Share the post "What is “Enough”?"I got an email from a college student this morning asking me for financial advice and tips as they near graduation. I always respond to emails like this and try to give people useful advice. But deep down in my heart I know I am mostly just repeating mundane and useless bull shit. You know, work hard, do something you love, etc. But then I sat down and I started thinking about my own situation and I realized that one of the big reasons I am happy is because I figured out what was “enough” for me.About 15 years ago when my career was just getting started I made a big list of all the things I wanted to accomplish.¹ It was basically a list of all the things I would buy when I made gobs of money. Looking back at it, I have a good laugh because I realize that most of the crap on that list is “too much”. Sports cars, McMansions, etc. It was a list of things I want, but don’t need. It was all too much. Luckily, as time went on and I got more successful my needs actually decreased. In other words, my potential liabilities declined even as my assets increased. I not only felt “rich”, but I got happier. A lot happier.I got to thinking about all of this in more detail last week when this post by Financial Samurai went viral in nerdy financial circles.

Topics:

Cullen Roche considers the following as important: Life & Stuff

This could be interesting, too:

Cullen Roche writes I am Not a Dog Person Anymore

Cullen Roche writes 40 Things I’ve Learned in 40 Years

Cullen Roche writes Redemption

Cullen Roche writes My View On: The FIRE Movement

Share the post "What is “Enough”?"

I got an email from a college student this morning asking me for financial advice and tips as they near graduation. I always respond to emails like this and try to give people useful advice. But deep down in my heart I know I am mostly just repeating mundane and useless bull shit. You know, work hard, do something you love, etc. But then I sat down and I started thinking about my own situation and I realized that one of the big reasons I am happy is because I figured out what was “enough” for me.

About 15 years ago when my career was just getting started I made a big list of all the things I wanted to accomplish.¹ It was basically a list of all the things I would buy when I made gobs of money. Looking back at it, I have a good laugh because I realize that most of the crap on that list is “too much”. Sports cars, McMansions, etc. It was a list of things I want, but don’t need. It was all too much. Luckily, as time went on and I got more successful my needs actually decreased. In other words, my potential liabilities declined even as my assets increased. I not only felt “rich”, but I got happier. A lot happier.

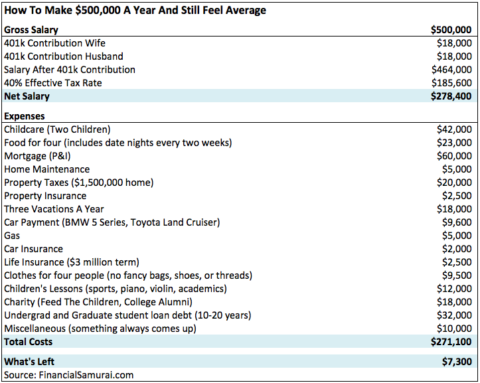

I got to thinking about all of this in more detail last week when this post by Financial Samurai went viral in nerdy financial circles. It’s called “Scraping By On $500,000  A Year: Why It’s So Hard For High Income Earners To Escape The Rat Race”. The chart at the right is a breakdown of a family making $500K “scraping” by.

A Year: Why It’s So Hard For High Income Earners To Escape The Rat Race”. The chart at the right is a breakdown of a family making $500K “scraping” by.

Okay, there’s a few obvious problems here. The 401K is money coming out of one pocket and going into another. So that’s 36K in real savings every year. And I’d argue that the charity and a few other items are totally discretionary. So this family could actually get pretty close to a 12% savings rate. That’s not scraping by at all. But the point remains – most people do scrape by. But why?

Aside from the big obvious macro problems like inequality I suspect the answer is that most people never learn what is enough for them. Making more money can become a revolving door. The more you make the more expensive your tastes get and the higher the expectations become. Mo money doesn’t mean mo problems. Mo money means the same problems mo bigger.

And that’s the kicker here. Financial success is all about managing your asset and liability mismatch. Most people earn a higher and higher income and just increase the proportion of their asset liability mismatch. That is, they make more and they spend more. This is usually a function of their exceedingly high expectations. Expectations that most people never actually achieve. Or, when they achieve them, they realize those expectations aren’t making them happier, but only more burdened.

I consider myself financially successful because I realized what “enough” was. I realized I don’t need fancy cars, huge homes and all the big ticket stuff that drains the bank account fast.² Don’t get me wrong – I like nice stuff, but you won’t ever find me in a $5,000 suit drinking Macallan 25 (although this sounds really nice on second thought). So, you want financial advice young man/woman? Figure out what is enough for you. And as you get older don’t let that “enough” evolve to the point where you’re in the revolving door drowning in work and debt as you try to fund your ever growing asset liability mismatch.

¹ – I would post this list, but that would be super embarrassing and then you’d stop being my friend(s).³

² -Want to learn this lesson fast? Do what I did and buy a boat when you’re young, keep it for a year, then punch yourself in the face for a year and then sell it ASAP.

³ – This footnote assumes there is at least one person reading this and that that person is already my friend.

Share the post "What is “Enough”?"