Summary:

How many countries can really claim to have full monetary sovereignty?

The simplistic answer is "any country which issues its own currency, has free movement of capital and a floating exchange rate." I have seen this trotted out MANY times, particularly by non-economists of the MMT persuasion. It is, unfortunately, wrong.

This is a more complex definition from a prominent MMT economist:

1. Issues its own currency exclusively

2. Requires all taxes and related obligations to be extinguished in that currency

3. Can purchase anything that is for sale in that currency at any time it chooses, without financial constraints. That includes all idle labour

4. Its central bank sets the interest rate

5. The currency floats

6. The Government does not borrow in any currency other than

Topics:

Frances Coppola considers the following as important:

currency,

MMT,

money,

sovereign debt,

trade

This could be interesting, too:

Merijn T. Knibbe writes Monetary developments in the Euro Area, september 2024. Quiet.

Lars Pålsson Syll writes MMT — debunking the deficit myth

Mike Norman writes Jared Bernstein, total idiot. You have to see this to believe it.

Frances Coppola writes Trade lunacy is back

How many countries can really claim to have full monetary sovereignty?

The simplistic answer is "any country which issues its own currency, has free movement of capital and a floating exchange rate." I have seen this trotted out MANY times, particularly by non-economists of the MMT persuasion. It is, unfortunately,

wrong.

This is a more complex definition from a prominent MMT economist:

1. Issues its own currency exclusively

2. Requires all taxes and related obligations to be extinguished in that currency

3. Can purchase anything that is for sale in that currency at any time it chooses, without financial constraints. That includes all idle labour

4. Its central bank sets the interest rate

5. The currency floats

6. The Government does not borrow in any currency other than its own.

This appears solid. But in fact, it too is wrong.

The big hole in this is the external borrowing constraint - item 6 in the list. If a government genuinely could purchase everything the country needed in its own currency, then it would indeed be monetarily sovereign. But no country is self-sufficient. All countries need imports. So item 3 on the list is a red herring. A government may be able to buy anything that is for sale in its own currency, but that doesn't include oil, or gas, or raw materials for industrial production, or basic foodstuffs. To buy those, you need US dollars. Indeed, these days, you need dollars for most imports. Most global trade is conducted in US dollars.

The only country in the world that can always buy everything the country needs in its own currency, and therefore never needs to borrow in another currency, is the United States, because it is the sole issuer of the US dollar. This is another way of expressing what is known as its "exorbitant privilege".

