HEADLINES: +103,000 jobs added U3 unemployment rate unchanged at 4.1% U6 underemployment rate fell -0.2% from 8.2% to 8.0% Here are the headlines on wages and the chronic heightened underemployment: Wages and participation rates Not in Labor Force, but Want a Job Now: fell -35,000 from 5.131 million to 5.096 million Part time for economic reasons: fell -141,000 from 5.160 million to 5.019 million Employment/population ratio ages 25-54: fell -0.1% from 79.3% to 79.2% Average Weekly Earnings for Production and Nonsupervisory Personnel: rose $.04 from .38 to .42, up +2.4% YoY. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to

Topics:

NewDealdemocrat considers the following as important: Taxes/regulation, US/Global Economics

This could be interesting, too:

Joel Eissenberg writes How Tesla makes money

Angry Bear writes True pricing: effects on competition

Angry Bear writes The paradox of economic competition

Angry Bear writes USMAC Exempts Certain Items Coming out of Mexico and Canada

- +103,000 jobs added

- U3 unemployment rate unchanged at 4.1%

- U6 underemployment rate fell -0.2% from 8.2% to 8.0%

- Not in Labor Force, but Want a Job Now: fell -35,000 from 5.131 million to 5.096 million

- Part time for economic reasons: fell -141,000 from 5.160 million to 5.019 million

- Employment/population ratio ages 25-54: fell -0.1% from 79.3% to 79.2%

- Average Weekly Earnings for Production and Nonsupervisory Personnel: rose $.04 from $22.38 to $22.42, up +2.4% YoY. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to come closer to the situation for ordinary workers.)

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

- Manufacturing jobs rose 22,000 for an average of +19,000/month in the past year vs. the last seven years of Obama’s presidency in which an average of 10,300 manufacturing jobs were added each month.

- Coal mining jobs were unchanged for an average of +75/month vs. the last seven years of Obama’s presidency in which an average of -300 jobs were lost each month

January was revised downward by -63,000. February was revised upward by +13,000, for a net change of -50,000.

- the average manufacturing workweek fell -0.1 hours from 41.0 hours to 40.9 hours. This is one of the 10 components of the LEI.

- construction jobs decreased by -15,000. YoY construction jobs are up +228,000.

- temporary jobs decreased by -600.

- the number of people unemployed for 5 weeks or less decreased by -221,000 from 2,508,000 to 2,287,000. The post-recession low was set over two years ago at 2,095,000.

-

- Overtime fell -0.1 hours to 3.6 hours.

- Professional and business employment (generally higher-paying jobs) rose by +33,000 and is up +502,000 YoY.

- the index of aggregate hours worked in the economy fell by -0.2%.

- the index of aggregate payrolls was unchanged.

- the alternate jobs number contained in the more volatile household survey increased by +163,000 jobs. This represents an increase of 2,683,000 jobs YoY vs. 2,261,000 in the establishment survey.

- Government jobs rose by 1,000.

- the overall employment to population ratio for all ages 16 and up was unchanged at 60.4 m/m and is up +0.2% YoY.

- The labor force participation rate fell -0.1% to 62.9 m/m and is down -0.1% YoY

This was a surprisingly weak report. While manufacturing employment continued to gain, and measures of underemployment fell (but not to new lows), most of the indicators fell. Some of these, like aggregate hours, the employment population ratio, and the labor force participation ratio, simply gave back last month’s improvement.

But that three of the four leading indicators, plus revisions, in the report declined is not welcome news (although obviously only one month), and wage growth for ordinary workers remains tepid at 2.4%.

If the jobs boost from last autumn’s spending by consumers is over, then the slow late-cycle deceleration in jobs growth can be expected to resume.

UPDATE:

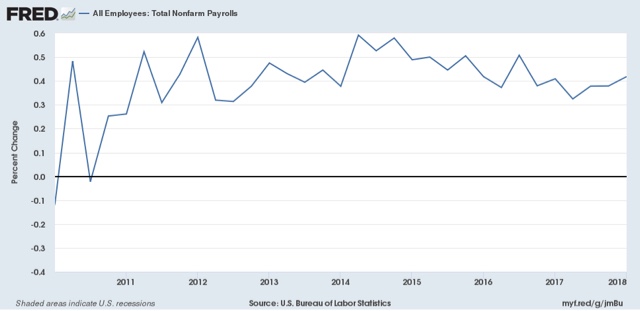

Here is the quarter on quarter growth rate of jobs since the beginning of this expansion:

The last three months together were still the best in the past year. But my suspicion is that we will see a resumption of the downtrend that began in early 2015 going forward.

THURSDAY, APRIL 5, 2018

April reports of short leading indicators start out good