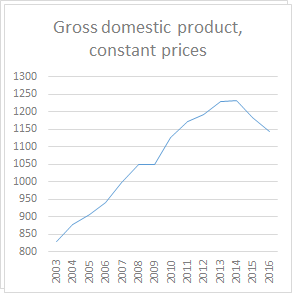

GDP has collapsed by a bit more than 7% in real terms over the last two years in Brazil (graph below show more recent data). This constitutes the worst crisis in recorded macroeconomic history, worse than the debt crisis of the early 1980s, and even the Great Depression. The reasons for this crisis are entirely self-inflicted. I discussed those issues before here (and here). The problem is not fiscal, which resulted from the crisis, nor external, since there was no real issue in financing the current account deficits. The fiscal adjustment was the main cause of the recession. And certainly monetary tightening didn't help, actually it made the fiscal situation worse by increasing debt servicing costs. At any rate, recently a short newspaper piece (in Portuguese, and registration might be required) by André Lara-Resende, one of the authors behind the idea of inertial inflation, and a student of Lance Taylor at MIT in the 1970s, has received significant praise from a wide and diverse audience. So I finally decided to read it.Lara-Resende notes, correctly, that the empirical evidence for the simple Quantity Theory of Money is not particularly good, and that there is little connection between money supply and prices. He also notes that modern macro has had a Wicksellian turn, something that is not that new.

Topics:

Matias Vernengo considers the following as important: Brazil, Fiscal dominance, Fiscal Theory of the Price Level, Gibson Paradox, Lara-Resende, Natural Rate, Quantity Theory of Money

This could be interesting, too:

Matias Vernengo writes The behavior of the nominal exchange rate between the Brazilian Real and the dollar in 2024

Matias Vernengo writes Serrano, Summa and Marins on Inflation, and Monetary Policy

Matias Vernengo writes Very brief note on the Brazilian real and the fiscal package

Matias Vernengo writes 30 years of the Real Plan: Unoriginal Lessons from Latin American Stabilizations

Lara-Resende notes, correctly, that the empirical evidence for the simple Quantity Theory of Money is not particularly good, and that there is little connection between money supply and prices. He also notes that modern macro has had a Wicksellian turn, something that is not that new. He is retooling and trying to learn modern macro at Columbia, and discovered the Fiscal Theory of the Price Level (FTPL).

In the traditional QTM story, if the economy is at full employment, and if we assume that the optimal output level is rigid and does not react to demand expansion, and the central bank increases money supply, then inflation would follow. Inflation may actually follow in this scenario even if the central bank decides to tighten monetary policy and not finance the deficits, according to New Classical authors. Sargent and Wallace argue that economic agents know that lower money supply growth today would lead to faster money growth in the future. In other words, if the central bank does not monetize debt in the present, it will be forced to do so in the future, since public debt is a promise to pay in cash in the future, and tighter money now means more inflation later. This would be a situation in which fiscal policy dominates monetary policy.

Fiscal dominance is a situation where the central bank gives up its control over the quantity of money and over inflation to prevent the government from defaulting on its public debt. In addition, with rational expectations, economic agents would anticipate this higher growth rate in the future, and inflation would accelerate in the present without monetization. Sargent and Wallace suggest that inflation becomes always and everywhere a fiscal phenomenon. This is the basis of the FTPL, and the work of Cochrane, which Lara-Resende sees as unorthodox and an alternative to conservatism.

Note that he sees this ideas as unorthodox, in particular because they can account for the possibility of a positive relation between the nominal rate of interest and the price level, something that used to be called the Gibson Paradox.* But, like Cochrane and his fellow New Classical authors, the idea is that to control inflation you need a good old-fashioned fiscal adjustment (btw, that was true too for the old Monetarists, that thought that monetary expansion was caused by fiscal deficits).

The notion that monetization of debt, or fiscal dominance, would lead to inflation, however, is predicated on the supposition that the system has a tendency to move to full employment, and to do it relatively fast. The central question regarding monetization, then, is what determines this supply constraint that imposes an inflation barrier to demand expansion, what Friedman referred to as the natural rate of unemployment – note that natural was meant to suggest that policy cannot affect it. If the economy is below the supply constraint or the supply constraint is variable, then monetization is not inflationary.

Interestingly enough, Lara-Resende does not discuss whether Brazil is at the natural rate at all, and what would be the effect of a massive fiscal adjustment. The idea here is that low rates of interest would signal, lower inflation expectations, and that the fiscal adjustment would reduce the real rate of interest determined by non-monetary factors (the natural rate of interest). There are too many problems with the notion of a natural rate of interest (yes, as I always insist, go learn about the capital debates). But there is hardly anything unorthodox about it. And besides, austerity, which seems to be the default position now in Brazil, would lead to a worsening of the crisis, and contrary to what Lara-Resende thinks, monetary tightening, through its effect on the exchange rate and the cost of imported goods (and its impact on real wages; on top of the effects of the recession on workers' bargaining power, and the government's policy for minimum wages), would maintain inflation low. Low rates of interest (even if welcome) are not the solution; at this stage only expansionary fiscal policy would work.

* It's not really a paradox in a classical (as in classical political economy) context, in which the interest rate is a cost of production.