Summary:

Jeremy Corbyn’s “People’s QE” scheme has been extensively discussed in the media. In fact it has caused something of a storm. The FT’s Chris Giles did an excellent balanced analysis of it, and there have also been useful contributions from – among others - Oxford University’s Simon Wren-Lewis, The Economist’s Buttonwood and FT Alphaville’s Matt Klein. The extent of discussion is far more, in my view, than the scheme deserves.

The scheme envisages that the Government, via a public investment bank, would issue bonds for infrastructure development, which would then by bought by the Bank of England as part of a QE programme. The architect of the scheme, Richard Murphy, suggests that to avoid accusations of monetary financing of government – which is a breach of the UK’s obligations under the Lisbon Treaty – the bonds would be issued to the private sector initially at a price set by the Bank of England, which would then hoover them up in (presumably compulsory) secondary purchases. I find it hard to see how this complies with the spirit of Article 123, but I’ll let that pass. My real objection

to this scheme lies elsewhere.

The need that this scheme ostensibly addresses is the desperate need for investment in infrastructure, R&D, skills and social housing. Few, I think, would disagree with this.

Topics:

Frances Coppola considers the following as important:

government,

investment,

QE,

sovereign debt

This could be interesting, too:

Frances Coppola writes Why the Tories’ “put people to work” growth strategy has failed

DT Cochrane writes What do Canadian corporations do with their profits?

Frances Coppola writes We need to talk about the state pension

Steve Roth writes Government is Not the Problem. Bad Government is the Problem

Jeremy Corbyn’s “People’s QE” scheme has been extensively discussed in the media. In fact it has caused something of a storm. The FT’s Chris Giles did an

excellent balanced analysis of it, and there have also been useful contributions from – among others - Oxford University’s

Simon Wren-Lewis, The Economist’s

Buttonwood and FT Alphaville’s

Matt Klein. The extent of discussion is far more, in my view, than the scheme deserves.

The

scheme envisages that the Government, via a public investment bank, would issue bonds for infrastructure development, which would then by bought by the Bank of England as part of a QE programme. The architect of the scheme, Richard Murphy, suggests that to avoid accusations of monetary financing of government – which is a breach of the UK’s obligations under the Lisbon Treaty – the bonds would be issued to the private sector initially at a price set by the Bank of England, which would then hoover them up in (presumably compulsory) secondary purchases. I find it hard to see how this complies with the spirit of

Article 123, but I’ll let that pass. My real objection

to this scheme lies elsewhere.

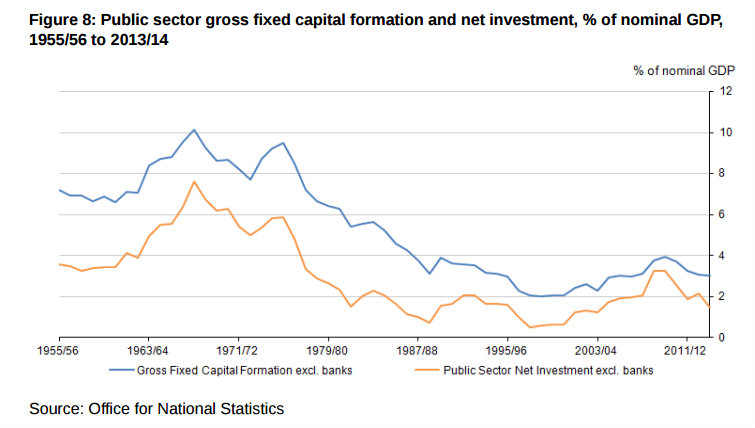

The need that this scheme ostensibly addresses is the desperate need for investment in infrastructure, R&D, skills and social housing. Few, I think, would disagree with this. Private and public sector investment in Britain have both been well below levels in most other developed countries for a long time. The Coalition government not only reversed the modest investment spending increases of the previous Labour government, it made deep cuts: halving the deficit between 2010 and 2015 was achieved in part by halving investment spending. Despite interest rates at unprecedentedly low levels, government investment in the future of the economy is now at its lowest for over a decade (

ONS, 2014):

Not only is investment desperately needed, safe assets are too. Savers suffer from cripplingly low returns on their savings in part because the supply of government debt – which makes up a substantial part of pension investments - has been restricted by QE, raising its price and hence depressing its yield. The Bank of England currently owns about 30% of the UK’s stock of gilts. Of course, the loss in yield is offset by the gain in price. But for those who live on the returns on their pensions, this is cold comfort. The last few years have been grim, and there is no end in sight: interest rates remain on the floor and the Bank of England shows no signs of unwinding its QE purchases. The Coalition government offered some relief to pensioners with its

Pensioner Bonds, which enabled retirees with liquid savings to buy government bonds at above market rates. But this is a drop in the ocean.

The fact is that there is plenty of demand among UK residents for UK government debt, including longer maturities, and plenty of potential public sector investment projects that could be funded by long-term government debt. Government debt is the safest form of saving available to UK residents, as well as an important anchor in the financial system. There is absolutely no reason from an investment point of view to restrict its supply.