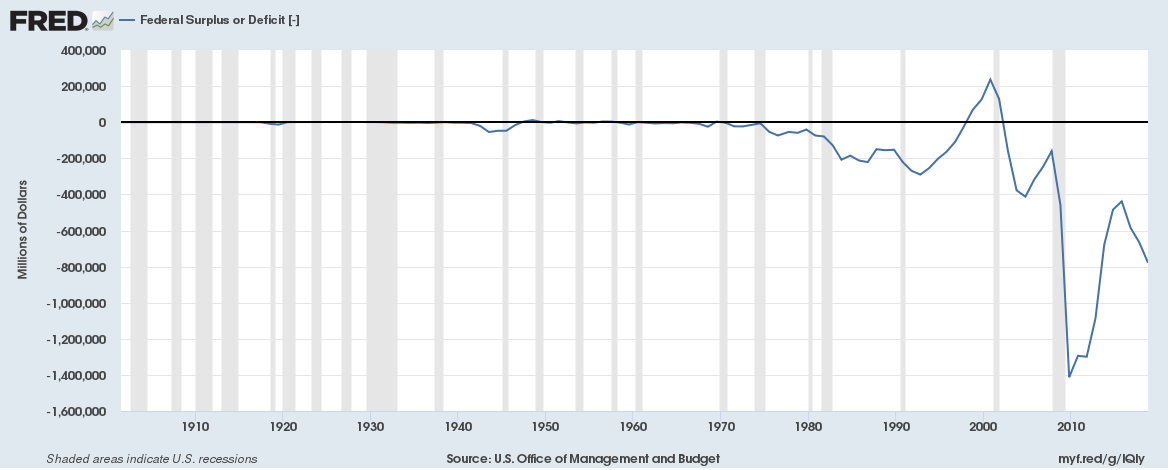

However, the dark side of this is that the US is obliged to run wide current account and fiscal deficits, because global demand for the dollar far exceeds US production. When it attempts to close these deficits, global trade and investment shrinks, causing market crashes and triggering recessions around the world. Sometimes, there is even a recession in the US itself. The US's last attempt to run a fiscal surplus ended in the 2001 market crash and recession:

MMT adherents like to cite this as evidence that eliminating the government deficit in

any country will result in a recession. But this is stretching things considerably. FRED shows us that even in the U.S., only one recession in the last century has been preceded by a government surplus.

Of course, many developed countries do in practice pay for imports in their own currencies. Governments, banks and corporations meet dollar funding requirements by borrowing in their own currency and swapping into dollars in the financial markets. This diminishes the need for dollar-denominated borrowing, either by government or the private sector. These countries therefore have a considerable degree of monetary sovereignty. But it is not absolute as it is in the United States. It crucially depends on the stability of their currencies and the creditworthiness of their borrowers, both of which are a matter of market confidence.

For most countries, the need for external borrowing crucially depends on the external balance. If the current account is balanced or in surplus, then they will earn the dollars they need to pay for essential imports. But any country that runs a current account deficit inevitably borrows dollars.

This doesn't necessarily mean that the government borrows dollars. Borrowing may be largely confined to the private sector, as (for example) it is in Turkey. But private sector FX borrowing is subject to the vagaries of capital markets. If the local currency depreciates significantly (see item 5 in the list), local banks and corporations can find themselves unable to service dollar debts, because dollars become far more expensive.

If banks stop lending cross-border, as they did in 2008, local banks and corporations can find themselves unable to refinance dollar debts. The world is littered with examples of countries that have had to run down public sector FX reserves to provide dollar liquidity to local banks and corporations after they are effectively shut out of global markets by local currency depreciation. If the public sector doesn't have sufficient dollar reserves, it must borrow them, or face financial crisis, widespread debt defaults and economic recession. In an FX crisis, private sector external debt becomes public sector external debt.

Thus, when currencies are allowed to float freely (item 5), no government that runs a current account deficit can possibly guarantee that it will never borrow in any currency other than its own (item 6). The list therefore contains an internal contradiction.

This could be resolved by adding another clause to the list:

7. The current account is maintained in balance or surplus at all times.

Of course, not all countries can maintain the current account in surplus. We do not trade with Mars. So there will always be countries that lack monetary sovereignty even though they issue their own currency, have free movement of capital and a (theoretically) floating exchange rate. In particular, developing countries that have current account deficits and little access to dollar funding markets cannot afford to allow their currencies to collapse. For these countries, item 4 in the list may be true, but it will in practice be determined by the need to support the exchange rate.

Additionally, many countries that maintain the current account in surplus are major exporters of commodities. Australia, for example, is the world's primary exporter of iron ore. The currency exchange rates of these countries

typically track the global price of their primary export. The central bank may set the interest rate, but this tends to have little effect on the movement of funds in and out of the country. These countries do not have full monetary sovereignty.

To explain why, consider what happens if the global price of the primary export falls. Commodity price collapses quickly wipe out the current account surpluses of commodity-exporting countries, forcing them to draw on FX reserves to pay for imports. Additionally, since a current account surplus does not mean there is no dollar debt, the public sector may need to provide dollar liquidity to distressed banks and corporations. Typically, the currency exchange rate collapses at the same rate as the primary export price. So the country has to run down FX reserves, and may need to borrow or buy more, just when dollars are becoming considerably more expensive. This way lies FX crisis.

