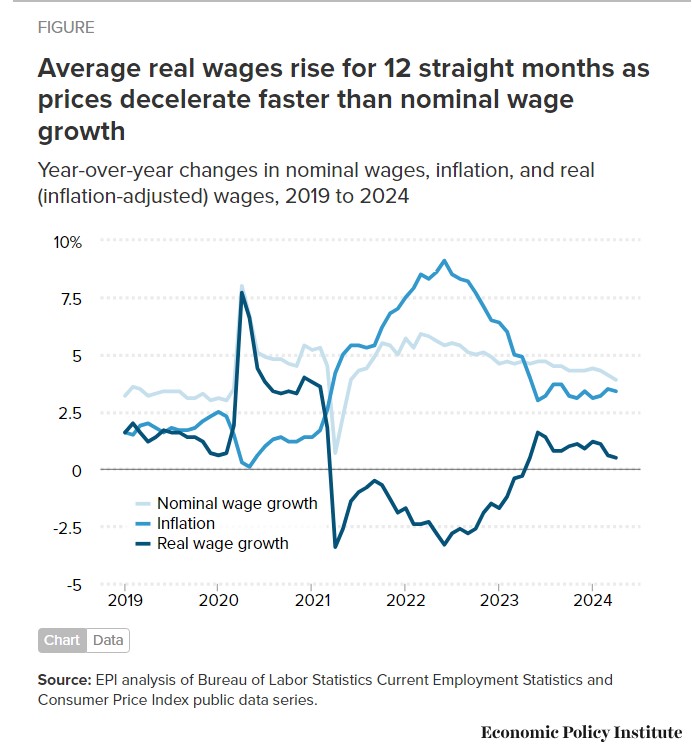

by Elise Gould EPI Average hourly wage growth has exceeded inflation for 12 straight months, according to new Bureau of Labor Statistics data released this morning. This real (or inflation-adjusted) wage growth is a key indicator of how well the average worker’s wage can improve their standard of living. As inflation continues to normalize, I’m optimistic more workers will experience real gains in their purchasing power. The dark blue line in the figure below plots year-over-year real hourly wage changes for all private-sector workers. Year-over-year real wage changes measure the percent change in wages in one month compared with the same month a year prior. Monthly or even quarterly changes in wages are notably more volatile. While

Topics:

Angry Bear considers the following as important: EPI, Hot Topics, US EConomics, wage growth

This could be interesting, too:

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Bill Haskell writes Families Struggle Paying for Child Care While Working

by Elise Gould

EPI

Average hourly wage growth has exceeded inflation for 12 straight months, according to new Bureau of Labor Statistics data released this morning. This real (or inflation-adjusted) wage growth is a key indicator of how well the average worker’s wage can improve their standard of living. As inflation continues to normalize, I’m optimistic more workers will experience real gains in their purchasing power.

The dark blue line in the figure below plots year-over-year real hourly wage changes for all private-sector workers.

Year-over-year real wage changes measure the percent change in wages in one month compared with the same month a year prior. Monthly or even quarterly changes in wages are notably more volatile. While shorter-term measures are valuable to capture very recent changes, this year-over-year measure provides a more stable and longer-term perspective on the state of real wage growth.

As the figure shows, average real wages rose sharply at the onset of the pandemic, but it is because the bottom dropped out of the labor market when millions of lower-wage workers lost their jobs. Average real wages then fell sharply in the pandemic recovery as many of those lower-wage workers returned to work, pulling down the average. Real wage growth continued to decline as inflation rose steadily due to supply chain bottlenecks and shifts in consumer demand. As quickly as inflation rose—peaking at 9.1% in June 2022—it fell, hitting 3.0% in June 2023.

Nominal wage growth is the year-over-year growth in wages, not adjusted for inflation. The Federal Reserve looks at that measure for signs of wage-driven inflationary pressures. What’s clear is that nominal wage growth has been steadily decelerating over the last two years, as shown in the lightest blue line in the figure. The latest data find nominal wage growth at 3.9%, just a bit above the 3.5% long-run target for wage growth that is consistent with the Fed’s inflation target (2.0%) plus productivity growth (likely around 1.5%).

While nominal wage growth is an important indicator for Fed policymakers to measure signs of labor market slack and inflationary pressures (and these remain relatively muted), real wage growth is what matters for workers’ living standards. On average, the data are clear: wages have been beating inflation for 12 months now.

Looking beyond the average, production/non-supervisory workers—roughly the bottom 82% of the wage distribution—started seeing positive real wage growth two months earlier in March 2023, now 14 months in a row (not shown). It’s not surprising that those more moderate-wage workers experienced faster wage growth as other research has shown that lower-wage workers had the strongest wage growth during the pandemic, which is quite unusual in recent U.S. history. These gains for workers are encouraging—and something I hope continues.

Angry Bear . . . Any increase in Social Security withholding staves off depletion of the trust fund. On a 40,000 annual salary, 1/2 of 1% withholding is $200 annually for a person and the same for a company. Not rocket science.