But a toxic narrative has grown up around government debt. Because of events in the Eurozone and some unhelpful academic research, we have learned to regard it as something bad to be eliminated – a burden on future generations, a drag on growth, a source of fiscal vulnerability. At very high interest rates, this would be true. But at today’s very low interest rates, the return on the vast majority of investments would far exceed the cost, even if bonds were issued at a premium to market rates as the Pensioner Bonds were. Tomorrow’s pensioners would be supported by the returns on their investment today, while their children and grandchildren benefited from modern infrastructure, better education and a higher standard of housing. And importantly, businesses of the future would benefit from investment in R&D and innovation. We need to stop regarding government debt as something malign, and start regarding it as a social good. It is the investment of today’s citizens in their own future and the future of those they love.

How the Government should organise the financing of public sector investment projects is a matter of some debate. Richard Murphy envisages a public investment bank, capitalised by the government, which would issue bonds to fund itself and lend funds to suitable projects. But the government is already

its own bank: it could simply issue bonds directly to the public to fund specific projects. The UK has historically funded wars by issuing War Bonds directly to the public. Why should it not finance infrastructure projects, R&D, education and social housing construction by issuing Development Bonds?

An alternative would be a leveraged Sovereign Wealth Fund, which would fund itself by issuing bonds which it would use to purchase assets. This could include taking equity stakes in housing, infrastructure developments and - possibly – innovative start-ups. Clearly such a fund would take risks, but importantly these risks would not be passed on to the people whose life savings would be funding it. Government can eat losses much better than small savers. Anyway, there is no particular reason why a leveraged sovereign wealth fund should lose money overall if it is properly managed, even with a scatter of project failures.

The arguments of those who object to public sector investment on the grounds of inefficiency usually rest on the belief that government does not evaluate projects properly or manage them effectively. They ask how “malinvestment” would be prevented. There are, of course, examples of project failure in the public sector, some of which have caused

major losses. But this is to ignore the many projects that do deliver on time, to budget and deliver the required returns, particularly in local authorities.

Professional project evaluation and management is as necessary in the public sector as it is in the private sector. Potential projects should be subject to rigorous cost/benefit evaluation with sensible hurdle rates of return. Of course it can be difficult to establish tangible benefits for social projects, but not even to attempt to do so is lazy. Government projects should aim to deliver real returns just as private sector ones do. And they should be properly managed. The mistakes that led to the cancellation of the NHS project - and other expensive failures - were

elementary project management errors. These are as common in the private sector as the public sector: but private sector project failures are swept under the carpet, whereas public sector ones make headline news. The possibility of failure should not deter investment in the public sector any more than it does in the private sector.

Of course, borrowing for investment does have limits. When governments are very highly indebted, investors start to get worried and bond yields start to spike. But we are nowhere near that limit. Japan currently has debt of over 200% of GDP. For much of the last century, the UK’s public debt was well in excess of 100% of national income, as indeed it was for much of the previous century too (

Ritschl, 1996):

Neither Japan nor the UK has ever defaulted on public debt. Indeed, Japanese government bonds and UK gilts are regarded as among the safest investments in the world. Even quite a sizeable increase in public debt for investment purposes would be unlikely to change this, especially if investors knew the Bank of England stood ready to buy bonds if necessary to stabilise yields. Having a trusted and effective central bank guarding your back makes a huge difference to sovereign creditworthiness. It is this that the Eurozone lacks, and it is for this reason that comparisons with say Greece are invidious.

But there is an additional problem. The UK is still running a fiscal deficit of 5.5% of GDP. How can a substantial investment programme be undertaken without vastly increasing this deficit?

I don’t wish to dismiss the deficit as unimportant. But it is not relevant to the discussion of investment spending. The present situation is that what we might call the “day-to-day” spending of the government exceeds its revenues. I am personally of the opinion that trying to reduce this directly has untoward effects and it would be better to focus on measures to improve productivity and wages, but I recognise that to many people a persistent deficit spells disaster. But judicious investment spending can be expected to raise national income and therefore both increase government revenue and reduce its spending. For example, investment that results in higher productivity feeding through into higher wages means more tax revenue for government AND lower welfare bills. Investment spending has long-term benefits on both sides of the public balance sheet. Indeed, that is its purpose!

Failing to invest in projects which have clear positive returns on the grounds that it would increase the current deficit is a false economy. So investment spending should not be counted as part of the “current” deficit at all. This is the strongest argument in favour of a public investment bank or sovereign wealth fund rather than direct public investment. It makes the distinction between current and investment spending crystal clear and forces the real returns from investment spending and asset acquisition to be recognised in public accounts.

The UK needs investment spending. Restricting investment spending while interest rates are so low is not “responsible management” of the economy. Unfortunately, none of the candidates for Labour leadership have so far pointed this out. All of them –

including Mr. Corbyn – have tacitly accepted that eliminating the deficit is top priority and government debt serves no useful purpose. I find this depressing. And I find it even more depressing that Mr. Corbyn, who at least acknowledges the need for investment spending, fails to address this poisonous narrative head on, preferring to propose a form of financial engineering that would deny Britain’s savers the opportunity to invest in their future for better returns than they currently get. In this respect, “People’s QE” it is not.

It would of course be perfectly acceptable for the Bank of England to buy “Development Bonds” as part of a QE programme in a future recession. Richard Murphy believes that in 2020 there will be a recession. If he is right, then a Jeremy Corbyn-led government could indeed do “People’s QE” as he outlines it. But I fail to see why investing in the future of the economy should be dependent on there being a recession. And I fail to see why it has to wait for 2020, either. Her Majesty’s Opposition should get its act together and make the case for investment NOW.

Related reading:

Image from The Independent.