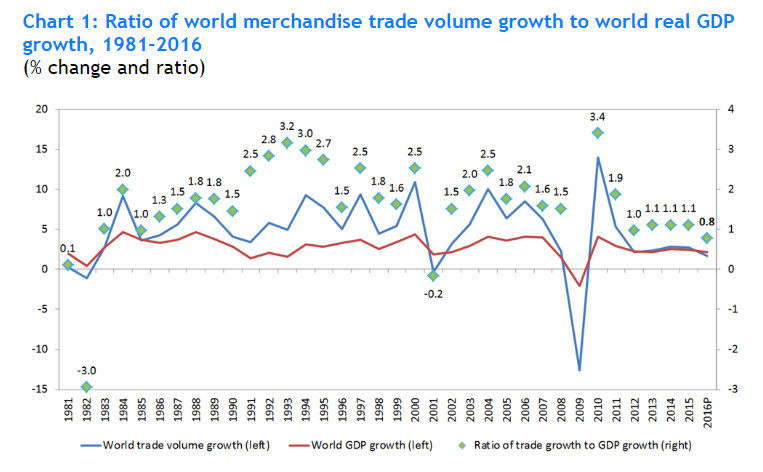

Global trade is awful. Really, it is. For the last five years, trade volumes have been growing at their slowest sustained rate since the early 1980s. Here's a horrible chart from the World Trade Organisation's latest forecast: And in the last year, things have got worse: Import demand of developing economies fell 3.2% in Q1 before staging a partial recovery of 1.5% in Q2. Meanwhile, developed economies recorded positive import growth of 0.8% in Q1 and negative growth of -0.8% in Q2. Overall, world imports stagnated in the first half of 2016, falling 1.0% in Q1 and rising 0.2% in Q2. This translated into weak demand for exports of both developed and developing economies. For the year-to-date, world trade has been essentially flat, with the average of exports and imports in Q1 and Q2 declining 0.3% relative to last year. Oh great. The WTO's chart shows that flat trade eventually translates into flat growth. And as this chart from the World Bank shows, growth is indeed flat: Now, ok, things were worse in the early 1990s, and much worse in the early 1980s. In fact if we went back further, we would also find things were pretty bad in 1973-5. Developed-world recessions are bad for global growth.

Topics:

Frances Coppola considers the following as important: China, Debt, Emerging Markets, lending, trade

This could be interesting, too:

Dean Baker writes Donald Trump is badly nonfused # 67,218: The story of supply and demand

Merijn T. Knibbe writes Peak babies has been. Young men are not expendable, anymore.

Robert Skidelsky writes In Memory of David P. Calleo – Bologna Conference

Global trade is awful. Really, it is. For the last five years, trade volumes have been growing at their slowest sustained rate since the early 1980s. Here's a horrible chart from the World Trade Organisation's latest forecast:

Import demand of developing economies fell 3.2% in Q1 before staging a partial recovery of 1.5% in Q2. Meanwhile, developed economies recorded positive import growth of 0.8% in Q1 and negative growth of -0.8% in Q2. Overall, world imports stagnated in the first half of 2016, falling 1.0% in Q1 and rising 0.2% in Q2. This translated into weak demand for exports of both developed and developing economies. For the year-to-date, world trade has been essentially flat, with the average of exports and imports in Q1 and Q2 declining 0.3% relative to last year.Oh great. The WTO's chart shows that flat trade eventually translates into flat growth. And as this chart from the World Bank shows, growth is indeed flat:

Now, ok, things were worse in the early 1990s, and much worse in the early 1980s. In fact if we went back further, we would also find things were pretty bad in 1973-5. Developed-world recessions are bad for global growth.

But we don't have a developed-world recession now, do we? The developed world is struggling to get inflation off the floor, of course: interest rates are extremely low - in some places negative - and three major central banks are doing QE. In Europe, growth remains elusive and unemployment very high. The US is doing better, but has backed away from planned interest rate increases. Japan is now in its third decade of stagnation. And the UK, which was looking pretty good, has shot itself in the foot. In July, the IMF cut its global growth forecast by 0.1% because of the impact of the UK's decision to leave the European Union. Their October forecast is due out shortly, and signalling ahead of the release is that like everyone else, they are worried about the slowdown in global trade.

