Asymptosis » Actually, Only Banks Print Money, Steve Roth I’m thinking this headline will raise some eyebrows in the MMT community. But it’s not really so radical. It’s just using the word money very carefully, as defined here. Starting with the big picture: You can compare the magnitude of these asset-creation mechanisms here. (Hint: cap gains rule.) The key concept: “money” here just means a particular type of financial instrument, balance-sheet asset: one whose price is institutionally pegged to the unit of account (The Dollar, eg). The price of a dollar bill or a checking/money-market one-dollar balance is always…one dollar. This class of instruments is what’s tallied up in monetary aggregates. A key tenet of MMT, loosely

Topics:

Steve Roth considers the following as important: Hot Topics, money, US EConomics

This could be interesting, too:

NewDealdemocrat writes JOLTS revisions from Yesterday’s Report

Joel Eissenberg writes No Invading Allies Act

Bill Haskell writes The North American Automobile Industry Waits for Trump and the Gov. to Act

Bill Haskell writes Families Struggle Paying for Child Care While Working

Asymptosis » Actually, Only Banks Print Money, Steve Roth

I’m thinking this headline will raise some eyebrows in the MMT community. But it’s not really so radical. It’s just using the word money very carefully, as defined here.

Starting with the big picture:

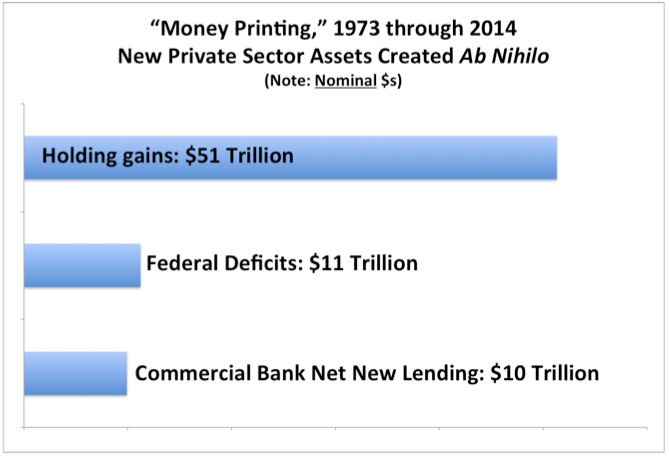

You can compare the magnitude of these asset-creation mechanisms here. (Hint: cap gains rule.)

{kind=link}

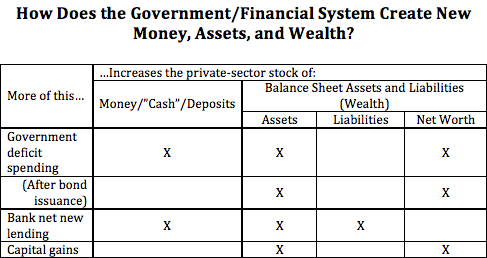

The key concept: “money” here just means a particular type of financial instrument, balance-sheet asset: one whose price is institutionally pegged to the unit of account (The Dollar, eg). The price of a dollar bill or a checking/money-market one-dollar balance is always…one dollar. This class of instruments is what’s tallied up in monetary aggregates.

A key tenet of MMT, loosely stated, is that government deficit spending creates money. And that’s true; it delivers assets ab nihilo onto private-sector balance sheets, and those new assets are checking deposits — “money” as defined here.

But. Government, the US Treasury, is constrained by an archaic rule: it has to “borrow” to cover any spending deficits. So Treasury issues bonds and swaps them for that newly-created checking-account money, reabsorbing and disappearing that money from private sector balance sheets.

If you consolidate Treasury’s deficit spending and bond issuance into one accounting event, Treasury is issuing new bonds onto private-sector balance sheets. It’s not printing “money,” not increasing the aggregate “money stock” of fixed-price instruments.

This was something of an Aha for me: If you look at the three mechanisms of asset-creation in the table above, only one increases the monetary aggregates that include demand deposits (M1, M2, M3, and MZM): bank (net new) lending.

Arguably there might be one more row added to the bottom of this table: so-called “money printing” by the Fed. But as with Treasury bond issuance, that doesn’t actually create new assets. The Fed just issues new “reserves” — bank money that banks exchange among themselves — and swaps them for bonds, just changing TheBanks’ portfolio mix. That leaves private-sector assets and net worth unchanged, and only increases one monetary aggregate measure: the “monetary base” (MB).

I’ll leave it to my gentle readers to consider what economic effects that reserves-for-bonds swap might have.

Asymptosis » MMT and the Wealth of Nations, Revisited, Steve Roth