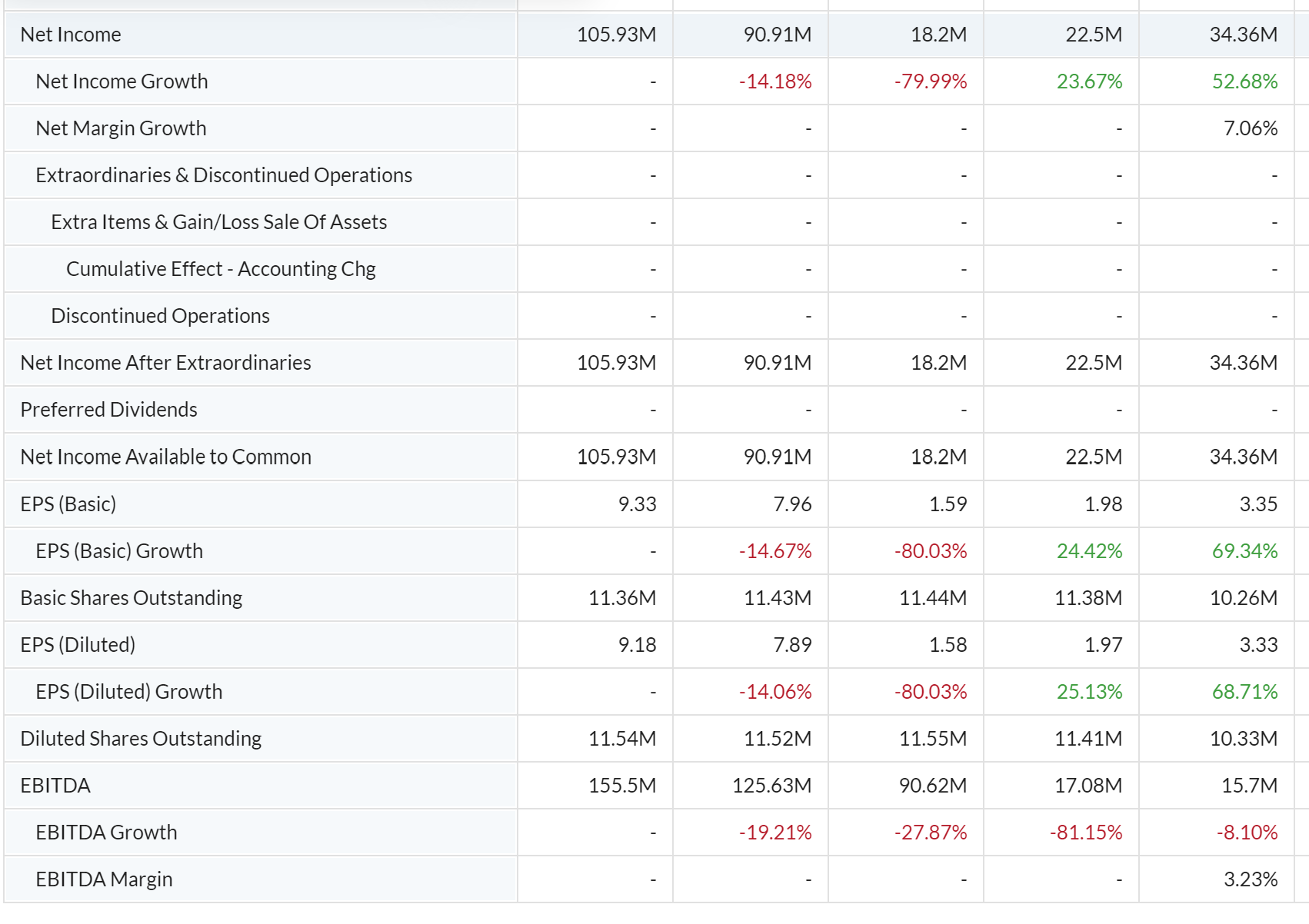

Do you have a poorly-performing company that you don't know what to do with? Bitcoin fixes this! At least, that's what Michael Saylor seems to think. Since August 2020, Microstrategy, the company of which he is simultaneously CEO, chairman and principal investor, has invested heavily in Bitcoin. And Saylor has joined the select group of billionaires fronting the campaign to promote Bitcoin's widespread adoption (and talk up its price). Microstrategy has been bumping along the bottom for quite some time. MarketWatch helpfully reports the income statements for the last five years. They make grim reading. Here are the bottom-line net income and key financial metrics from 2015 to 2019 inclusive:Yes, there's been some improvement in net income, but just look at that EBITDA....The financials

Topics:

Frances Coppola considers the following as important: Bitcoin, Debt, risk

This could be interesting, too:

Dean Baker writes Crypto and Donald Trump’s strategic baseball card reserve

merijn knibbe writes The incredible cost of Bitcoin.

