Last week saw two high-profile corporate failures in the UK. Toys R Us finally went into administration after a stay of execution over Christmas. And private equity firm Rutland Partners pulled the plug on geeky electronics retailer Maplin. Total job losses from both failures amount to something in the region of 5,000 across the whole of the UK. No-one was particularly surprised by the failure of Toys R Us. The company had proved slow to respond to the rise of online shopping and the trend away from large out-of-town retail outlets in favour of small local shops. In the US, Toys R Us filed for Chapter 11 bankruptcy protection (the American equivalent of administration) in September 2017. Despite the American company's insistence that its European operations were not affected, it was

Topics:

Frances Coppola considers the following as important: Debt, insolvency, loss, profit

This could be interesting, too:

Robert Skidelsky writes Britain’s Illusory Fiscal Black Hole

Michael Hudson writes Gold as the Peace Currency

Angry Bear writes The Rising Burden of Government Debt

Angry Bear writes US Debt, Problems, and Fixes

Last week saw two high-profile corporate failures in the UK. Toys R Us finally went into administration after a stay of execution over Christmas. And private equity firm Rutland Partners pulled the plug on geeky electronics retailer Maplin. Total job losses from both failures amount to something in the region of 5,000 across the whole of the UK.

No-one was particularly surprised by the failure of Toys R Us. The company had proved slow to respond to the rise of online shopping and the trend away from large out-of-town retail outlets in favour of small local shops. In the US, Toys R Us filed for Chapter 11 bankruptcy protection (the American equivalent of administration) in September 2017. Despite the American company's insistence that its European operations were not affected, it was almost inevitable that the UK subsidiary would eventually follow suit. British consumers are shifting to online shopping every bit as rapidly as consumers across the Pond, and the trend towards localism is evident in the UK with the growth of convenience stores. Toys R Us, with its big out-of-town stores, poor online offering and lack of high street presence, looked increasingly anachronistic.

But the second failure came as something of a shock. Only a few days before, Maplin had blithely announced the opening of a new store. What went wrong?

The company that has been placed into administration is MEL Topco, which is the top layer of a complex corporate structure created by Rutland Partners in 2014 when Rutland purchased Maplin Electronics Group (Holdings) Ltd. from its previous owner Montagu Private Capital. Maplin Electronics Group (Holdings) Ltd. still exists, however; its 2017 accounts say that it is a "non-trading intermediary holding company". Its sole owner is MEL Bidco. MEL Bidco is a wholly-owned subsidiary of MEL Midco, which in turn is a wholly-owned subsidiary of MEL Topco. The corporate structure below Maplin Electronics Group (Holdings) is similarly complex. Maplin Electronics Group (Holdings) Ltd. is the sole owner of Maplin Electronics (Holdings) Ltd., which in turn is the sole owner of Maplin Electronics Ltd., the actual retailer. So the retailer has no less than six holding companies above it. It also has a wholly-owned subsidiary of its own, Maplin Electronics HK Ltd.

MEL Midco's 2017 accounts were created on a "going concern" basis even though it has no income and a balance sheet consisting entirely of debt. Apparently this is ok because its shareholder, MEL Topco guarantees its solvency. Similarly, MEL Bidco's accounts were also done on a "going concern" basis despite having £83m of net current liabilities. Apparently MEL Topco guarantees those, too. So MEL Midco and Bidco are now insolvent, because MEL Topco cannot honour those guarantees.

Further down the corporate structure, Maplin Electronics Group (Holdings) Ltd. mainly seems to exist to drain Maplin Electronics Ltd. of profits. On the books of Maplin Electronics Group (Holdings) Ltd. is an intercompany loan to Maplin Electronics Ltd. at an interest rate of 10%. The interest charge on this loan was sufficient to ensure that Maplin Electronics Ltd. made a statutory loss in both 2016 and 2017. Meanwhile, the direct owner of Maplin Electronics Ltd, Maplin Electronics (Holdings) Ltd., appears to exist only as a vehicle to hold a £31m revolving credit facility from Lloyds Bank. All of these intermediate companies are effectively guaranteed by MEL TopCo. All of them are now therefore insolvent.

