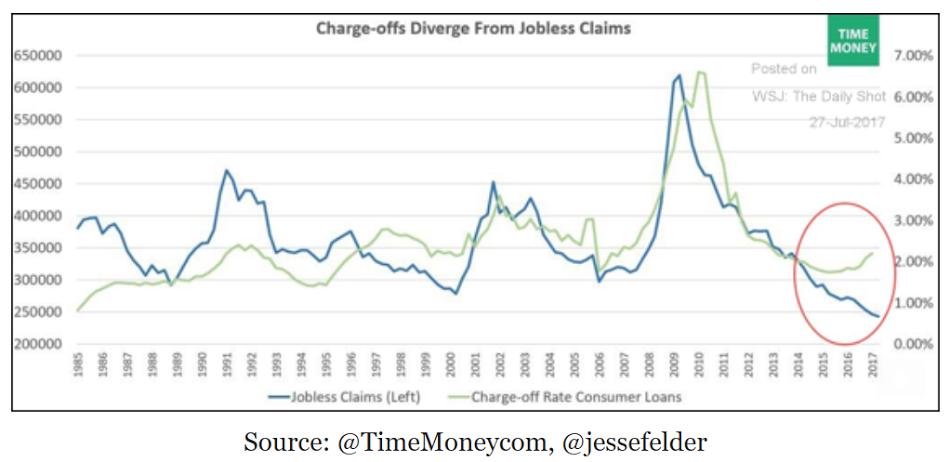

Weaker lending here as well as the US:

Euro zone corporate lending slows from post-crisis high

By Jason Lange and Lindsay Dunsmuir

Jul 26 (Reuters) — Corporate lending in the 19-country currency bloc grew by 2.1 percent in June, a big slowdown from the previous month’s 2.5 percent when growth was at its best pace since 2009. “The decline in the annual growth rate of loans to non-financial corporations in June reflects to a significant extent intragroup transactions,” the ECB said about the data. Lending to households meanwhile grew by 2.6 percent in June, unchanged from the previous month when it hit its highest pace since March 2009. The annual growth rate of the M3 measure of money circulating in the euro zone rose to 5.0 percent last month from 4.9 percent in May.