Robert Skidelsky writes Britain’s Illusory Fiscal Black Hole

Michael Hudson writes Gold as the Peace Currency

Do you have a poorly-performing company that you don't know what to do with? Bitcoin fixes this!

At least, that's what Michael Saylor seems to think. Since August 2020, Microstrategy, the company of which he is simultaneously CEO, chairman and principal investor, has invested heavily in Bitcoin. And Saylor has joined the select group of billionaires fronting the campaign to promote Bitcoin's widespread adoption (and talk up its price).

Microstrategy has been bumping along the bottom for quite some time. MarketWatch helpfully reports the income statements for the last five years. They make grim reading. Here are the bottom-line net income and key financial metrics from 2015 to 2019 inclusive:

Yes, there's been some improvement in net income, but just look at that EBITDA....

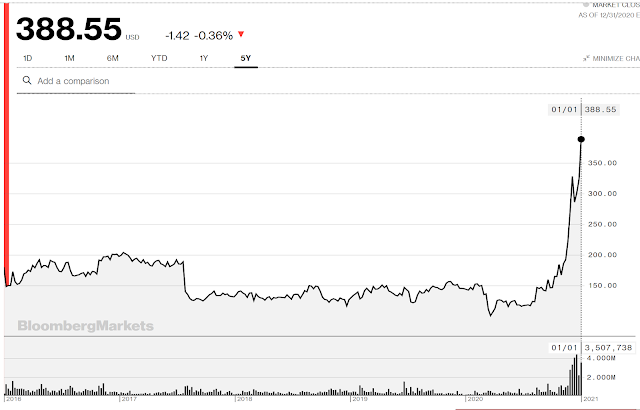

The financials reveal a company that is making little money, generating little free cash and repeatedly reporting operating losses. Sales are disappointing and operating costs are high. At the time of these reports, it had an absolutely massive pile of cash which wasn't being using productively. As a result, the share price was in the doldrums:

"Zombie" is perhaps too harsh a word for Microstrategy, but it does seem to be living in some kind of twilight zone. Vibrant, it is not. And there is - or was - an awful lot of idle cash sitting around. Presumably the only reason it hasn't been a takeover target is that Michael Saylor, who owns about 70% of the voting shares (though only 20% of total stock), for some reason didn't want to sell the company despite its persistently poor performance.

It does make sense for a company with an enormous cash pile to diversify its treasury management: supplementing operating earnings with income from external investments is far more sensible than sitting on a heap of cash equivalents, especially in these days of zero interest rates. But the mystery is why Microstrategy apparently has no use for this cash. It is hardly generating much in the way of sales or income. Surely some of the cash could be productively invested into developing new product lines and upgrading existing ones?

In August 2020, Microstrategy announced that it would make Bitcoin its primary reserve asset. And it proceeded to buy $425m worth of bitcoin, reducing its cash reserves by approximately 90% in the process. But August 2020 turned out to be not the best time to buy; Bitcoin's price promptly dropped, and by the end of September Microstrategy had been forced to impair the carry value of its newly-acquired bitcoin assets by $44.2m. It's perhaps unfortunate that this happened so soon after acquisition, but Bitcoin's volatility means there will inevitably be substantial impairments from time to time. Microstrategy now has little free cash to absorb these shocks, and it still isn't earning much in the way of income. Converting so much of its cash reserve to bitcoin has considerably increased its cash flow risk.

Despite the impairment (or, perhaps, because of it), Microstrategy hung on to its bitcoins. And in December, as Bitcoin's price started to rise rapidly, Microstrategy announced its intention to borrow $650m to invest in yet more bitcoin. The debt offer completed on 11th December and Microstrategy duly spent the money acquiring bitcoin. It has now spent a total of $1.13bn on bitcoin, and its bitcoin holdings, worth some $2.7bn at today's prices, are by far its largest asset.

Despite this, Saylor denies that Microstrategy is a Bitcoin ETF, insisting that Microstrategy's whopping bitcoin investment is simply treasury management. Frankly this excuse is wearing very thin. Microstrategy needed to diversify its treasury, yes, but buying massive quantities of bitcoin isn't diversification. And Microstrategy was probably insufficiently leveraged before - debt can be an efficient way of financing a business, after all. But leveraging it up purely to buy bitcoin isn't investing in the business, unless the business is bitcoin - in which case we are back to a Bitcoin ETF, aren't we?

