I have written about student loans or have added articles about student loans to Angry Bear here, here, here, here, etc, etc, etc. I go back years on the topic as well as Alan Collinge of Student Loan Justice does. Politicians resist loan forgiveness claiming students are taking advantage of the system. It is a lie and many of the students have interest on loans which surpass the principal. I know of no bank or business loan which has such harsh actions or requirements on loans. The 2005 Act slammed the door shut on the remainder of student loans eligible for relief. Interest rates on loans should be held to 3% or less for all degrees. Student loans should not be a money maker for the government or banks. Both Alex and Algernon are giving

Topics:

Angry Bear considers the following as important: Debt, Education, politics, student loans, US EConomics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

I have written about student loans or have added articles about student loans to Angry Bear here, here, here, here, etc, etc, etc. I go back years on the topic as well as Alan Collinge of Student Loan Justice does.

Politicians resist loan forgiveness claiming students are taking advantage of the system. It is a lie and many of the students have interest on loans which surpass the principal. I know of no bank or business loan which has such harsh actions or requirements on loans. The 2005 Act slammed the door shut on the remainder of student loans eligible for relief. Interest rates on loans should be held to 3% or less for all degrees.

Student loans should not be a money maker for the government or banks.

Both Alex and Algernon are giving an update on what may happen to students holding loans. Here again and the same as Oil, there are people outside of government preparing the Executive Orders, etc. for trump to sign and put into action for Student Loans. It appears the trump collection of followers may not have the qualifications to write such Executive Orders plopped before trump.