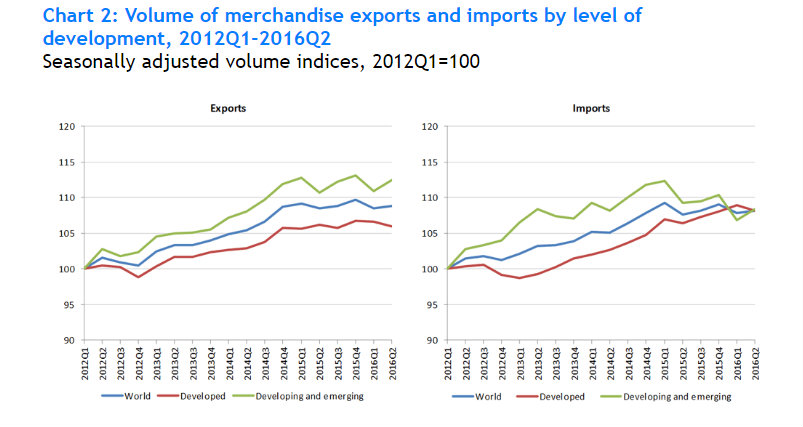

It would, however, be a mistake to see the last four years of global trade slowdown as one event. There are actually two distinct phases, as these charts from the WTO show:

But the current slowdown is not a developed-country story. No, it is caused by a considerable fall in imports to developing and emerging countries, starting at the beginning of 2015.

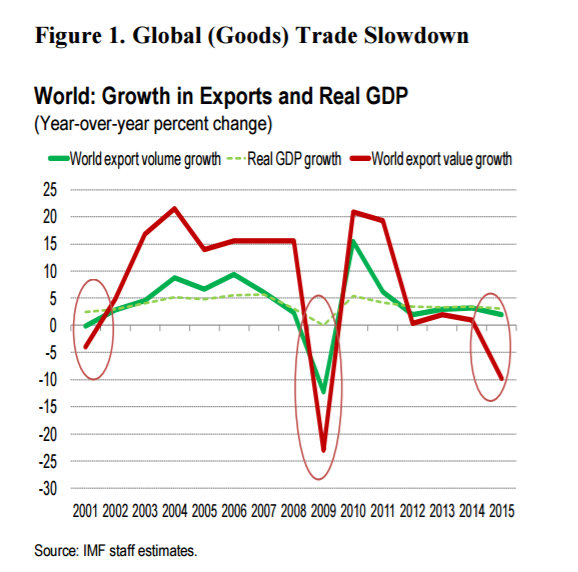

And before some clever devil points out that this is only volumes, and values could look a whole lot better - they don't. They are far worse:

(this chart and the one below are from this IMF working paper)

Global exports have been falling in value terms since 2014. This is partly caused by the commodity and oil supercycle unwinding, which has clobbered the dollar value of exports of raw materials and oil from developing and emerging market countries. But it is also a China story. As this chart shows, China is the single biggest contributor to the trade slowdown of the last two years:

Nonetheless, China's rebalancing has drastic effects on its satellites. It has become a trade hub in Asia, importing goods from other countries in the region as inputs to final processing of items for export to the West. So an import slowdown in China ripples back to other countries in the Asia-Pacific region through the south-south supply chains.

So why is global trade so weak? Most analyses of the current slowdown that I have seen focus on the effect of economic fundamentals on import demand. Some also discuss changes in international supply chains. Few seem to discuss finance, and if they do, they focus narrowly on trade finance, not on the global financial currents that drive all economic activity.

But this is macroeconomics, and if there is one thing we have learned from the GFC, it is that finance is fundamental to macroeconomics. Papers that omit any discussion of the role of global financial flows - like, for example, the IMF working paper from which I took the above charts - are surely unable to explain adequately what is really causing the current trade slowdown.

