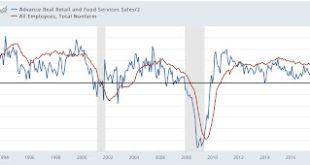

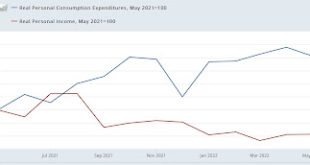

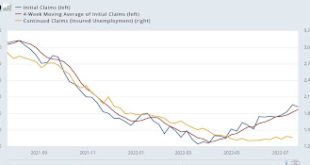

JOLTS report for June amplifies likelihood of substantial downturn in job growth, upturn in unemployment Before we get to the JOLTS report for June, which was released this morning, I wanted to make a point about the overall trend in employment. Because, the two best short leading indicators for employment and unemployment are both pointing South. First, as I have written dozens of times over the past 10+ years, consumption leads employment,...

Read More »JOLTS report for June amplifies likelihood of substantial downturn in job growth, upturn in unemployment