Here are some things I think I am thinking about. 1. Is the Fed “Playing with Fire”? Stan Druckenmiller had an op-ed in the WSJ about how Fed policy has been too loose for too long. I think there are some reasonable perspectives here. I’ve been pretty vocal about the risk of inflation overshooting the Fed’s target this year. I also think there’s an increasingly convincing argument that the Fed’s policies have contributed to a lot of financial market craziness in the last year. It would not surprise me at all to see the Fed backpedaling later this year or in 2022 as they unwind the balance sheet a bit and raise interest rates to try to contain inflation and the housing market. At the same time, I think this was a risk worth taking. For instance, let’s say the Pandemic had turned out to

Topics:

Cullen Roche considers the following as important: Most Recent Stories

This could be interesting, too:

Cullen Roche writes Understanding the Modern Monetary System – Updated!

Cullen Roche writes We’re Moving!

Cullen Roche writes Has Housing Bottomed?

Cullen Roche writes The Economics of a United States Divorce

Here are some things I think I am thinking about.

1. Is the Fed “Playing with Fire”?

Stan Druckenmiller had an op-ed in the WSJ about how Fed policy has been too loose for too long. I think there are some reasonable perspectives here. I’ve been pretty vocal about the risk of inflation overshooting the Fed’s target this year. I also think there’s an increasingly convincing argument that the Fed’s policies have contributed to a lot of financial market craziness in the last year. It would not surprise me at all to see the Fed backpedaling later this year or in 2022 as they unwind the balance sheet a bit and raise interest rates to try to contain inflation and the housing market.

At the same time, I think this was a risk worth taking. For instance, let’s say the Pandemic had turned out to be much worse than expected. In that case the extra stimulus wouldn’t have been nearly enough. Personally, I think we’re in the clear now and the Fed should be more forward looking, but it was worth dumping gasoline on this fire back in 2020 because the downside risk of no stimulus (a huge deflationary collapse) was far more damaging than the alternative risk from too much stimulus (3-4% inflation).

2. Dollar Reserve Status at Risk? Druck went on CNBC this morning explaining this argument in more detail. He said that the government’s policies endanger the Dollar’s Reserve status. This is a pretty familiar refrain on this website and one that I just think goes too far. I’ve discussed this concept a bunch in the past. Basically, reserve currency status isn’t like a set of car keys. You don’t just up and lose it. Historically, countries lose reserve currency status over hundreds of years. Similarly, reserve currency status is earned over hundreds of years by producing so much output that the rest of the world ends up necessarily needing your financial assets because they’re the assets that are supported by most of the world’s output.

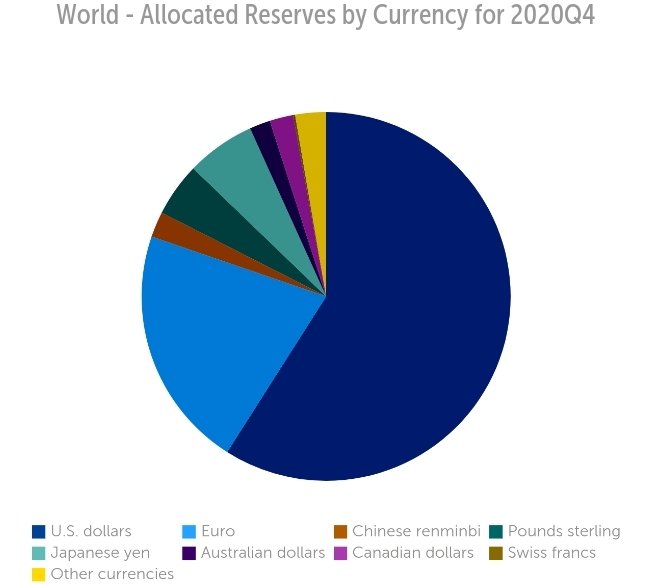

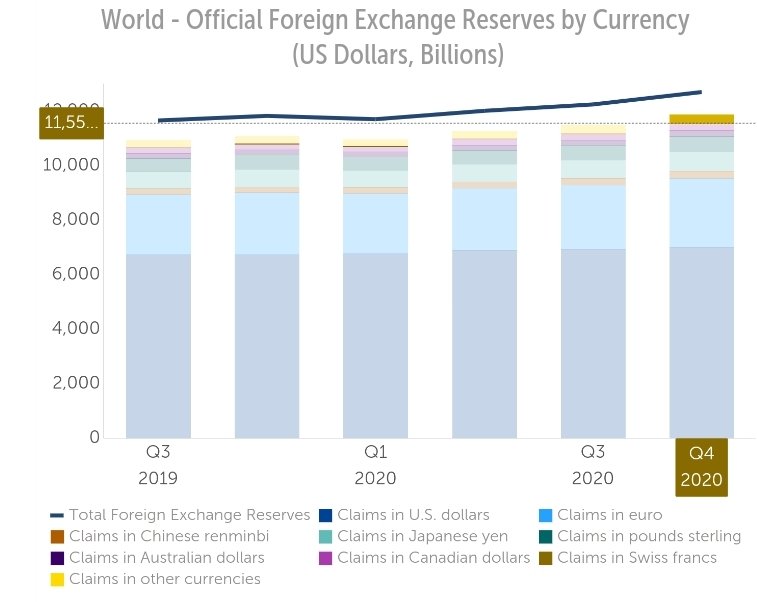

This is clearly still the case in the USA where foreign dollar reserves represent the overwhelming majority of financial reserves.

And this position hasn’t really changed in recent years despite the huge policies from the government:

Will the USA lose reserve status at some point. Yes, absolutely. But it’s likely to be a slow relative process. But for now, it’s pretty hard to imagine what will replace it given the fact that the Euro remains somewhat dysfunctional and the Yuan remains discredited due to the lack of transparency in China….

3. Will Bitcoin Replace the Dollar? Druck also mentioned that Bitcoin or some other cryptocurrency could replace the USD in the coming decades. This is a common argument and one that I also think veers in an extreme.

Basically, I view cryptocurrency as venture capital in some sort of specific blockchain based technology. For instance, in the specific case of Bitcoin I view it as venture capital in a global payment system. That system competes with the USD in certain instances, but it mostly runs parallel to the USD system. It’s kind of like a foreign currency in this sense. For instance, the Euro and USD compete in a certain sense for global reserve currency dominance. The US and European economies make certain quantities of goods/services and the currency’s relative values reflect demand for that currency. But a rising EUR/USD exchange rate does not necessarily mean that the US economy is losing out to Europe in the aggregate. In fact, both economies could be growing strongly and the European economy might just be doing a little better.

It’s the same basic idea as Google and Amazon both growing over time even though Amazon might grow a little faster. The GOOG/AMZN stock exchange rate might change over time, but it’s not a zero sum game at the aggregate level. Same basic point for the global economy. It’s not a zero sum game and Bitcoin or other cryptos could increase in value and provide real value for people in certain ways that the USD does not. And the centralized USD system can continue to add value to the economy in ways that the Bitcoin decentralized system cannot. They’re parallel and complementary systems in many ways, not necessarily competing zero sum assets.

Anyhow, I don’t mean to drag Druckenmiller or make this sound personal. He’s way smarter than I am and I have bigly respect for him, but I think he takes these views a little too far. More importantly, I hope this adds a little bit of extra perspective to topics that many people tend to take too far in my view.

Got Questions/Comments? Go To the Forum for More.