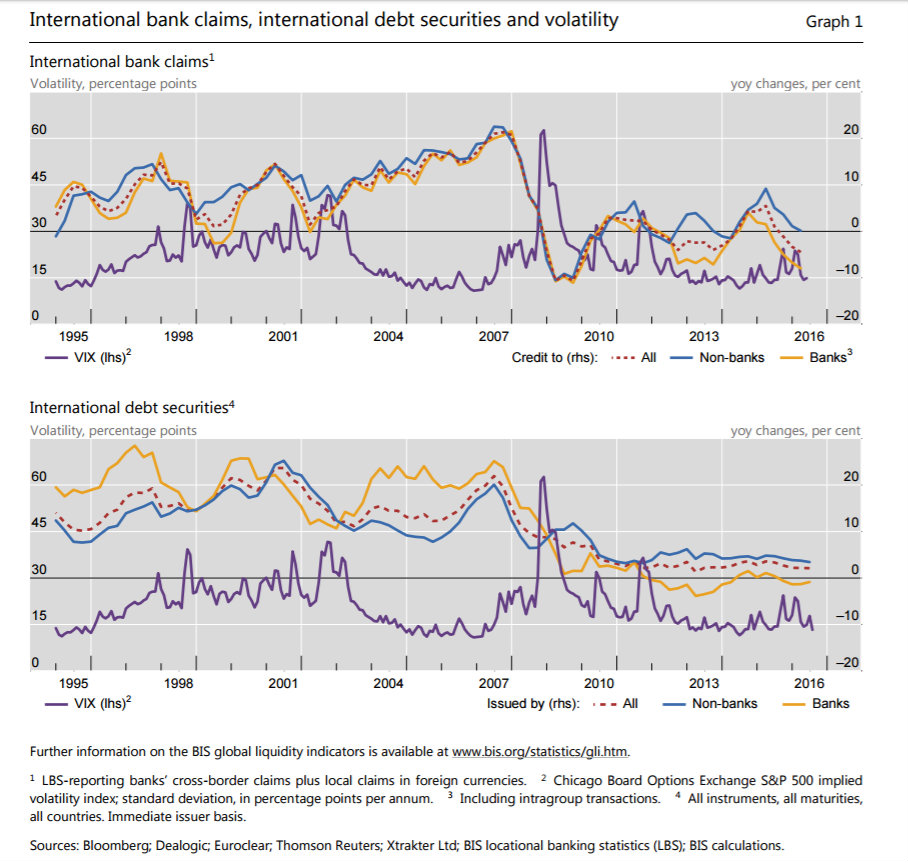

So let's look at what is going on in international finance. This pair of charts is from the Bank for International Settlements (BIS)'s latest review:

Well now. Cross-border lending (loans and bonds) has been flat for the last six years. In 2012-13 there was a marked fall in both lending and securities issuance by banks. And there now appears to be another sharp contraction in bank lending (chart 1) and a tailing-off of securities issuance by both banks and non-banks (chart 2).

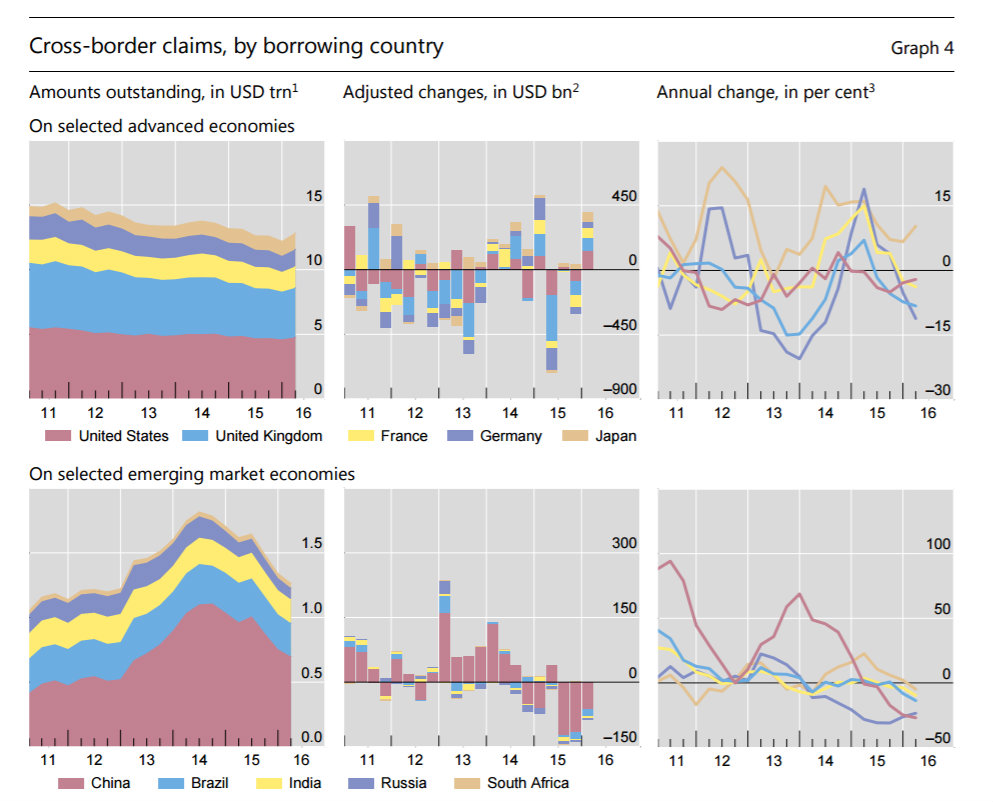

In fact there is a striking resemblance between falling imports in emerging markets (see chart 2 above), and shrinking cross-border finance to emerging markets:

