We have been needing more people, people of some importance, to say something about the economy besides how bad it is. Mind you, no matter how good the recovery is; the negatives will still flow from the other side of the room. If you have been reading New Deal democrat’s commentary at Angry Bear each day, you already have a pretty good idea of where we will land. NDd: “Real retails sales stopped deteriorating YoY last spring, and have been more or less flat YoY since summer. This tells us that the unemployment rate should stop deteriorating as well over the next few months.” “Scenes from the jobs report 2: unemployment rate and consumption: weak, but not recessionary,” Angry Bear , NDd. Coming up? Economist Krugman talks politics as related

Topics:

Bill Haskell considers the following as important: Hot Topics, paul krugman, politics, US EConomics

This could be interesting, too:

Robert Skidelsky writes Lord Skidelsky to ask His Majesty’s Government what is their policy with regard to the Ukraine war following the new policy of the government of the United States of America.

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Ken Melvin writes A Developed Taste

We have been needing more people, people of some importance, to say something about the economy besides how bad it is. Mind you, no matter how good the recovery is; the negatives will still flow from the other side of the room. If you have been reading New Deal democrat’s commentary at Angry Bear each day, you already have a pretty good idea of where we will land.

NDd: “Real retails sales stopped deteriorating YoY last spring, and have been more or less flat YoY since summer. This tells us that the unemployment rate should stop deteriorating as well over the next few months.”

“Scenes from the jobs report 2: unemployment rate and consumption: weak, but not recessionary,” Angry Bear , NDd.

Coming up? Economist Krugman talks politics as related to the economy.

Since we have been in Arizona, what we are experiencing is the lowest gasoline prices yet. Now that means little to me. To those who drive the 4-wheel drive pickups and the overpowered gas-guzzlers, this is a big deal. never ending supply of energy producing gasoline in the low 3-dollar range as compared to the mid to upper 4s not that long ago.

Still not happy. They prefer the orange faced one who handed the economy a $2 trillion deficit with the 2017 tax break. But, but, Biden . . .

Read Krugman’s take.

~~~~~~~~

“Is poor economic sentiment all about MAGA?” NYT, Paul Krugman.

The economy is good, but Americans feel bad about it. Or do they?

The more I look into it, the more I’m convinced that much of what looks like poor public perception about the economy is actually just Republicans angry that Donald Trump isn’t still president.

Last year was a very good one for the U.S. economy. Job growth was strong, unemployment remained near a 50-year low and inflation plunged. Some reports I’ve seen suggest that this favorable combination was somehow paradoxical and contrary to economic theory. In fact, however, it’s exactly what textbook economics says to expect in an economy experiencing an improvement in its productive capacity. And I do mean textbook economics. Here’s a figure from one of the leading introductory economics textbooks — OK, Krugman and Wells, seventh edition (forthcoming) — on the effects of adverse and favorable “supply shocks”:

See here

Setting aside the added details that you can read about there, you can clearly see that the right panel, showing the effects of a positive supply shock, exactly matches what happened in 2023: strong growth combined with falling inflation.

Furthermore, the source of the positive supply shock is obvious: The economy finally got past the disruptions caused by the Covid-19 pandemic. Working out those disruptions took longer than almost anyone expected, then happened faster than almost anyone expected, but there’s no great mystery here. If some prominent economists denied that such a thing was possible, well, that’s their problem.

What is a mystery is why the improving economy hasn’t been reflected in public perceptions. There have been some fairly elaborate analyses of the divergence between economic fundamentals and consumer sentiment, but here’s a simple version:

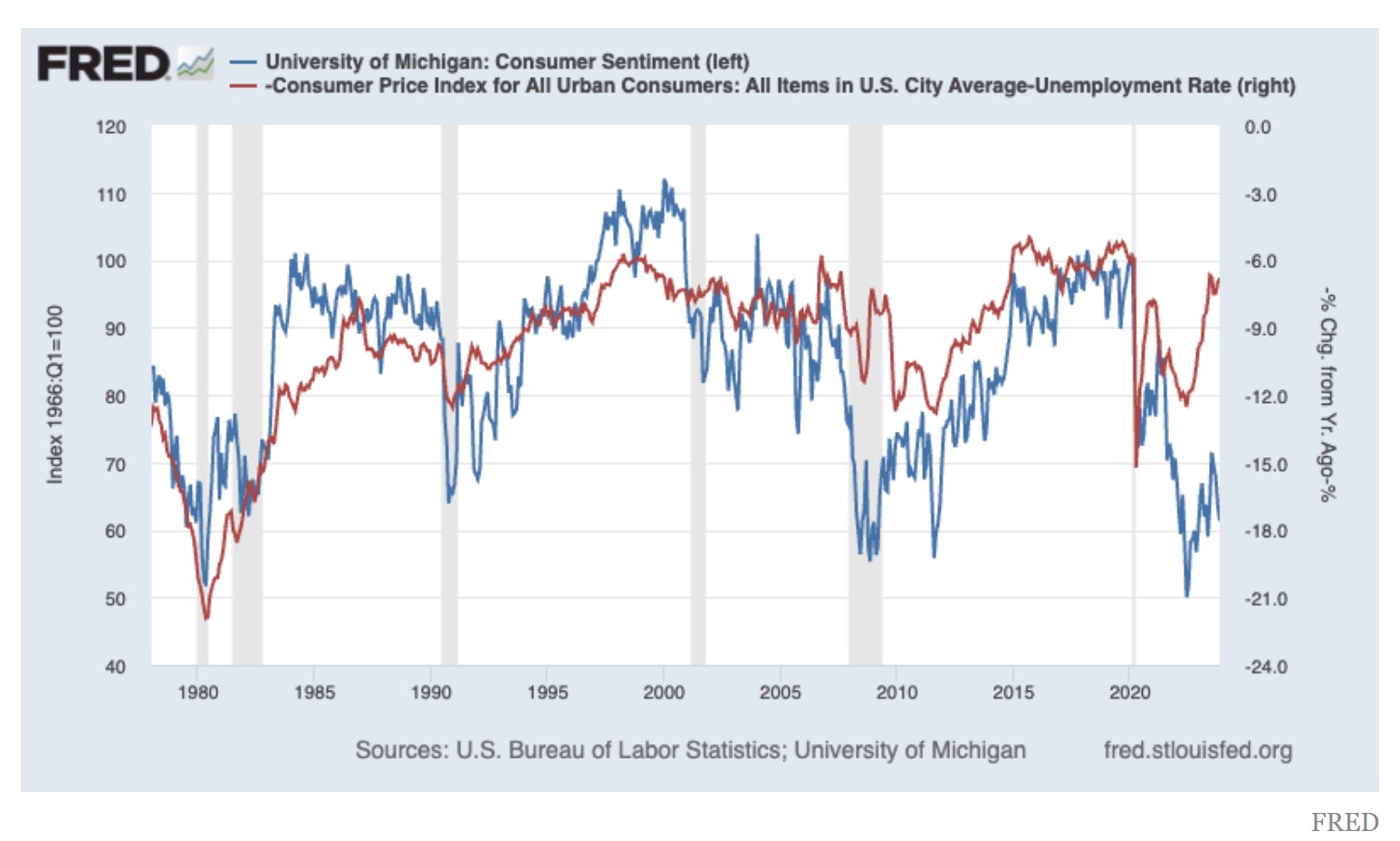

The blue line is the economic sentiment index that has been produced for decades by the University of Michigan. The red line is the “misery index,” the sum of the unemployment rate and the inflation rate, inverted so that up means improved conditions. Until a few years ago, these two measures generally moved together. But despite an uptick in the most recent numbers (not shown), consumer sentiment remains at levels that in the past were associated with severe recessions, very high inflation or both.

As I and many others have pointed out, consumers’ behavior doesn’t match the grim answers they give pollsters: Actual consumer spending remains strong. Still, where is that negative assessment coming from?

Now, Michigan isn’t the only game in town. Another long-running survey, from the Conference Board, paints a more favorable picture, especially for perceptions of the present situation as opposed to expectations. And there’s a newer, internet-based survey, from Civiqs; I am by no means an expert on economic surveys, but Civiqs seems to be using fairly sophisticated methodology.

And their results on economic views by political affiliation look broadly in line with those found by Michigan for “current economic conditions.” The difference is that the Michigan numbers, which are based on a small sample, are very noisy, while Civiqs uses a bigger sample plus statistical wizardry to produce “smoothly trending estimates.” I wouldn’t bet my life on the Civiqs estimates, but in what follows I’m going to use them to suggest that one of the factors everyone knows is affecting consumer sentiment — partisanship — may be even more important than most economists realize. Indeed, weak consumer sentiment may be almost entirely about MAGA.

It has been obvious for a while that views of the economy have become increasingly partisan. It’s also clear that this partisanship is asymmetric: Republicans are much more likely than Democrats to say that the economy is good when their party holds the White House and bad when it doesn’t.

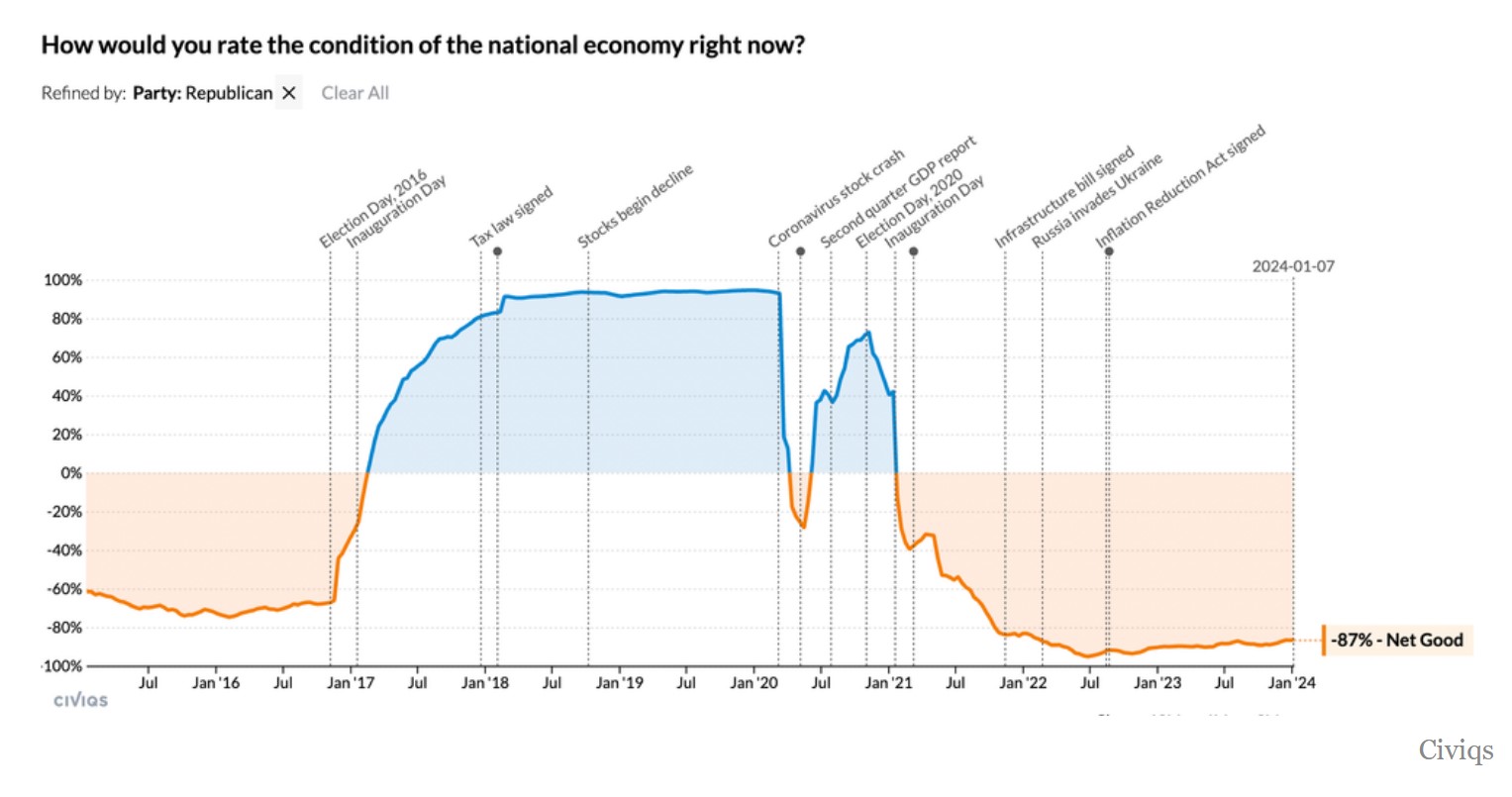

But the Civiqs charts show this asymmetric partisanship especially clearly. Here are their results for self-identified Republicans:

Republican assessments of the economy soared when Donald Trump took office. Even during the pandemic recession, when unemployment rose to almost 15 percent, Republicans had a more favorable view of the economy than they did in the Obama years. And when Joe Biden came in, almost all Republicans declared that the economy was bad — a view that has barely budged in the face of good macroeconomic news.

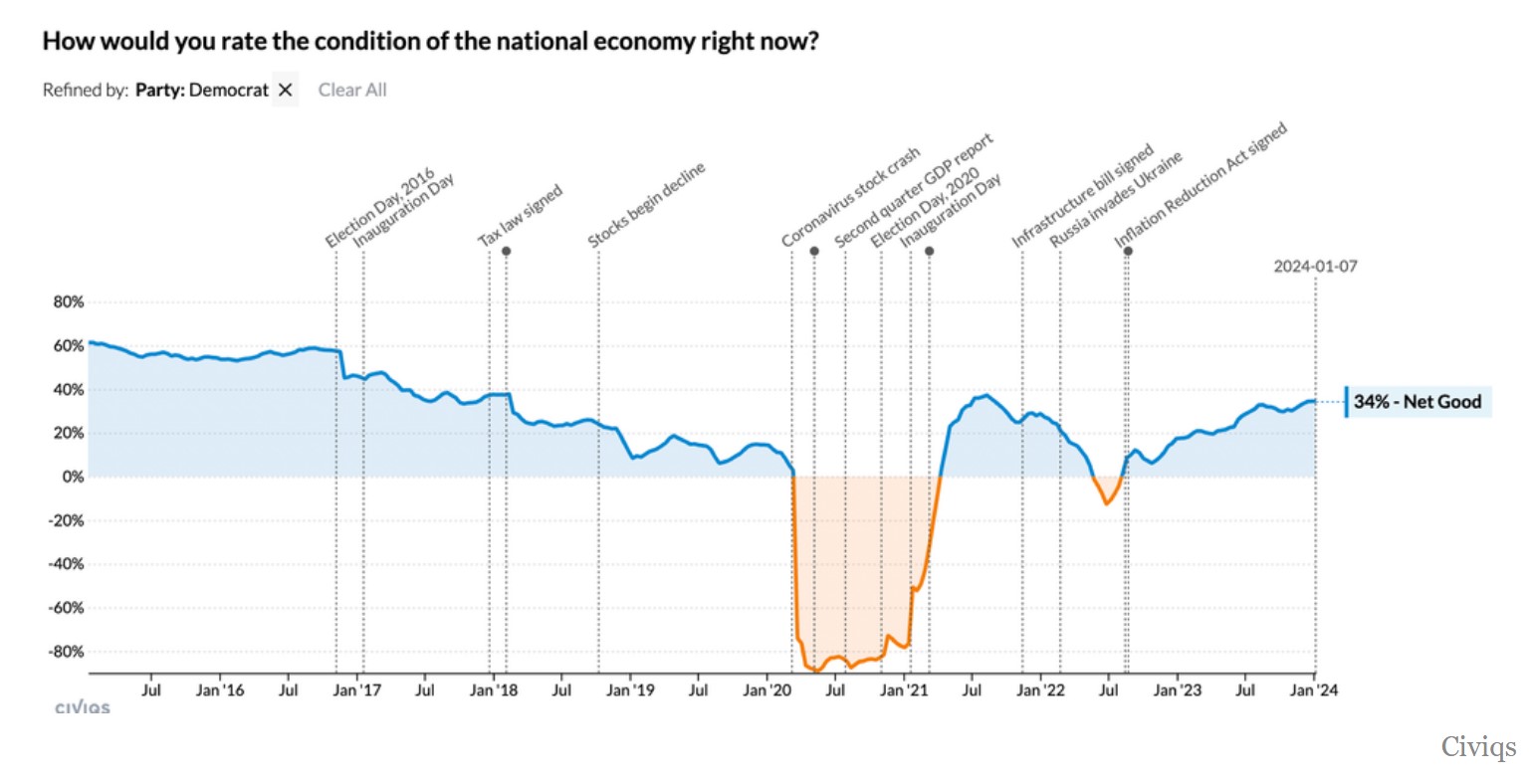

Democrats are not Republicans’ mirror image. Here’s what the Civiqs numbers look like:

If you squint hard, you might see some decline in Democratic economic optimism around the time of Trump’s election, but it’s small. Democrats did feel better about the economy after Biden won, but the economy actually was improving as we recovered from the Covid shutdown. And Democrats’ economic sentiment thereafter followed economic fundamentals, declining as inflation rose, then improving as inflation came down.

What about independents? Never mind. True independents, voters without partisan leaning, barely exist; data for independents is basically an average of voters who think like Democrats and voters who think like Republicans.

What I find most interesting about Democrats’ numbers is what we don’t see: a clear drag on sentiment from the level of prices. There’s a lot of anecdotal evidence — and innumerable posts on social media — to the effect that Americans are upset about how much things cost rather than the inflation rate over the past year. But that’s not obvious from the Civiqs chart on Democrats, who are roughly as positive about the economy now as they were in Biden’s early months, before the big price increases of 2021-22.

I’m not prepared to completely dismiss the issue of the overall price level, which is backed by academic research as well as anecdotes. But as I said, it’s not obvious in the survey data.

So maybe we should at least entertain the hypothesis that the historically anomalous behavior of consumer sentiment reflects the historically anomalous nature of the modern G.O.P., two-thirds of whose supporters believe — based on no evidence — that the 2020 election was stolen. Maybe economic polling, like everything else with this crowd, is all about MAGA.

If that’s really true, the political implications are somewhat ambiguous. Poor economic sentiment may not weigh on Biden because it’s being driven by people who would never vote for him anyway. On the other hand, this interpretation suggests that most of the political upside of an improving economy may already be baked in, since Democrats have already accepted the good news, while Republicans never will.

In any case, the general point is that you just can’t interpret surveys of economic sentiment, or for that matter anything else, without taking into account the fact that the modern G.O.P. bears no resemblance to the Republican Party of past years, or for that matter any political party in modern U.S. history.