Interestingly, the lower half of the structure pre-dates Rutland's acquisition. It was created by Maplin's previous owner, Montagu Capital, when it acquired Maplin in 2004. So it seems Rutland simply added its own layers on top of the existing structure.

Quite why Rutland has created such a complex corporate structure for Maplin is not immediately apparent, but I suspect it may have something to do with tax, or rather avoiding it. The accounts of the holding companies reveal complex and opaque inter-company loans and transfers which are otherwise hard to explain. I'd like a tax accountant to have a good look at those intercompany transfers.*

However, the complexities of Maplin's structure post-Rutland are not my concern. I'm chasing a different hare.

When Rutland Partners acquired Maplin in 2014 it funded the purchase with debt. That debt was loaded in its entirety on to the books of MEL Topco, in the form of £15m of bank loans at Libor + 7.5% and £72m of shareholders' loan notes at 15%. The 2017 full-year accounts show that MEL Topco generated an operating profit. This turned into a statutory loss after goodwill amortisation and interest charges. Richard Murphy, in his brief analysis of MEL Topco's 2017 accounts, says that it was the high interest charges on the shareholders' loans and accrued interest that rendered MEL Topco insolvent.

It is fair to say that the shareholders' loans were significantly more expensive than the bank loans. But that does not necessarily mean that the interest rate was exorbitant. Shareholders' loans are deeply subordinated debt instruments with equity-like characteristics. Really, they are equity dressed up as debt to take advantage of the "tax shield" on debt. So that 15% interest rate can be regarded as equivalent to the after-tax return that Rutland Partners, as shareholder, expected to receive from its acquisition. Was that an unreasonable expectation?

For a long-term acquisition of a sound company with stable cash flow, 15% would be a fairly high return, though not exceptional - many shareholders would expect a return on equity of the order of 12-15%. On the face of it, therefore, an interest rate of 15% on shareholders' loans doesn't look exorbitant.

But a sound company can finance itself with senior debt, so would pay a lower interest rate. By using the interest rate on Maplin's bank loans as a benchmark, Richard Murphy effectively assumes that Maplin was a sound company. If he is right, then Rutland's high interest rates are extortionate

But I'm afraid he is wrong. The hard truth is that Maplin not only is insolvent now, but was when Rutland Partners bought it. In fact it has been insolvent for a very long time. It is a zombie company.

The story of how it became a zombie is interesting, and ultimately, very sad. It is a story of a family business that was too successful for its own good.

Maplin was originally created in 1972 by two geeks who were frustrated by the difficulty they had obtaining components for their home electronics. They started up a mail order business from their attic room, producing a catalogue of electronic components from which fellow geeks could order. The business quickly expanded beyond simple mail order, though: Companies House tells us that Maplin Electronics Ltd. was incorporated in 1976, when its owners opened their first retail electronics store. Originally, it was called Maplin Electronic Supplies Ltd, but in 1988, the name was changed to Maplin Electronics Ltd.

Maplin's first audited accounts, in 1982, reveal a fast-growing small company, still owned by its founders. Its turnover had risen from £2m to £3m in one year, it was generating substantial profits and had just made its first acquisition, a company called Mapsoft. It was a little slow paying its bills - trade creditors were high - which suggests it had cash flow problems. The normal response to this would be to obtain working capital finance. But Maplin went much further than simply easing its cash flow difficulties. In the 1985 audited accounts, trade creditors were lower, but Maplin's bank overdraft was well over £1m. It appears that Maplin had bought itself new freehold premises and paid for them entirely with short-term finance - hardly the most prudent financial management. In 1987, it mortgaged the property.

