I always find the views of former policymakers fascinating, not least because of their tendency to become much more outspoken once they are out of office. Some express much more radical views than they did while in office: Larry Summers springs to mind, and Adair Turner. Others become critical of the institutions that they ran: Mervyn King, for example. The latest former policymaker to reveal what he really thinks is Vítor Constâncio, Vice President of the ECB from 2010 to 2018. In a fascinating lecture at the London School of Economics, he discussed the causes of the Euro crisis, the policy responses to it, and what should be done to prevent such a disaster happening again. The entire lecture is on an LSE podcast (audio only, sadly), but Vítor released four of the slides from his

Topics:

Frances Coppola considers the following as important: austerity, ECB, EU, Eurozone, Greece

This could be interesting, too:

Merijn T. Knibbe writes ´Extra Unordinarily Persistent Large Otput Gaps´ (EU-PLOGs)

Merijn T. Knibbe writes Monetary developments in the Euro Area, september 2024. Quiet.

Merijn T. Knibbe writes In Greece, gross fixed investment still is at a pre-industrial level.

Nick Falvo writes Report finds insufficient daytime options for people experiencing homelessness

The latest former policymaker to reveal what he really thinks is Vítor Constâncio, Vice President of the ECB from 2010 to 2018. In a fascinating lecture at the London School of Economics, he discussed the causes of the Euro crisis, the policy responses to it, and what should be done to prevent such a disaster happening again. The entire lecture is on an LSE podcast (audio only, sadly), but Vítor released four of the slides from his presentation on Twitter, with brief comments.

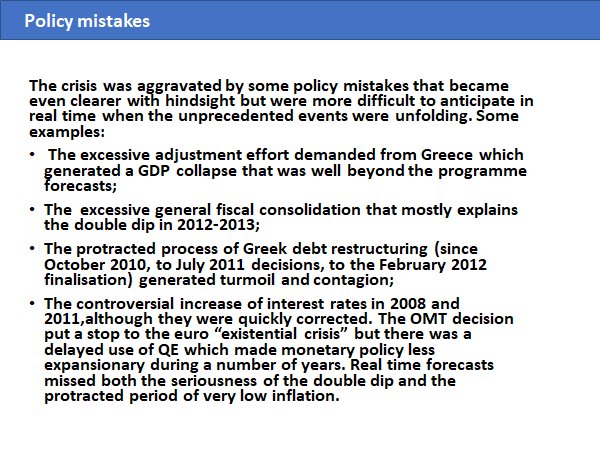

The slide that has attracted the most attention is this one:

Many people seem to have interpreted this as some kind of mea culpa. And the slide does appear to read like this. But I am not so sure. On the podcast, Vítor repeats that this is his view with hindsight, but that at the time, much of this could not have been known. The only policy actions he thinks were clearly mistaken at the time were the two interest rate rises, one in 2008 and the other in 2011 - and he points out that they were quickly corrected, so could not have been major contributory factors in the Eurocrisis and the Greek collapse. An alternative title for his lecture might be, "Being Wise After The Event".

But at the time, many people - including me - thought that severe front-loaded austerity in Greece would make its debt problems worse. Pulling well-thumbed copies of Irving Fisher's Debt Deflationary Theory of Great Depressions and Barry Eichengreen's Golden Fetters from our bookshelves, we waved them under the noses of policymakers.

Our cries went unheard. Eichengreen was irrelevant, apparently, because Greece wasn't on a gold standard - though it was locked into a poorly designed and incomplete monetary union that behaved like a gold standard on steroids. And Fisher was irrelevant because Greece's debt problems were entirely of its government's making and of course had absolutely nothing to do with the behaviour of badly-regulated and excessively risky banks, especially French and German ones. In an unfortunate echo of the way the British press portrayed the Celtic Irish at the time of the 1846-51 famine, the popular press, particularly in Germany, portrayed Greeks as "lazy" and "dependent". No-one wanted to soften the blow.

So we watched impotently as Greece went through every stage identified by Fisher. Unsurprisingly, Greece's Depression became as deep as that of the U.S. in the 1930s. And it lasted for longer. Indeed, it is not by any means over yet.

Thus, Greece's collapse was both foreseeable and foreseen. But those who foresaw the consequences of the policy errors that Vítor identifies were ignored and silenced, just as those who foresaw the 2007-8 financial crisis had been ignored and silenced.

Many of us also warned that concurrent fiscal consolidation across the EU without monetary offset would have deflationary effects. Indeed, on this Keynesians and monetarists were, for once, united; they disagreed about whether fiscal stimulus or QE was more important, but they agreed that doing neither would make recovery all but impossible. But they too were ignored. Policymakers "heard what they wanted to hear, and disregarded the rest."

However, pursuing a witch hunt against policymakers who were blind and deaf to the warnings is unhelpful. What matters is that the world learns from the mistakes that they made.

In this respect, Vítor's contribution is an important step forward. Few of the European policymakers involved in the Eurocrisis and the Greek bailouts have shown any willingness to accept that their decisions caused a wholly unnecessary Depression in several Eurozone countries and a decade of stagnation across the EU as a whole. For example, I have recently been reading Jeroen Dijsselbloem's account of the Eurocrisis. He must know what the policies espoused by the Troika did: yet nowhere is there any recognition of his own role in forcing these through. Rather, he seems complacent and self-congratulatory. I think I would give his book the alternative title "It wasn't my fault".

