High powered money in Greece. The EU is re-financing 8,5 billion of Greek debt. About 7 billion of this is just trading in one kind of government bonds for another kind of government bonds. Much ado about less than nothing. There is some welcome softening of the terms – but not enough. However: About 1,6 billion has to be used to pay overdue bills which have to be paid by the government. This exchanging private debt for government bonds and will lead to an injection of highly powered money into the Greek economy which will prevent bankruptcies, which will enable these suppliers to pay their bills to their suppliers. Spain has however already threatened to block the agreement as it wants to protect a corrupt Spanish citizen in charge of privatization in Greece. The ECB doubles down on

Topics:

Merijn T. Knibbe considers the following as important: Uncategorized

This could be interesting, too:

tom writes The Ukraine war and Europe’s deepening march of folly

Stavros Mavroudeas writes CfP of Marxist Macroeconomic Modelling workgroup – 18th WAPE Forum, Istanbul August 6-8, 2025

Lars Pålsson Syll writes The pretence-of-knowledge syndrome

Dean Baker writes Crypto and Donald Trump’s strategic baseball card reserve

High powered money in Greece. The EU is re-financing 8,5 billion of Greek debt. About 7 billion of this is just trading in one kind of government bonds for another kind of government bonds. Much ado about less than nothing. There is some welcome softening of the terms – but not enough. However: About 1,6 billion has to be used to pay overdue bills which have to be paid by the government. This exchanging private debt for government bonds and will lead to an injection of highly powered money into the Greek economy which will prevent bankruptcies, which will enable these suppliers to pay their bills to their suppliers. Spain has however already threatened to block the agreement as it wants to protect a corrupt Spanish citizen in charge of privatization in Greece.

The ECB doubles down on monetary financing of the government. The European Central Bank published a report detailing why banks do or do not get ELA (Emergency Liquidity Assistance). To an extent, this is an answer to questions of Varoufakis and it surely makes the ECB more transparent. And, as ELA was the ultimate lever to discipline Ireland, Cyprus and Greece, it also makes the European Union more transparent (though not more appealing). Alas, the ECB is digging in when it comes to monetary financing of the government and uses the prohibition of ‘monetary financing’ even to enable Outright Money Destruction. It now considers financing of bankrupt banks as monetary financing of the government: “ELA provision to insolvent institutions and institutions for which insolvency proceedings have been initiated according to national laws violates the prohibition of monetary financing.”. For ordinary companies I agree that these, in case of insolvency, should not be financed by central bank money. In this case the above statement however means: “people will lose their deposit money”. Whenever a bank is insolvent, the European system of Central Banks, headed by the ECB, should totally allow everybody to cash all their deposit money, using the ATP. ELA should finance this (of course after stock- and bondholders have been bailed in). This would of course mean an accounting loss for the ECB (so what). But otherwise, households and companies will lose their money – a big deal (another method would be to ensure that every bank already has enough central bank money in a seperate ECB account to do this before they are insolvent)!

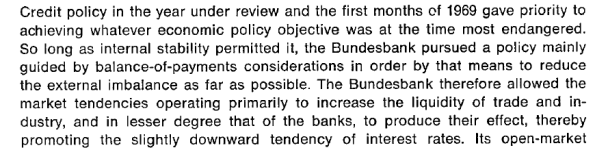

A glimpse from the Golden Age of Applied Macro-Economics. The German ‘Statistisches Bundesamt’ stated that, fifty years ago today, the German Stability Law was enacted. According to this law, the government had a quadruple economic goal:

continuous and adequate economic growth

stable price level

high level of employment

foreign trade equilibrium

Note that the government deficit and government debt is not mentioned. These were not goals but means. Government saving of dissaving was used, together with the exchange rate (the Deutsche Mark was revalued in 1961 and 1969) and the interest rate/credit guidance of the Bundesbank as a tool to stabilize the economy. To give a flavor of this kind of economic policy: in 1968 the current account surplus of Germany increased. The German Bundesbank feverishly tried to get the surplus down. From the 1968 annual report (a screenshot as I could not select text):