Please don't tell me that this remarkable similarity is purely coincidental. Now that we know how fundamental finance is to macroeconomics, we must surely admit that changes in cross-border financing must be a key part of the global trade slowdown story. Indeed, although I would normally be the first to say correlation doesn't indicate causation, in this case I would stick my neck out and say the contraction in cross-border lending is the primary cause of the sick state of global trade. The reason why the cross-border lending slump precedes the trade slump is because businesses and households can run on reserves for a while when their funding is pulled, and because just as rising investment takes time to flow through into increased trade, so falling investment can take a while to show up as declining trade.

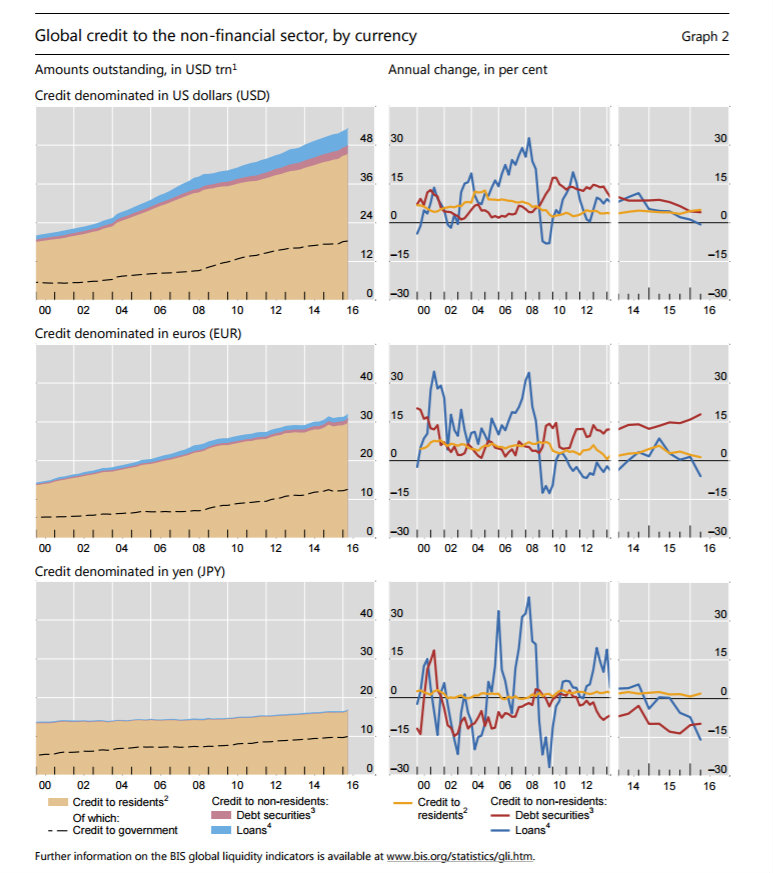

Just how weak cross-border financing has become since 2010 is evident in this set of charts from BIS showing lending to non-banks in the world's three main funding currencies - the US dollar, the Euro and the Japanese yen:

The one bright spot in this dismal set is the Euro debt securities issuance. But sadly this is not what it seems. The BIS explains that this is due to "reverse yankee" issuance by American corporations who have discovered that it is cheaper to fund in euros and swap into dollars than to fund directly in dollars. Accompanying this explanation, the BIS has an interesting paper on why "covered interest rate parity" appears to have failed. It is a story of over-enthusiastic regulation progressively destroying the mechanisms that make markets work efficiently.

But if shrinking cross-border financing is a large part of the answer to "why is global trade so weak?", then the next question is surely "why is cross-border financing shrinking"?

I will attempt to answer that in another blogpost.

Related reading:

Slovenia and the banks

How do you say "dead cat" in Latvian?

Austerity and the rise of populism

Image from Fotolia.