Nonetheless, Maplin continued to grow fast, riding the 1980s boom in home computing and electronics. By 1988, it was a solidly profitable company with a sensible mix of short and long-term financing. And it continued to expand. In 1989, it created a National Distribution Centre for its products. Four years later it opened its first overseas office, in Taiwan.

Maplin's final accounts as an independent company were issued in 1994. Later that year, it was acquired by the private equity company Cannon Street Investments plc, later renamed Saltire plc. However, this appears to have been a friendly merger, since Maplin's original owners remained as directors, and additionally became shareholders in Saltire. It certainly wasn't a leveraged buyout. Maplin continued to finance itself sensibly with bank loans and retained earnings, though in 1995 it took a hit to its revaluation reserve when it was forced to write down the value of its substantial property portfolio in the wake of the UK's property market crash.

Maplin's business continued to expand under Saltire's ownership. It made further acquisitions, opened more stores, and expanded overseas, establishing a Hong Kong subsidiary. But as operating profits rose, the company gave increasingly generous dividends to shareholders. In 1998, its dividend policy even turned a respectable operating profit into a loss. The need to keep Saltire happy was distracting attention from longer-term investment.

In 2000, the dividends stopped when Maplin declared a loss due to a major restructuring. Possibly to protect itself from takeover, Maplin took itself private in March 2001. But the sharks were already circling. In June 2001, the private equity firm Graphite Capital - of which Maplin's director Keith Pacey was a director and shareholder - led a leveraged management buyout of the company.

That's when Maplin acquired the first of its current holding companies. Maplin Electronics (Holdings) Ltd. was formed in 2001 as a vehicle for the debt financing of Maplin's acquisition by Graphite. At that time, it was loaded up with nearly £40m of debt, made up of a mixture of bank loans and subordinated loan notes. Balancing this was an enormous goodwill asset that dwarfed the retailer's substantial tangible assets. The 2002 accounts show that a reasonable operating profit was turned into a loss by the interest charges on the debt. Sounds familiar, yes?

No, this wasn't the start of Maplin's zombification. £40m wasn't a huge amount of debt for a fast-growing medium-size company, and the company was without question creditworthy. So by 2004, it was looking a whole lot healthier. It reported a respectable profit and had refinanced the subordinated loan notes with cheaper bank loans. Admittedly, Graphite was draining the company to some extent: the £5m dividend that year was paid by increased borrowing. But at this stage, Maplin was a healthy profitable company. In September 2004, Graphite sold it to Montagu Capital for £244m, six times what it paid for it. Graphite still lists Maplin as one of its most successful corporate acquisitions.

Montagu Capital took the same funding approach as Graphite. It created the second of Maplin's holding companies, Maplin Electronics Group (Holdings) Ltd., and loaded it up with acquisition debt. But because Montagu Capital had paid so much for the company, the amount of debt loaded on to the new holding company was far more. Right from the start, it proved an intolerable burden.