Admittedly, FX crisis arrives much more quickly for commodity exporters if the exchange rate is fixed. They can quickly burn through their FX reserves propping up the exchange rate and then, when the exchange rate inevitably crashes, find themselves shut out of dollar markets. But floating exchange rates are not a panacea. Falling exchange rates make dollars much more expensive.

Some say that since a currency-issuing government can always print more of its own currency, it can always buy dollars, however low the exchange rate falls. This is the assumption behind items 1 and 5 in the list. It is, unfortunately, a fallacy. Printing more dollars simply hastens the exchange rate collapse. After all, for you to buy dollars, someone has to be willing to buy your currency. And who in their right minds would buy a currency whose value in dollars was falling through the floor?

Printing money to fund an external deficit in a foreign currency always ends with the country shut out of markets and facing a painful choice between an IMF programme and debt default, possibly accompanied by hyperinflation. This has just happened to Argentina. Argentina, a country which issues its own currency, has free movement of capital and a floating exchange rate, does not have monetary sovereignty.

Monetary sovereignty is perhaps best regarded as a spectrum. No country on earth is completely monetarily sovereign: the closest is the US, because of its "exorbitant privilege", but even the US cannot completely ignore the effect of its government's policies on international demand for its currency and its debt.

In general, the major reserve currency issuers tend to have more monetary sovereignty than other countries, because there is international demand for their currencies and their debt. The primary reserve currency issuer is the US, but the Eurozone (for which Germany is the primary safe asset issuer), the UK, Japan, Switzerland, Canada, and - now - China, all fall into this category.

However, there is a hierarchy even among reserve currency issuers. High on the list comes Japan, because its debt is held almost exclusively by its own citizens (and its central bank), and investors regard it as a "safe haven" in troubled times. But the ostensibly similar Switzerland has less monetary sovereignty than Japan, because it has extensive trade and financial ties to its much larger neighbour the Eurozone.

The Eurozone countries have relinquished their monetary sovereignty in the interests of developing ever-closer links. However, the Eurozone as a bloc has a high degree of monetary sovereignty, because its currency is the second most widely used currency for trade after the dollar.

Commodity exporting countries that maintain a diversified economy and don't let their fiscal finances become dependent on commodity prices also retain monetary sovereignty. Norway is perhaps the best example: the sovereign wealth fund took a beating when oil prices crashed, but the country itself didn't suffer much. Sadly, Norway's prudence has not been reflected in other countries.

North Korea also has a high degree of monetary sovereignty, because it is autarkic. The price it pays for this is extreme poverty. Losing some degree of monetary sovereignty is surely a small price to pay for the openness to trade that brings prosperity.

Outside this somewhat exclusive club, monetary sovereignty becomes much diluted.

Few developing countries allow their currencies to float freely, and with reason. A floating exchange rate can be actively damaging to an economy if it is thinly traded and volatile, because the value of imports and exports varies so much: this is why the US dollar, and to a lesser extent the Euro, are so widely used in trade involving developing countries. For many developing countries, pegging to a stronger currency, or even adopting it outright, is the only way of creating sufficient stability for trade to develop.

Free movement of capital can also be extremely harmful to countries that don't have well-developed capital markets and strong institutions. The damage done by hot money flows in and out of developing countries that have prematurely opened their capital accounts is well documented.

Small countries that have close trade and financial links with much larger ones do not have monetary sovereignty, even if their currencies are floating and they have free movement of capital. Perhaps the best example of this is Kazakhstan, which in 2014 was forced to float its currency after the Russian central bank floated the ruble. Kazakhstan's close links with Russia made pursuing an independent monetary policy impossible.

For various reasons, therefore, most countries are not monetarily sovereign, even if they issue their own currencies and have floating exchange rates and open capital accounts. Sadly, if MMT's policy recommendations rely on there being monetary sovereignty, it can never safely be used in more than a handful of countries. Monetary sovereignty is largely a myth.

Related reading: