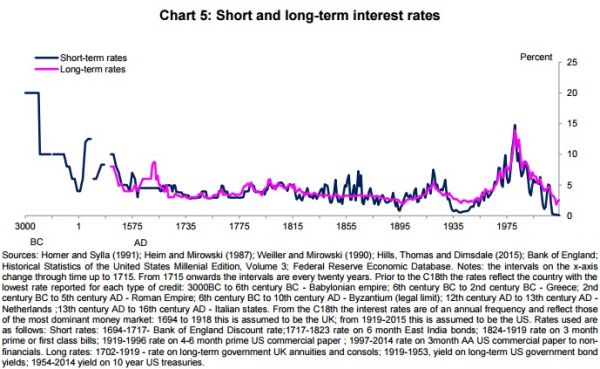

This chart has been fascinating me for ages. It was produced by the Bank of England to illustrate a speech by Andy Haldane. Shock, horror - we have the lowest interest rates for 5,000 years. Even in the Great Depression they were higher than they are now. These are, of course, nominal interest rates. Real interest rates are even lower - though not by much, since inflation is close to zero in all major economies.Note also the divergence of long-term and short-term interest rates. This is encouraging, since it suggests that investors view future prospects as brighter, though hardly scintillating. Central banks have been trying to close that gap with various monetary policy tools, the idea being to bring forward some of that future enthusiasm into the present day. But so far, all they have succeeded in doing is depressing expected interest rates far into the future.Now, policy makers are beginning to talk about interest rates remaining permanently lower than their long-run average. Here, for example, is John Williams of the San Francisco Federal Reserve discussing expectations for r*, the rate of interest when the economy is at full capacity: A variety of economic factors have pushed natural interest rates very low and they appear poised to stay that way (Williams 2015b, Laubach and Williams 2015, Hamilton et al. 2015, Kiley 2015, Lubik and Matthes 2015).

Topics:

Frances Coppola considers the following as important: demographics, history, Interest rates, pensions, savings

This could be interesting, too:

Ken Melvin writes A Developed Taste

NewDealdemocrat writes Constitutional Interregnum

Bill Haskell writes Know Nothings

Angry Bear writes Could Elon Musk Take on Healthcare and Healthcare Insurers and Lower Costs?

This chart has been fascinating me for ages. It was produced by the Bank of England to illustrate a speech by Andy Haldane. Shock, horror - we have the lowest interest rates for 5,000 years. Even in the Great Depression they were higher than they are now.

Note also the divergence of long-term and short-term interest rates. This is encouraging, since it suggests that investors view future prospects as brighter, though hardly scintillating. Central banks have been trying to close that gap with various monetary policy tools, the idea being to bring forward some of that future enthusiasm into the present day. But so far, all they have succeeded in doing is depressing expected interest rates far into the future.

Now, policy makers are beginning to talk about interest rates remaining permanently lower than their long-run average. Here, for example, is John Williams of the San Francisco Federal Reserve discussing expectations for r*, the rate of interest when the economy is at full capacity:

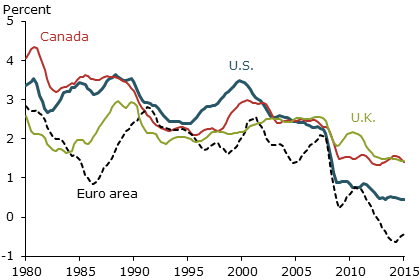

A variety of economic factors have pushed natural interest rates very low and they appear poised to stay that way (Williams 2015b, Laubach and Williams 2015, Hamilton et al. 2015, Kiley 2015, Lubik and Matthes 2015). This is the case not just for the United States but for other advanced economies as well. Figure 1 shows estimates of the inflation-adjusted natural rate for four major economies: the United States, Canada, the euro area, and the United Kingdom (Holston, Laubach, and Williams 2016). In 1990, estimates ranged from about 2½ to 3½%. By 2007, on the eve of the global financial crisis, these had all declined to between 2 and 2½%. By 2015, all four estimates had dropped sharply, to 1½% for Canada and the United Kingdom, nearly zero for the United States, and below zero for the euro area.And here is Williams's Figure 1 showing how rates have fallen:

Unlike the Bank of England's chart, these are real interest rates. But they show the same thing - except that Williams has told only half the story.

It is all about the start point. This chart (courtesy of Economics Help) shows UK nominal interest rates, as in the Bank of England's chart, but plotted against inflation:

The real interest rate is the nominal rate minus inflation. So we can see that in 1975, when the nominal interest rate was about 12% and inflation spiked to 25%, the real interest rate was deeply negative. But by 1981, nominal interest rates had risen to 17%, and the real interest rate was positive. It remained positive for the next 25 years. Remarkably so, in fact. The period from 1982 to 2007 had the highest real interest rates since WWII.

Perhaps even more importantly, for much of that period nominal rates were very high too. People take far more notice of nominal rates than they do real ones. Money illusion is definitely a thing, when you are paying a mortgage and saving for your retirement. And the Bank of England's chart shows that the period from 1975 to 2007 had the highest nominal rates in recorded history. Not since Babylon had there been such high nominal rates sustained for so long.