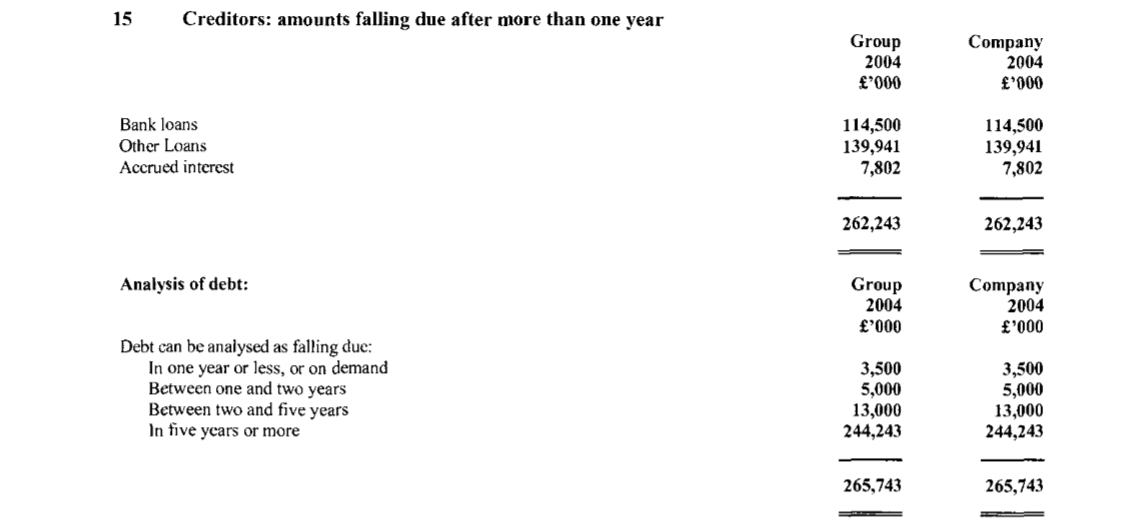

This is the long-term debt of Maplin Electronics Group (Holdings) Ltd. as at January 2005:

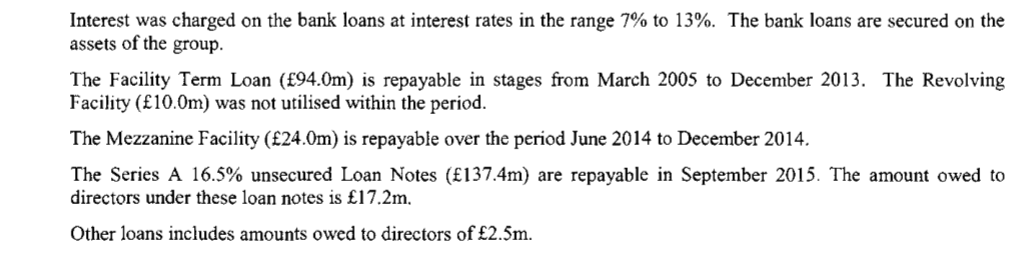

And these are the types of debt, with the interest rates charged:

Not only were the Series A notes extortionate, Maplin was never able to refinance them as it had Graphite's subordinated loan notes. The interest on all that debt, together with amortisation of the balancing goodwill asset, completely swamped Maplin. The January 2005 accounts show that an operating profit of £1.84m was wiped out by £11.74m of interest charges, resulting in a statutory loss of £9.6m. As the holding company didn't have any equity to start with, that loss rendered it insolvent by the same amount.

By December 2005, things were even worse. Operating profits were £16.43m, but goodwill amortisation of £12m and interest charges of £37.24m turned that into a loss of nearly £33m. The shareholders' deficit (the amount by which the company was technically insolvent) grew to £42.4m.

Every year thereafter, Maplin Electronics Group (Holdings) reported a loss. Because interest was being capitalised, the interest charges continually rose, so even though the company's operating profits improved every year until 2011, they were never enough to eliminate the losses. By 2012, the net debt had grown to nearly half a billion pounds, of which £68.9m was accrued interest, and the shareholders' deficit was £320m. Montagu Capital's extortionate charges had turned a healthy growing company into a zombie.

The aftermath of the financial crisis cost Maplin dearly. In 2011, its operating profits slumped as sales growth fell. When the downturn continued into 2012, Montagu realised the game was up. While operating profits were improving, it could pretend that the company would eventually deliver a profit. But now that operating profits were falling, reporting losses year after year while claiming that the company was still a going concern was no longer a sustainable strategy. Trading while insolvent is illegal in the UK. The directors of Maplin were risking disqualification, and Montagu Capital was risking legal action by its customers for failing to take action to recover their money.