It is a good read.

~~~~~~~~

Student Debt Crisis Would Likely Worsen Under a Second Trump Administration

Alex Richwine and Algernon Austin

CEPR

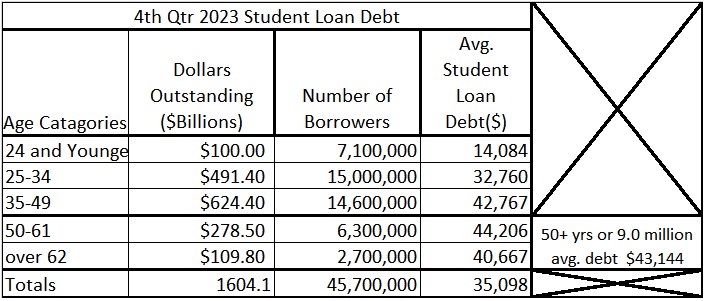

The crisis of student debt has reached proportions never before seen in the United States. Collectively, students owed $1.6 trillion in federal student loans at the end of 2023. However, that total is slightly lower than it was two years prior, thanks to some proactive actions from the Biden administration. The administration has pursued a variety of policies and initiatives to forgive student debt and ease the process of repayment. These policies have halted a decades-long increase in outstanding student debt, but that increase would likely return under a second Trump administration.

Last year, the Heritage Foundation’s Project 2025 released its Mandate for Leadership: The Conservative Promise policy manual. The document provides 900 pages of detailed policy prescriptions for a Republican administration to implement in 2025. The authors include 18 former senior Trump administration staff, scholars from various conservative think tanks, as well as academics with a history of advocating for reduced government involvement. Project 2025 has been endorsed by over 100 prominent conservative organizations. While there is no guarantee that a potential Trump administration would accept the authors’ recommendations, many of the recommendations from the 2016 version of Mandate for Leadership were eventually advanced by the Trump administration.

On student debt relief, the Mandate for Leadership proposals would roll back much of what the Biden administration accomplished for student borrowers and loan-burdened public servants. Indeed, their ideal wish is that “there should be no loan forgiveness.” If the first Trump administration was any indication, a second would work to eliminate the federal tools that could help student borrowers instead of addressing the student debt crisis.

Key Findings

- The Mandate for Leadership recommends an approach to student loans that is profitable to lenders, but more costly to the federal government.

- The authors of the Mandate would like that “there should be no loan forgiveness.”

- The Biden administration attempted to cancel over $400 billion in federal student debt in 2021, but the Supreme Court struck this down last year.

- The Biden administration has found other ways to administer the most student debt forgiveness of any presidential administration.

- The Trump administration demonstrated no interest in easing the burden on student borrowers, and, in fact, supported some policies that harmed student borrowers.

Who is Burdened by Student Debt and Why

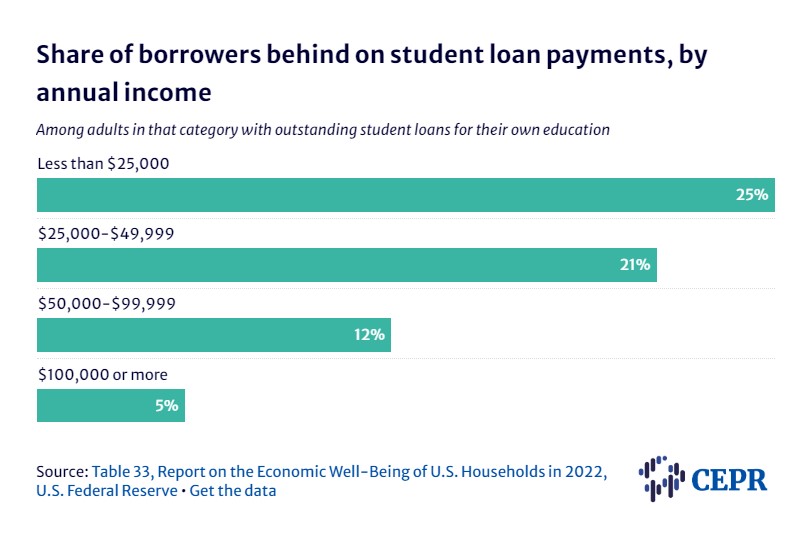

The student debt crisis represents a major obstacle to wealth generation for the middle class. Though the possibility of working your way through school was highly feasible in decades past, the skyrocketing cost of higher education means that those wishing to escape financial insecurity with credentialization must increasingly make use of student loans. Figure 1 shows that lower-income borrowers are more likely to be behind on their student loan payments. Twenty-five percent of borrowers with family incomes below $25,000 are behind on their student loan payments while only 5 percent of borrowers with incomes of $100,000 or more are in the same situation.

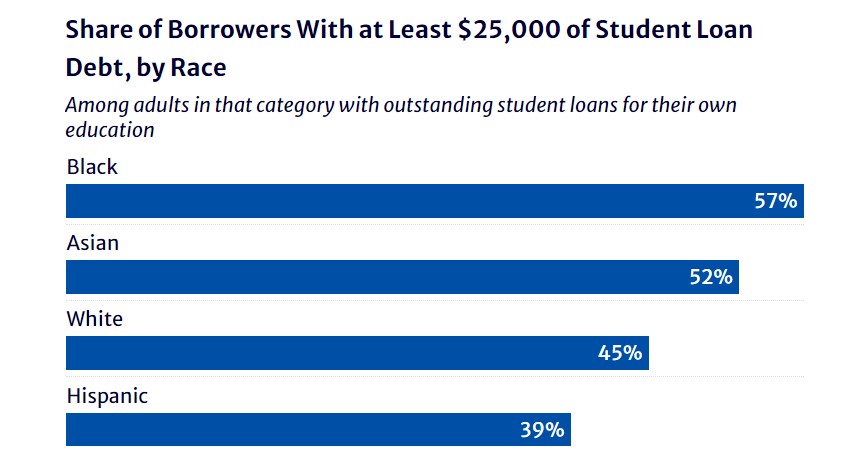

While individuals from all racial backgrounds have student loan debt, Black borrowers, especially Black women, are much more likely to be indebted than other borrowers due to the higher need for accreditation and poorer labor market prospects. Figure 2 shows that 57 percent of Black borrowers had at least $25,000 in student loan debt. Forty-five percent of white borrowers had this range of debt. Student debt relief brings significant benefits to groups facing social and economic disadvantages.

Figure 1

Figure 2

Prior to 2010, the student loan system was a public-private mix that was shown to be more costly than if loans were issued directly by the Department of Education. However, the student loan industry and Republicans in Congress did their best to block or stall the transition to government-issued loans. After the 2008 financial crisis had a chilling effect on private companies’ willingness to issue loans, President Obama was able to sign a bill instructing the Department of Education to issue all federal student loans going forward.

Though the government now serves as a direct lender for federal student loans, it continues to use private companies to assist with Income-Driven Repayment (IDR) administration. These private servicers have a documented record of dysfunctional handling of these loans. Some servicers failed to grant forgiveness to millions of borrowers, despite the fact that they had met the 20-year threshold for forgiveness. This had a particularly negative impact on low-income borrowers. The Biden administration has been working to clean up this mess.

What is in the Mandate

Based on the Mandate for Leadership, we can expect a second Trump administration to mobilize against student loan assistance in a variety of ways.

The authors of the Mandate want little to no role for the government in managing student debt portfolios. Ultimately, they want the private sector to take over completely, but the more feasible proposal is shifting the federal government’s role from direct lender back to guarantor. As mentioned above, while this approach is profitable to lenders, it is more costly to the federal government. The Mandate’s authors wish to “completely reverse the student loan federalization” by gradually eliminating the Office of Federal Student Aid (FSA). Distribution of federal loans would then be a private operation, with a new public corporation acting as the monitor.