So the young adults of the 1980s paid the highest interest rates in history on their mortgages and car loans. Now, they are approaching retirement - indeed the oldest among them have already retired. And today's ultra-low interest rates seem like a major betrayal. Where have the returns on their savings gone?

This is a bigger problem than it might seem. In the 1980s, companies started to replace defined-benefit pensions, which promised an income based on final salary, with defined-contribution pensions, where the returns on investment provide an income in retirement. By the mid-1990s, most defined-benefit schemes were closed to new entrants.

Replacing defined-benefit with defined-contribution didn't seem that big a deal at the time. Some people even thought it was better. After all, with the rates prevailing at the time, you wouldn't need a huge investment portfolio to generate quite a decent income in retirement. It never occurred to anyone that interest rates would fall.

And yet they were already falling. All three charts show that interest rates have fallen steadily since their 1980 peak. In fact John Williams's chart shows that real interest rates have fallen rather less in the UK than elsewhere: but it is nominal interest rates that people understand. Now, people are not going to get anything like the returns on their pension investments that they expected. Nor on any other form of savings, either. If anything, private pensions and life insurance schemes look even worse than defined-contribution corporate schemes, and the interest rates on liquid savings such as ISAs are approaching zero.

Over at Bond Vigilantes, Jim Leaviss has an excellent explanation of the rise and fall of post-war interest rates. I have shamelessly borrowed his charts. This one wonderfully shows how the anomalously high interest rates of the 1980s and 90s were entirely due to the baby boom:

And here is Jim's verbal explanation:

The relatively low supply of labour in the 1970s gave power to those of working age. Trade union membership peaked in the late 1970s (when 12 million people in the UK were members) and wage growth outstripped productivity growth and inflation. Government debt burdens grew, and interest rates and bond yields hit double digits. There were talks of ‘buyers’ strikes’ by institutional gilt investors in the UK.

But as the baby-boomers entered the workforce after school or college, there was a significant improvement in the demographic trends. From that low of 40% in 1975, by the end of the 1980s the ratio of workers to non-workers was back above 50%, peaking at over 60% by the end of the 20th century. The developed world had become a world with lots of workers, keeping inflation low (trade union membership shrank), producing tax revenue to reduce government borrowing (at times in the US there was even discussion about retiring the national debt), and investing in paper assets like government bonds to provide future incomes in retirement. Inflation collapsed (you could argue that central banks, despite becoming fierce inflation fighters over this period, starting with Paul Volker taking over at the US Federal Reserve in late 1979, should take little credit here; the demographics did the heavy lifting) and 10-year US Treasury bond yields halved from nearly 13% at the start of the 1980s to 6.5% by the end of the 1990s.Now the baby boomers are leaving the workforce, we should expect interest rates to rise. Here is Jim's view of where interest rates should be now:

So perhaps the baby boomers were not unreasonable in expecting their investments of the 1980s and 90s to deliver a comfortable retirement. Something has gone badly wrong. But what?

Jim identifies five reasons why interest rates have failed to recover. To many people, they will be all too familiar.

- Globalisation: offshoring of jobs to cheaper locations and competition from cheaper imports, putting downwards pressure on wages and prices. In the UK, this was compounded by immigration from the EU.

- The Great Financial Crisis of 2008: deliberate cuts in interest rates, interventionist central banks preventing buyers' strikes, financial repression and poor wage growth

- Technology: progressive replacement of humans with robots causes wages and prices to fall

- Longevity and under-saving: people are living longer, and as already mentioned, older workers have not saved enough, so they are staying in the workforce for longer

- China's influence on the US Treasury bond yield (which influences all other government bond yields)

And they paid in for their pensions and their healthcare, too. So close the tax loopholes, make the rich pay their fair share and honour the pensions and universal healthcare promises of the past. It's only fair.

This leaves me with two unanswered questions. Firstly, why did people fail to see that the high interest rates of the 1980s and 1990s were anomalous? And secondly, why do Williams and others think low interest rates are here to stay? After all, if people in the 1980s could erroneously believe that high interest rates would last forever, people in 2016 can equally wrongly think that low interest rates are here to stay.

We are short-lived creatures: what seems "normal" to us may simply be a pimple or a dent on the surface of time. Looked at through the lens of 5000 years, the high interest rates of the 1980s and 90s were indeed a pimple, but those who lived through that time did not see it. Looked at through the same lens, today's ultra-low rates look suspiciously like a dent.

As we near the end of the golden age of globalisation, the emerging future looks to be nationalist and protectionist. The world is shrinking, becoming poorer and less connected. We may yet see the return of higher interest rates. If, that is, we don't blow the place up first.

This post has been focused on the UK, but many of the drivers I describe apply equally to other developed nations. Falling interest rates and a sense of betrayal among older people are features of much of the developed world. They are not unique to the UK, despite its unusual occupational pension system.