In January 2014, Montagu cancelled the accrued interest and injected £542m of new equity into the company. It also impaired the goodwill asset by £85.4m. The goodwill impairment and debt for equity swap weren't enough to return Maplin to solvency, but that wasn't the intention. After all, when your gravy train hits the buffers, you get off it, don't you? So all Montagu aimed to do was make Maplin sufficiently attractive to interest a buyer. It was putting makeup on a corpse.

The buyer that Montagu managed to attract was Rutland Partners, a distressed debt specialist. Rutland paid £89m for Maplin, most of which went to clear Maplin's remaining debt. The first set of accounts for MEL Bidco, the holding company Rutland created as a vehicle for the funding of Maplin's acquisition, say that the real consideration was only £14.7m after debt settlement. But since Maplin was actually insolvent at the time of the acquisition, arguably even this amount was too high. The right price was probably a nominal £1 plus a further cash contribution from Montagu to help settle Maplin's debts. To my mind, Rutland did not drive a hard enough bargain. It must really have wanted Maplin in its portfolio. I wonder if some of its directors are closet geeks.

This brings us to the financing of Rutland's acquisition. In the circumstances, financing with bank loans and/or senior debt, as Richard Murphy suggested, was out of the question. Even financing with bank loans and commercial subordinated debt, as Graphite had done, was impossible. Rutland had to put its own money at risk - or rather, its customers' money. Interest rates are far lower now than they were in 2004, of course. But I find it hard to see that 15% was an exorbitant hurdle rate of return on what was by any standards an extremely risky acquisition.

However, this does not mean that Rutland bears no responsibility for Maplin's failure. Like Montagu, Rutland paid far too much for Maplin. And like Montagu, it funded the overpayment with debt, then loaded that debt onto Maplin's books. Once again, Maplin was loaded with debt it could not service. Had Rutland paid the right amount for Maplin, debt service would not have been so onerous, and Maplin might still be alive today.

Of course, if Rutland had tried to drive a hard bargain, Montagu might have opted to put the company into administration. Indeed, it could have done so anyway. The fact that Montagu sold Maplin to Rutland rather than putting it into administration kept it alive, and its staff in work, for four precious years. The job prospects for its staff now are better than they were four years ago. Perhaps that is something to be grateful for.

The sad story of Maplin Electronics might lead people to damn all private equity investment. Indeed, this is the conclusion that Richard Murphy reaches:

The time has come to question whether the venture capital business model adds value in the UK. The evidence is it may not because it places real business under too much financial stress to survive, let alone prosper.But Maplin was owned by four private equity companies during its long lifespan. And under two of them, it flourished. Only when it was loaded down with debt and systematically drained of profits because its owners had paid far too much for it, did it get into trouble. Perhaps the problem is not so much the venture capital business model itself, but the greed and folly of some of those who make investment decisions.

And there is one final twist in this tale. We don't know exactly why Rutland pulled the plug, but we do know that Maplin's external financiers were getting cold feet. Maplin recently had its trade credit insurance revoked, which for retailers is usually a precursor to failure, whether or not they have a private equity owner. In an interesting article, Computer Weekly argues that Maplin has been unable to respond to the challenge of online sales and has become over-reliant on its stores. So the sad story of Maplin may simply be an old-fashioned tale of over-expansion, loss of core focus and inability to respond to a fast-changing market. Just like Toys R Us.

Corporate insolvencies - or potential insolvencies - are quite a thing at the moment. Here are a few more that have interested me recently.

Clearing out Carillion's cupboards

The misery of Mitie

The Fallout from Carillion's Failure: Could Interserve Be the Next Domino To Fall? - Forbes

After Carillion, Capita's profits warning comes as no surprise - Forbes

* Various people have pointed out that layers of holding companies are often used in PE buyouts because they create structural subordination of various classes of debt. It's entirely possible that this is the reason for Maplin's complex structure.

The original version of this article lacked the final paragraph. The Computer Weekly link was in Related Reading. I have now brought it into the post to tie up with the Toys R Us discussion at the head of the post.