The Mandate authors wish to phase out all existing Income-Driven Repayment (IDR) plans and replace them with an IDR that would have more narrow eligibility rules. Ideally, the goal is that “there should be no loan forgiveness.” This would remove the possibility of student loan forgiveness for countless individuals who make consistent payments but have no hope of fully paying off the loan.

The section on education reform also features a recommendation that colleges have “skin in the game,” to enforce accountability for the indebtedness of their students. Essentially, a college would be incentivized to keep costs low if it were required to pay penalties when its students default on student loans. This idea once had bipartisan support on the Hill, but many have come to realize that this would likely have adverse effects on institutions that largely admit students from underserved populations, including HBCUs and community colleges. These schools might reduce their admission of low-income students to avoid penalties, an outcome that would sacrifice educational equity. Alternatively, universities that expect to be paying these penalties — because they continue to prioritize enrolling low-income and minority populations — would increase tuition to account for these expected costs. Neither of these options bodes well for the sustainability of accessible higher education. Furthermore, private colleges already invest in their students by funding financial aid programs from their own resources.

None of these proposals represent a solution to the problem, namely, that economically insecure students must indebt themselves to have a chance at securing good jobs. Though student debt relief is not a panacea for this problem, a reduction of the government’s role in helping student borrowers would certainly worsen the issue.

Biden Administration’s Record on Student Debt Relief

With the potential of a new Trump administration dismantling federal student loan forgiveness, it is worth recounting what the Biden administration has done in this area. The administration attempted to cancel over $400 billion in federal student debt in 2021, but the Supreme Court struck this down last year. The Biden administration has pursued alternative means and has administered the most student debt forgiveness of any presidential administration — roughly $153 billion. The administration canceled student debt for nearly 900,000 public service workers, debt totaling $62.5 billion. The Biden administration has been committed to helping struggling student borrowers.

One of the major avenues through which the Biden administration has administered student debt forgiveness is the “borrower defense to repayment” program. This program allows the President to unilaterally cancel debt for student borrowers who were defrauded, typically by for-profit colleges. While it has been successful in eliminating debt for millions of borrowers so far, recent challenges in the courts may halt further use of this program.

The administration is currently working to promote the SAVE plan, championing it as the “most affordable repayment plan ever.” The program would cap monthly payments for borrowers with undergraduate loans at five percent of discretionary income. The SAVE plan would also forgive both balance and fees for low-balance borrowers after 120 monthly payments.

What the Trump Administration Did for Student Borrowers

The first Trump administration showed no sympathy for indebted student borrowers. The borrower defense to repayment program, which protects defrauded borrowers, was left virtually unused. Certain collection agencies had been dismissed by the Obama administration for not providing adequate information to debtors about student loan balances. Within 100 days of Trump’s 2017 swearing-in, the Department of Education reinstated contracts with two of those private collection agencies.

Efforts to increase barriers to student debt forgiveness made up a common thread of the Trump administration’s student debt policy. Former Secretary of Education Betsy DeVos made it more difficult for borrowers to pursue forgiveness through the borrower defense to repayment program. In May 2020, Trump vetoed a bipartisan bill to undo that move by DeVos. DeVos was also sued by student borrowers in 2020 for illegally garnishing the wages of borrowers despite a pandemic pause on the practice. Trump’s presidential budgets in 2017 and 2019 called for an elimination of public service debt forgiveness. The administration showed no interest in easing the burden on student borrowers.

Conclusion

The student debt crisis looms large in the political landscape, and for good reason. The crisis affects those who seek economic security but must indebt themselves in the process. While there is a significant need for broader higher-education financing reform, student debt relief is an important approach for improving the financial situation of struggling borrowers who fell victim to an unjust system. The Biden administration has recognized the exigency of this crisis in a way the Trump administration never did. The Mandate for Leadership suggests that a second Trump administration would not pursue student debt forgiveness, allowing the crisis to worsen at the expense of so many struggling Americans.