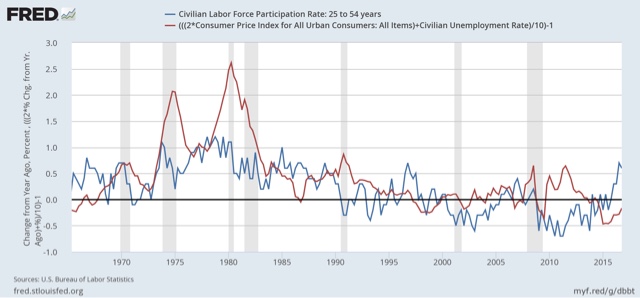

Labor force participation, unemployment, and wages: an update About a year ago I wrote a series of posts on the relationship between the unemployment rate, labor force participation, and wage growth. Especially in view of last Friday’s jobs report, which showed blockbuster hiring, but a continuation of tepid wage growth over 8 years into the expansion, now is a good time for an update. To recapitulate, history shows that wage growth is lags the economy, and specifically only turns after the unemployment rate begins to decline. More specifically, since 1994, once the underemployment rate has fallen below about 9% (red, inverted in the graphs below), wage growth (blue) has begun to improve: Meanwhile, the YoY% change in the prime age labor force

Topics:

NewDealdemocrat considers the following as important: Taxes/regulation, US/Global Economics

This could be interesting, too:

Joel Eissenberg writes How Tesla makes money

Angry Bear writes True pricing: effects on competition

Angry Bear writes The paradox of economic competition

Angry Bear writes USMAC Exempts Certain Items Coming out of Mexico and Canada

Labor force participation, unemployment, and wages: an update

To recapitulate, history shows that wage growth is lags the economy, and specifically only turns after the unemployment rate begins to decline. More specifically, since 1994, once the underemployment rate has fallen below about 9% (red, inverted in the graphs below), wage growth (blue) has begun to improve:

Meanwhile, the YoY% change in the prime age labor force participation rate turns about one year before wages (green):

On the other hand, the absolute *level* of prime age labor force participation only bottoms *after* wages have turned:

Here is the monthly graph through last Friday, whowing that all three metrics have continued to improve:

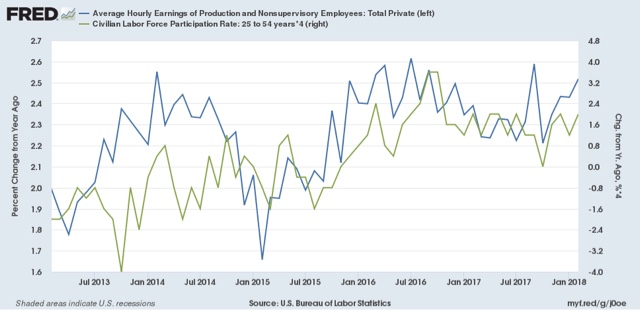

Here is an updated graph of wage growth (blue) and prime age labor force participation (green, right scale) through Friday:

In accord with my hypothesis last year, the continuing surge of participants into the labor force has acted to depress wage growth.

So, in sum, the trends remain positive, but an acceleration of wage growth probably won’t happen until this surge subsides.