Saylor has good reason to insist his company is simply using Bitcoin as part of its treasury management. The SEC has blocked every application to establish a Bitcoin ETF so far, and says it won't approve one while Bitcoin's price remains open to manipulation. But the SEC has no jurisdiction over a viable if disappointing company that sells some real goods and services (though not enough to make a decent profit). Investing its entire cash reserves in a single, highly volatile, speculative asset might not be prudent as a treasury strategy, but it's not the SEC's job to tell corporate managers how to run their business. The treasury of a cash-rich company like Microstrategy looks like an ideal place to conceal a Bitcoin ETF.

But if Saylor intended to use his company to conceal a Bitcoin ETF, why did he wait until August 2020 to set it up? Microstrategy has been both performing poorly and sitting on large amunts of cash for at least five years. During that time, Saylor did little to improve the company. He didn't sell the company, didn't significantly invest in it, didn't have much in the way of development plans, and didn't diversify its treasury. In the shareholders' letter of April 2020 he talks about growing the company through new product lines, but never mentions Bitcoin. So why, in August 2020, did Saylor suddenly decide to use the company as a Bitcoin investment vehicle?

Here's a possible explanation. The investment company Grayscale has a Bitcoin investment trust, known as GBTC or simply "BTC". The investment manager Hargreaves Lansdown describes BTC thus:

BTC enables investors to gain access and exposure to the price movement of bitcoin in the form of a traditional security without buying, storing and safekeeping bitcoin directly. BTC’s purpose is to hold bitcoins, which are digital assets that are created and transmitted through the operations of the peer-to-peer bitcoin network, a decentralized network of computers that operates on cryptographic protocols. The investment objective of BTC is for the shares (based on bitcoin per share) to reflect the value of the bitcoins held by BTC, determined by reference to the bitcoin index price, less the BTC’s expenses and other liabilities. The activities of BTC include issuing baskets in exchange for bitcoins transferred to the BTC as consideration in connection with the creations.

So, investors can buy shares in Grayscale's BTC trust instead of having to hold bitcoins themselves. It has been popular with big institutional investors, for whom Grayscale BTC shares allow them to gain from Bitcoin's rollercoaster ride while outsourcing the risks of investing in such a volatile asset.

In August 2020, Grayscale's Bitcoin investment trust (BTC) ramped up its bitcoin holdings. It has continued to do so ever since despite Bitcoin's price fall early in September. And as Bitcoin's price first recovered then rose precipitately, so too did the trust's share price. Grayscale now plans a considerable expansion to accommodate high demand for its cryptocurrency investment vehicles.

Did Saylor see what Grayscale was doing and think "I want some of that"? Is that what drove his decision to refocus his moribund company on bitcoin acquisition? It seems plausible to me, but there might be other explanations. We can never know for certain what goes on in someone's mind, or who influences their decisions behind the scenes.

Whatever the reason for Saylor's decision, the strategy is certainly paying off at the moment. The chart above shows that Microstrategy's share price has rocketed since the company started investing in bitcoin. It is now way overvalued relative to the company's fundamentals, though no-one seems to care about those any more.

But while it is undoubtedly generating riches for Saylor at present, using Microstrategy as a Bitcoin investment vehicle for banks and institutional investors is a highly risky strategy. Bitcoin is notoriously prone to sudden dramatic crashes. The last time there was rapid price appreciation of this kind, it all ended in tears. Microstrategy has put all its eggs in a leveraged Bitcoin basket. A 2018-style Bitcoin crash could mean not just tears, but bankruptcy.

This explains why Saylor has become a high-profile Bitcoin salesman. Bitcoin's volatility is potentially disastrous for his company. So his new job is to talk up its price. Well, maybe not a new job: arguably, this is his old job in a new form. He has a fiduciary duty to his shareholders, and his "treasury diversification strategy" exposes them to the risk of serious losses. It is his responsibility as CEO and chairman of the Board to do whatever it takes to deliver shareholder value - and that now means doing everything in his power to ensure that Bitcoin's price continues to rise indefinitely. Saylor is shilling Bitcoin in the best interests of his shareholders as well as himself.

It's possible that Bitcoin might fix Microstrategy. But it might also destroy it. Microstrategy is taking a massive unhedged long position on a highly volatile speculative asset, and its CEO and chairman is spending all his time talking up that asset's price. When the next Bitcoin crash happens, as it inevitably will despite Saylor's rhetoric, what assets will be left to repay those who have just bought $650m of newly-issued debt?

Related reading:

Clearing out Carillion's cupboards

The sad story of Maplin electronics

Why Bitcoin thrives (and why it won't replace the dollar) - Coindesk

2020 financial results - Microstrategy