The last published accounts for the NI Fund show that, contrary to popular mythology, it does not have an enormous surplus. In fact it is currently running a deficit, as it has been for the last five years. Its reserves have fallen to the point where the Government was forced to top them up to prevent them falling below the statutory minimum of 1/6 of payments out of the fund. So I was somewhat surprised to read written evidence to the Work and Pensions Select Committee which appeared to contradict the accounts. The evidence comes from Rita Abrahams and references the Social Security Up-Rating Report by the Government Actuary, published in January 2016.Here is how Ms. Abrahams has interpreted the Government Actuary's findings: The latest Actuary report published in January projected that by April 2021 our National Insurance Fund will have a balance of £58 billion; thus after setting aside the working balance requirement of £18.52 billion (1/6th of payments) a surplus would remain of £39.48 billion. The surpluses over the working balance for each of the next 5-years roughly breaks down as follows. 2016-2017: - £ 9.78 billion 2017-2018: - £ 3.85 billion 2018-2019: - £ 5.65 billion 2019-2020: - £ 9.10 billion 2020-2021: - £11.10 billion ....

Topics:

Frances Coppola considers the following as important: national insurance, NHS, pensions, public spending, WASPI

This could be interesting, too:

Nick Falvo writes Homelessness among older persons

Frances Coppola writes We need to talk about the state pension

Frances Coppola writes WASPI Campaign’s legal action is morally wrong

Frances Coppola writes Statistics for state pension age campaigners

Here is how Ms. Abrahams has interpreted the Government Actuary's findings:

The latest Actuary report published in January projected that by April 2021 our National Insurance Fund will have a balance of £58 billion; thus after setting aside the working balance requirement of £18.52 billion (1/6th of payments) a surplus would remain of £39.48 billion.

The surpluses over the working balance for each of the next 5-years roughly breaks down as follows.

2016-2017: - £ 9.78 billion

2017-2018: - £ 3.85 billion

2018-2019: - £ 5.65 billion

2019-2020: - £ 9.10 billion

2020-2021: - £11.10 billion

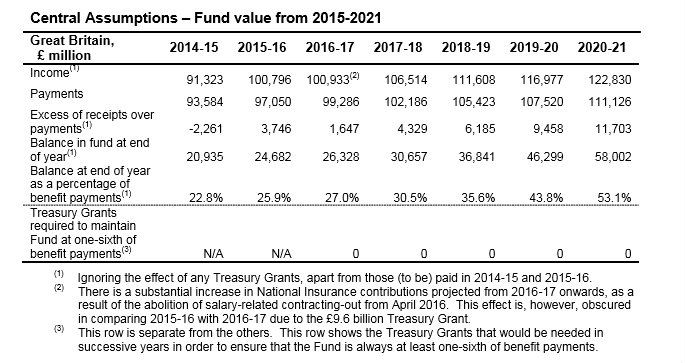

I fear Ms Abrahams has misinterpreted the Government Actuary's findings. She has failed to take into account the components of the baseline forecast for 2015-16, upon which all the later forecasts are built. And she has treated as "firm" a forecast that the Government Actuary says needs to be treated with extreme caution - and is already out of date.....Therefore, contrary to belief there would be no requirement to increase general taxes going forward or use funds that have been set aside for other projects since that £39 billion is a totally unexpected surplus as in January 2015 the Actuary projected a fund value at April 2020 of only £10.2bn, so not even enough to cover the working balance: the Actuary's latest projection for April 2020 stands at £46.299 bn.

Firstly, about that baseline. The Government Actuary has uprated the closing forecast balance for 2015-16, from £11.531bn in the 2015 published accounts to £24.682bn. This enormous rise is explained by four factors:

Of these, by far the most significant is the Treasury Grant. The Government Actuary's central forecast - upon which Ms Abrahams has based her evidence - is as follows:The relative improvement in Fund level in comparison with last year is mainly due to a combination of more optimistic economic assumptions, payment of Treasury Grant, a downward revision in contributory ESA and updates to contribution modelling using more recent information sources

We already know, from the 2015 accounts, that the NI Fund received a grant from general taxation of £4.6bn in 2014-15. Footnote 2 indicates that a further grant of £9.6bn will be paid in 2015-16. The central forecast assumes firstly that this second grant is paid in full, and secondly that neither grant is ever paid back. In other words, the projected £24.682bn surplus in 2015-16 includes a subsidy from general taxation of £14.2bn. Taking that out leaves the NI Fund reserve balance well below its statutory minimum. And since the reserve balance is cumulative, taking out the Treasury grants would also reduce the projected balance for April 2020 to £43.8bn.

It is also worth noting the large rise in NI contributions due to the ending of contracting-out from April 2016, and the fall in payments due to reduced ESA benefits. Both of these are already causing a storm of protest from those affected. The ending of contracting-out will eventually be offset by increased payments under the flat-rate pension scheme, though this is cold comfort to those facing large rises in their NI contributions. But it is not at all clear why the projected surplus should be used exclusively to provide would-be pensioners with relief from cuts to their entitlements. There would surely be a strong case for giving higher priority to restoring the ESA cuts.

That is, if there is a surplus. Forecasts of revenues into and payments from the NI fund are extremely sensitive to economic conditions. Because of this, the Government Actuary has given several forecasts. However, Ms. Abrahams has relied only on the Actuary's central forecast, and as already noted, she has treated it as "firm". But we already know the central forecast is over-optimistic, since it was based upon the OBR's economic forecasts from November 2015, which were downgraded in March 2016.

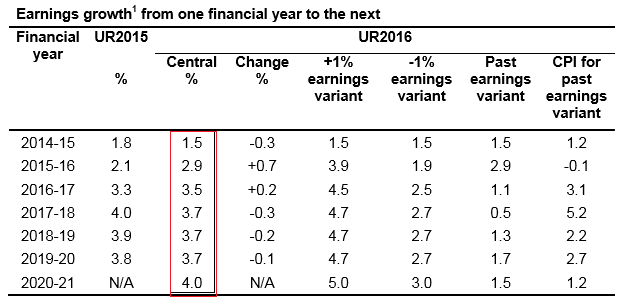

NI Fund receipts come from NI contributions, which are determined by earnings levels. Here are the Government Actuary's earnings growth assumptions for the next five years, with those underpinning the central forecast outlined in red:

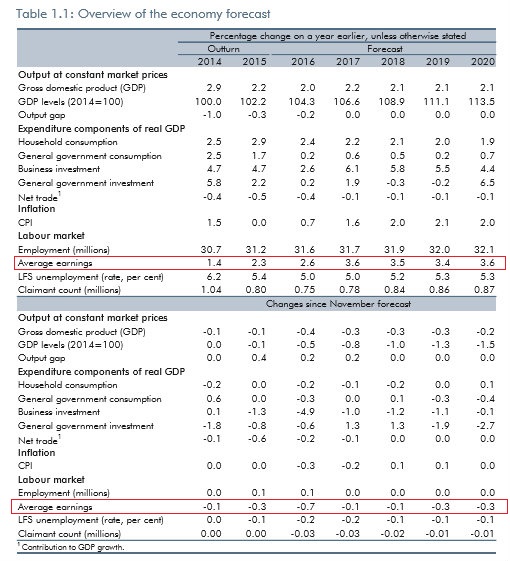

And here is OBR's March 2016 economic forecast with earnings growth assumptions also outlined in red, along with the change in those assumptions since November 2015:

As the OBR's revised estimates for earnings growth are substantially lower than those used by the Government Actuary, and no significant improvement in employment is forecast, the central forecast for NI Fund reserve balance in 2020 must also be downgraded absent a significant ADDITIONAL fall in payments.

On present projections, the NI Fund surplus for 2020 will come in somewhere between the Government Actuary's central and -1% forecasts. This is the -1% forecast:

So we could perhaps assume that the 2020 reserve balance will be somewhere in the region of £45bn. Should this projected balance be spent in advance of receipt to enable certain groups of people to receive state pension earlier than their current legislated state pension age? The NI fund cannot borrow on its own account, so this would mean the Treasury making additional grants funded by government borrowing. Is this a good idea?

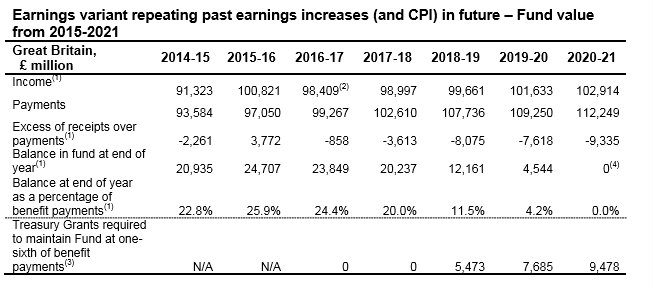

In my view, emphatically no. It is always a bad idea to spend unrealised gains. They can evaporate like the morning mist, leaving you substantially out of pocket. If average earnings do not increase as forecast - and even the downgraded forecasts make pretty heroic assumptions, particularly towards the latter end of the five-year period - then the NI Fund will not recover. Here is the Government Actuary's gloomy prognostication for the NI Fund's finances if earnings growth and CPI remain as stagnant as they have for the last few years:

Far from having surplus funds, the Fund's reserves would be entirely exhausted by 2020, and it would be dependent on rising Treasury subsidies to keep its working balance above the statutory minimum. So under the "no change" economic scenario, the Fund will be effectively insolvent in five years' time even with the planned NIC increases, SPA rises and benefit cuts. Remember that in this scenario, the Actuary has not assumed an economic downturn, only stagnation. The OBR's outside forecasts are even worse.*

So Ms. Abraham's analysis assumes that the NI Fund is considerably more robust than is in fact the case. But I think she knows this, really, since the rest of the piece is all about other ways of increasing the NI Fund surplus. And she thinks she has found a good one.

