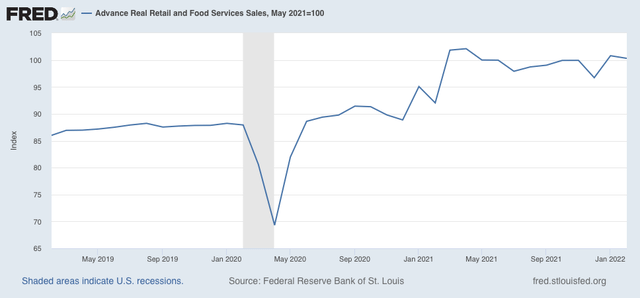

Real retail sales for February: not recessionary, but not healthy either Let’s take a look at the February update for one of my favorite indicators, real retail sales. For the past few months, I have suspected that a sharp deceleration beginning with the consumer sector of the economy was more likely than not. At the moment, the verdict on that forecast is mixed. In February, nominal retail sales rose +0.3%. Since consumer inflation rose 0.8%, real retail sales declined -0.5%. Further, they are down -1.8% from last April’s peak, although they are up 0.3% from last May (using that month because March and April were the stimulus months): On a YoY basis, real sales are up 9.0%, an increase since last month – but entirely due to the comparison

Topics:

NewDealdemocrat considers the following as important: real retail sales, Taxes/regulation, US EConomics

This could be interesting, too:

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Bill Haskell writes Families Struggle Paying for Child Care While Working

Joel Eissenberg writes Time for Senate Dems to stand up against Trump/Musk

Real retail sales for February: not recessionary, but not healthy either

Let’s take a look at the February update for one of my favorite indicators, real retail sales.

For the past few months, I have suspected that a sharp deceleration beginning with the consumer sector of the economy was more likely than not. At the moment, the verdict on that forecast is mixed.

In February, nominal retail sales rose +0.3%. Since consumer inflation rose 0.8%, real retail sales declined -0.5%. Further, they are down -1.8% from last April’s peak, although they are up 0.3% from last May (using that month because March and April were the stimulus months):

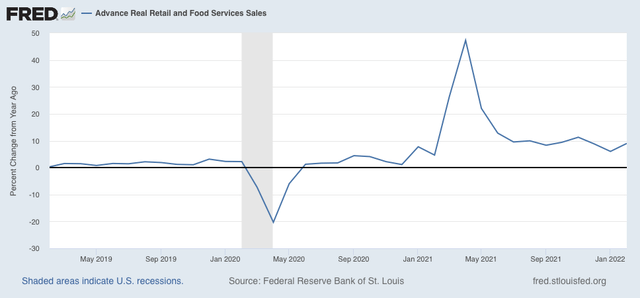

On a YoY basis, real sales are up 9.0%, an increase since last month – but entirely due to the comparison with the decline during the Big Texas Freeze last February. Over the long term this is a very good number:

The big takeaway from the above is that, as shown in the first graph above, real retail sales have been essentially flat beginning last May. That’s not recessionary, but it’s not good either. In other words, this report remains consistent with a slowdown in the consumer sector of the economy.

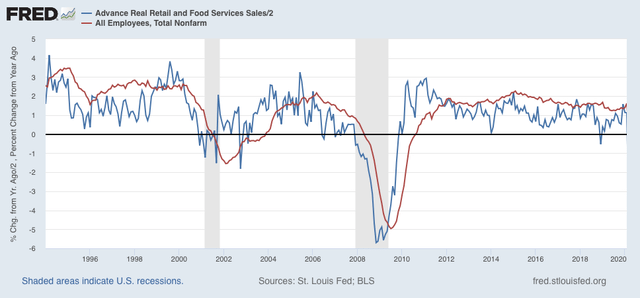

Next, let’s turn to employment because real retail sales are also a good short leading indicator for jobs.

As I have written many times over the past 10+ years, real retail sales YoY/2 has a good record of leading jobs YoY with a lead time of about 3 to 6 months. That’s because demand for goods and services leads for the need to hire employees to fill that demand. The exceptions have been right after the 2001 and 2008 recessions, when it took jobs longer to catch up, as shown in the graph below, which takes us up to February 2020:

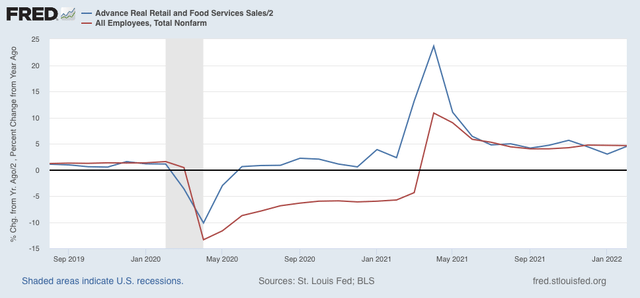

Now here is the same graph since just before the pandemic hit:

In February the two returned to their recent near-perfect sync, at roughly +4.5% YoY. With real retail sales essentially flat for the last 9 months, and down compared with last March and April, I expect the string of monthly jobs reports averaging 500,000 or more will end in several more months. Whether we get a negative print at some point in spring or early summer will depend on whether sales continue to go sideways, improve, or deteriorate.

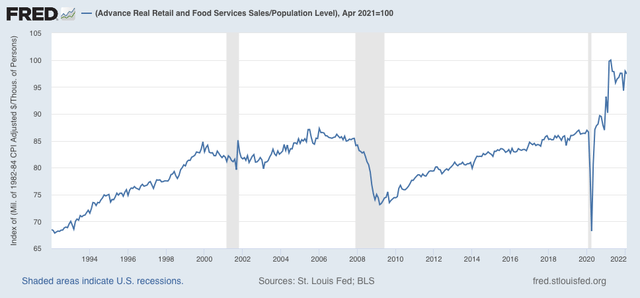

Finally, real retail sales per capita is one of my long leading indicators. Here’s what it looks like for the past 30 years:

These are down -2.6% since last April, and down -0.5% since last May, this remains a negative signal and continues to reinforce the long leading forecast of a stall or near-stall in the economy by about the end of this year.