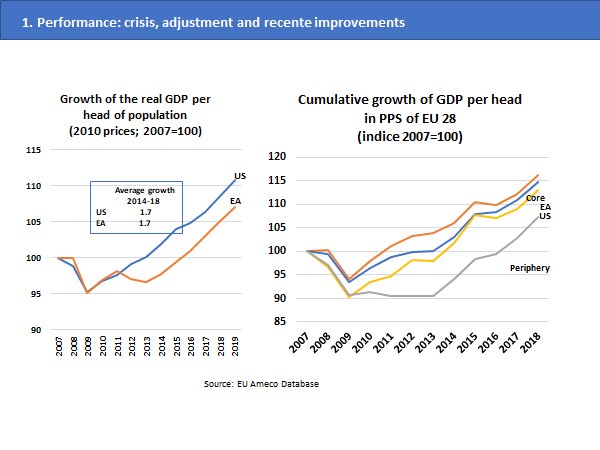

But even more important are the charts that Vítor released on Twitter. This is the first pair.

The first chart shows the Eurozone's pronounced double-dip recession, which seems to have done permanent damage to its output growth relative to the U.S.

Rightly, in my view, Vítor blames this mainly on concurrent fiscal tightening during and after the Eurocrisis. But Eurozone policymakers have not learned from their mistakes. Unemployment across the Eurozone is currently 8%, and much higher in some countries. If U.S. unemployment were still so high, policymakers would be doing fiscal stimulus, and the Fed would be doing QE without end. What are Eurozone governments doing? Balancing their budgets. And what is the ECB doing? Ending QE this year. Policy errors still continue.

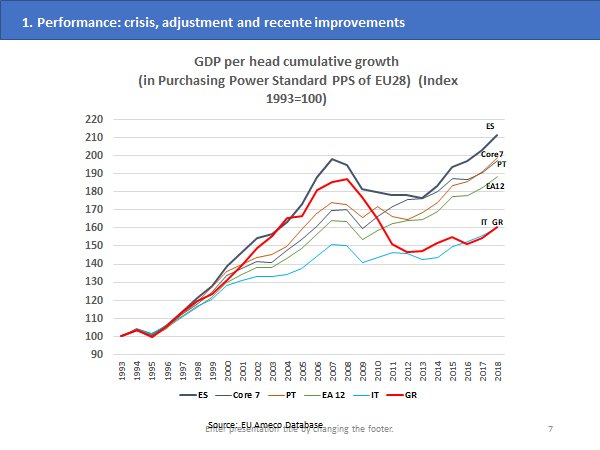

The second chart shows how hard the periphery of Europe was hit compared to the core. The gap has narrowed slightly in the last two years, but they are still a long way adrift. Tight fiscal policy and the ending of QE will make it all but impossible for them to catch up. Policy errors still continue.

But it is Vítor's third chart that really struck me. Here, in glorious technicolour, are the origins of the Eurocrisis. It was set up before the Euro was even created.

In the podcast (seriously, it is well worth listening to), Vítor identifies two financial shocks:

- convergence of real interest rates across the Eurozone after the Maastricht treaty of 1992

- large inflows of credit to the periphery after the Euro was created

Vítor observes that the credit bubble was mostly private debt, and identifies two principal causes:

- low and falling interest rates in the periphery compared to pre-Maastricht levels

- lack of pan-European bank supervision and regulation.

You can build an economy on debt as long as your creditors never change their minds. But if they decide to pull their funds, your debt edifice abruptly collapses. If the debt is mainly private, there can be widespread defaults and bankruptcies, leading to rising unemployment and falling real wages - the classic "debt deflationary spiral". But if the sovereign has borrowed extensively as well - as both Greece and Portugal did - the result can be sovereign default, a collapsing economy and sharp falls in living standards. Imposing severe austerity as the price of debt relief merely makes matters worse.

This is well known in developing countries, where unpayable debt has been written down many times - though sadly now and then some of them forget, over-extend themselves, and then the "sudden stop", debt deflation, debt writedown and IMF programme sequence replays itself, as it is currently doing for Argentina. The hubris of the Eurozone governments was that they thought it could not happen to them. They believed that the monetary union itself would enable them to borrow for resurrection without fear of their debt costs spiralling out of control. How wrong they were.

Could Vítor's policy prescriptions prevent a second Eurocrisis? Here are his recommendations:

The governing principle of the monetary union is that governments must take the market consequences of their fiscal decisions. This is the reason for the "no bailout" clause in the Lisbon Treaty. While this remains the case, I find it hard to see how sovereign debt markets could be reformed to eliminate the risk of liquidity squeezes, sudden stops and redenomination risk. Eliminating the possibility that a government that breaks fiscal rules could suffer sharp increases in borrowing costs, be driven close to default or forced to leave the Eurozone surely fatally undermines the fiscal compact. After all, if a government can break the rules with impunity, what traction can those rules have?

Admittedly, Vítor thinks that the circumstances that caused the Eurocrisis are unlikely to be repeated:

Perhaps he is right. But I wonder. Could it be that rather than people now being used to interest rate and inflation convergence, what people are actually becoming used to is continual pressure on governments to restrain fiscal policy? If so, then a government slipping the leash could break the whole thing open again. The debt of governments that refuse to conform to Eurozone rules carries redenomination risk - because in the end, if they won't abide by the single currency's rules, they must leave it. This is why the yields on Italian sovereign debt are currently rising.However, the initial double shock of much lower rates and huge capital inflows was a one-off shock to countries from a previous regime of higher inflation and rates. It cannot not be repeated in that scale in the future. Convergence of inflation and rates is now established. https://t.co/TUH0yHS3Uj— Vitor Constâncio (@VMRConstancio) October 7, 2018

It's worth recalling that OMT, the ECB's backstop for sovereign debt, is conditional on governments abiding by the fiscal rules. It has never been tested. One day, perhaps it will be. And then maybe we will watch the sequel to the Eurocrisis movie. Eurocrisis 2, alternatively titled "The Day the Fiscal Compact Died".

Related reading:

Nightfall in Euroland

Austerity and the Eurozone