Currently, the NI Fund partly funds the NHS. In 2003, NI contributions were raised by 1%, and all of that increase went to the NHS. Ms Abrahams argues that the increase should have been distributed more equitably between NHS funding and contributory benefits:

When looking at the years prior to and after the 1% increase in 2003 one can see a dramatic boost that almost doubled the amount of our NICs that was directly transferred by HMRC into the NHS account. NHS allocation funded from NICs between 2001-2015:

2001-2002 - £7.8 billion

2002-2003 - £8.0 billion

2003-2004 - £14.9 billion

2004-2005 - £16.8 billion

2005-2006 - £18.4 billion

2006-2007 - £18.9 billion

2007-2008 - £21.0 billion

2008-2009 - £20.7 billion

2009-2010 - £20.3 billion

2010-2011 - £20.4 billion

2011-2012 - £20.6 billion

2012-2013 - £20.5 billion

2013-2014 - £20.8 billion

2014-2015 - £21.5 billion

If the 1% increase in our NICs had instead been shared out in the same proportions, as before, then between 2003 and 2015 our NIF account would now have a surplus of over £100 billion more than the working balance.

But Ms. Abrahams has ignored the other side of the cash flow statement. The 1% increase can in no way be said to have gone entirely to the NHS. On the contrary, receipts into the Fund substantially exceeded payments out, including the NHS funding, for some years after 2003. By 2009/10, the Fund's reserves had risen to over £50bn:Unfortunately, it seems that the Government at the time decided that our NIF did not required extra funding; maybe it’s time to reverse that decision and share out our NICs in the same ratio as it was prior to the 2003 change.

On this basis alone, there seems little justification for Ms. Abrahams' assertion that the NHS share of the NI Fund payments should be reduced. The present deficit is not due to NHS costs, but the rising cost of pensions.

However, it is true that NHS funding takes a higher proportion of the NI Fund than it used to. Ms. Abrahams likes the idea of reverting to the pre-2002 percentages:

But simply reducing the share of NI Fund payments going to the NHS is silly. Why not transfer all NHS funding to general taxation and be done with it? Ms. Abrahams likes this idea too. It would create an even bigger NI Fund:Currently around 20% of NICs is transferred into the NHS fund with 80% into our NIF, if in 2020 we revert to the 2002 percentages so with around 12% going into the NHS fund and 88% into our NIF then that would give our State Pension Scheme an extra uplift in just that one year alone of around £12 billion.

And funding the NHS entirely from general taxation would resolve an anomaly:And if the Government ran it more like a company pension scheme so all NI contributions went into our NIF and none to the NHS then that would result in an extra uplift that year of around £30 billion and when added to the expected balance at the end of that year of £58 billion, that’s a massive pot of £88 billion and some £70 billion over the working balance.

Very true. It's a sensible suggestion.Admittedly that would mean less being transferred from our NICs to our NHS and therefore that shortfall would need to be made up from our general taxes but that would be more appropriate as all taxpayers would be contributing into this and not just working people under the state pension age who are the only ones who pay NICs.

But then her maths goes badly astray. She rightly says that removing NHS funding from the NI Fund would enable employer and employee NICs to be reduced. But this isn't remotely compatible with her idea of paying out the NI Fund surplus to everyone who had less than 10 years' notice of a state pension age rise:

That is a LOT of people. Far more than those ever envisaged by the WASPI campaign. It is clear that if all these people are to be excused the state pension age rises currently planned, NICs could not possibly reduce as Ms Abrahams suggests. Indeed, they might even have to rise. This would be in addition to increases in other taxes to fund the NHS spending moved to general taxation.Who should be eligible and why? All who’ve not received 10-years notice of a change to their SPA, so including both men and women, thus men 55 or older who’s not received notification should still be allowed to take their State Pension at 65 and women 50 or older who’s not received notification should still be allowed to take their State Pension at 60.

Under Ms. Abrahams' plan, the overall tax bill for working people (of any age) would rise - possibly substantially. The principal beneficiaries would be those who currently are not eligible for state pensions due to SPA rises.

So Ms Abrahams' proposal amounts to a disguised demand for rollback of the 1995 and 2011 Pensions Acts, funded by significantly higher taxes for working people and dependent on some highly optimistic actuarial forecasts. It should be rejected.

Related reading:

The Fund that isn't a fund

Research briefing: National Insurance Fund 1975-2014

OBR Economic and Fiscal Outlook, March 2016

* Really, this is telling us that unless the UK economy performs a lot better than it has in recent years, the Triple Lock is unaffordable. But that's a story for another day.