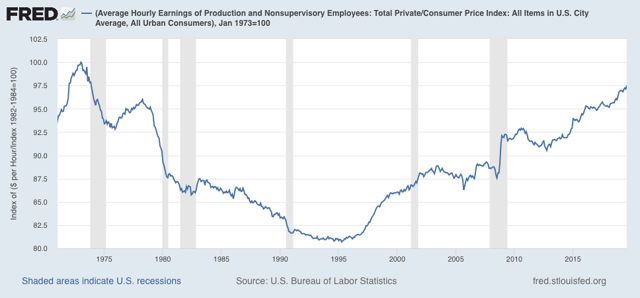

Real average and aggregate wage growth for August Now that we have the August inflation reading, let’s take a look at real wage growth. First of all, nominal average hourly wages in June increased a strong +0.5%, while consumer prices increased +0.1%, meaning real average hourly wages for non-managerial personnel increased +0.4%. This translates into real wages of 97.5% of their all time high in January 1973, a new high following revisions to prior months: On a YoY basis, real average wages were up +1.7%, still below their recent peak growth of 1.9% YoY in February: Aggregate hours and payrolls were up strongly in August’s household jobs report, so real aggregate wages – the total amount of real pay taken home by the middle and working

Topics:

NewDealdemocrat considers the following as important: US/Global Economics

This could be interesting, too:

Joel Eissenberg writes How Tesla makes money

Angry Bear writes True pricing: effects on competition

Angry Bear writes The paradox of economic competition

Angry Bear writes USMAC Exempts Certain Items Coming out of Mexico and Canada

Real average and aggregate wage growth for August

Now that we have the August inflation reading, let’s take a look at real wage growth.

First of all, nominal average hourly wages in June increased a strong +0.5%, while consumer prices increased +0.1%, meaning real average hourly wages for non-managerial personnel increased +0.4%. This translates into real wages of 97.5% of their all time high in January 1973, a new high following revisions to prior months:

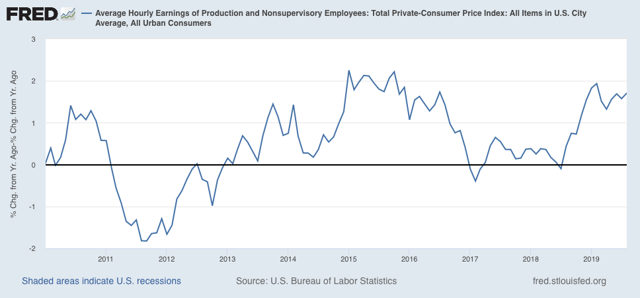

On a YoY basis, real average wages were up +1.7%, still below their recent peak growth of 1.9% YoY in February:

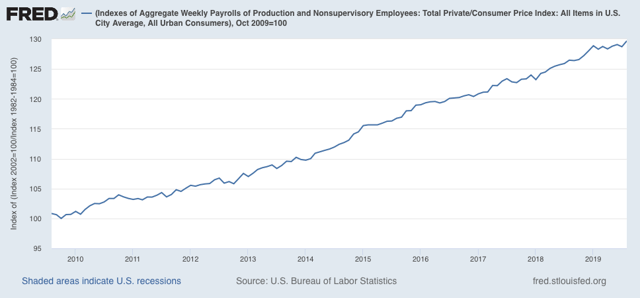

Aggregate hours and payrolls were up strongly in August’s household jobs report, so real aggregate wages – the total amount of real pay taken home by the middle and working classes – are up 29.7% from their October 2009 trough at the beginning of this expansion:

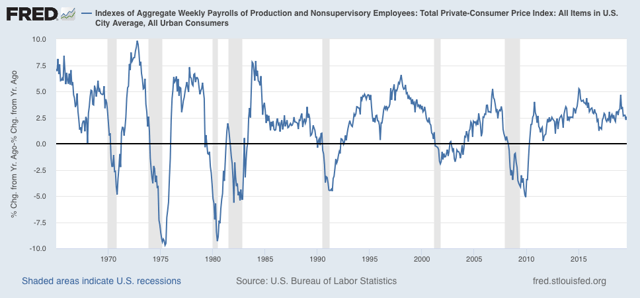

For total wage growth, this expansion remains in third place, behind the 1960s and 1990s, among all post-World War 2 expansions; while the *pace* of wage growth has been the slowest except for the 2000s expansion.

Note that we have had two similar declines already during this expansion. For now, this is just confirming that we are in a slowdown.